")

Introduction

Hims & Hers (NYSE:HIMS) is a fast-growing telehealth company that is on a mission to help the world feel great through the power of better health. Through H&H’s innovative platform, patients can access personalized, affordable, and high-quality medical care at just the tap of a button.

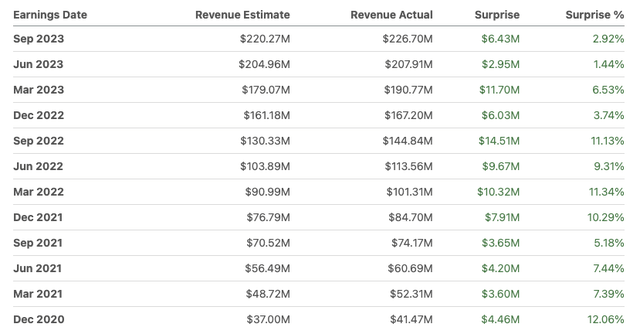

Recently, H&H reported Q3 earnings, delivering yet another beat (on revenue)-and-raise quarter. To say that execution has been strong is an understatement — just look at the company’s track record of beating revenue estimates. There’s not a single quarter where H&H disappointed investors.

Seeking Alpha

Despite the excellent performance, H&H stock is still down 70%+ from its all-time highs and down 40%+ in the past six months alone. While fundamentals continue to improve, the stock has been struggling as of late — if H&H keeps up with its stellar execution, it won’t be long before the stock catches up with its fundamentals.

That said, I believe H&H is one of, if not, the most undervalued small-cap growth stock you can buy today.

Growth

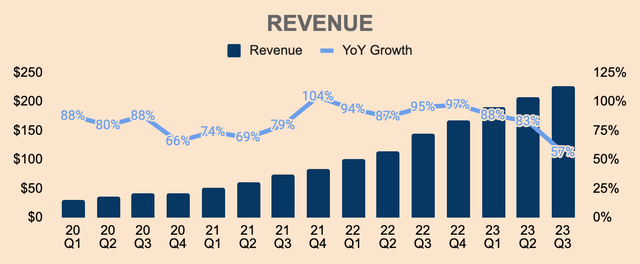

Q3 Revenue was $227M, up 57% YoY. This beat analyst estimates by $6.4M, or 2.9%, and beat management’s mid-point guidance by $7.2M, or 3.3%.

In my previous article, I mentioned that growth is expected to slow down and that is what we’re seeing in the most recent quarter, with growth dropping down ~2,600 basis points sequentially. This is probably the first time growth dropped below 60%. But going forward, I expect growth to continue to decelerate as the scale of the company begins to put pressure on growth.

Author’s Analysis

Breaking it down by segment, the online channel drove the majority of growth with $220M of Online Revenue in Q3, up 57% YoY, driven by the growth in Subscribers, Average Order Values (AOV), and Net Orders.

The online DTC channel is the bread and butter of H&H’s business model, producing high-margin subscription Revenue. As such, it’s great to see that growth in the segment remains robust. But again, expect continual slowdown as the company scales.

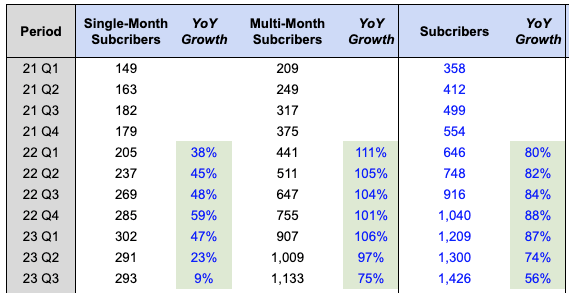

Nevertheless, H&H’s online subscriber base continues to expand with each passing quarter, ending Q3 with 1.4M Subscribers, up 56% YoY. On a QoQ basis, H&H added 126K Subscribers.

Subscriber growth was due to increased Marketing Expenses, which I’ll talk more about later.

Author’s Analysis

Breaking it down further, Single-Month Subscribers grew only 9% to 293K while Multi-Month Subscribers grew a staggering 75% to 1.1M.

It’s worth mentioning that the shift towards Multi-Month Subscriptions will be net beneficial for H&H since longer-duration plans have higher AOVs than Single-Month Subscriptions, which are paid upfront, thus, reducing the risk of Revenue lost through cancellations. From a cash flow management perspective, that is great news for H&H.

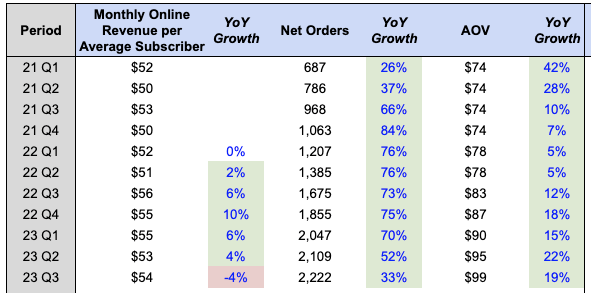

As you can see, AOV continues to expand, growing 19% YoY to $99 per order. Not surprisingly, Net Orders decelerated meaningfully, growing only 33% YoY to 2.2M.

Author’s Analysis

Nonetheless, this shift towards Multi-Month Subscriptions was the result of the price cuts that H&H initiated back in Q2, to make personalized and longer-duration plans more attractive for Subscribers.

Because of the price cuts, Monthly Online Revenue Per Average Subscriber naturally decreased YoY, to $54 a month. However, this is a slight improvement from Q2 as H&H saw more users choosing premium SKUs and switching to personalized plans, which “completely offset the pricing headwinds” in Q3 and gave management confidence that the pricing changes “will be net accretive well within a 12-month period”.

In other words, expect Monthly Online Revenue Per Average Subscriber to increase over time.

In my view, this change in pricing strategy is an intelligent move by management as it sets H&H up well for future growth.

All in all, it’s another beat on revenue estimates. It’s another record quarter. It’s another strong print on growth.

It’s nothing new. It’s business as usual.

On to the next quarter.

This consistent, solid execution is what makes investing in H&H so rewarding. Despite the fluctuation in share prices, the H&H team continues to show up, continues to deliver, and continues to build the company forward.

Profitability

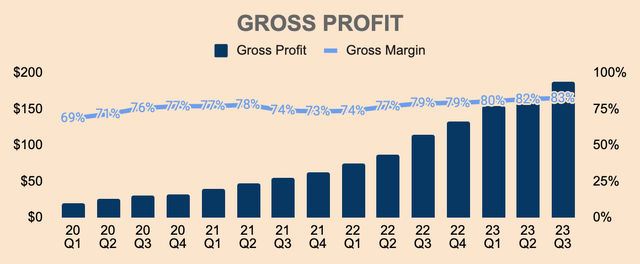

Turning to profitability, Q3 Gross Profit was $187M, representing a Gross Margin of 83%, an all-time high for the company.

This was in large part due to a greater proportion of orders fulfilled by Affiliated Pharmacies, which stands at 80%+ as of Q3. As H&H transitions to 100% in-house fulfillment — which is targeted to be the end of the year — Gross Margins should expand slightly over the next few quarters.

Author’s Analysis

H&H’s goal is to provide high-quality medical care at affordable price points, and with its expanding Gross Margins, management wanted to pass on the savings to its customers, thus the price cuts in Q2.

However, despite the price cuts, Gross Margins continue to expand, which reflects the strength of the company’s business model and value proposition.

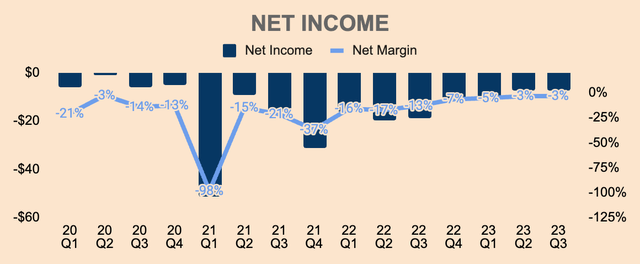

Jumping down the income statement, Q3 Net Income was $(8)M, representing a (3)% Margin. As you can see, Margins are trending in the right direction and GAAP profitability is well within reach. In fact, we could see that happening as early as Q4:

Financial performance continues to be exceptional across all measures and momentum remains solid. As a result of these trends, we expect to generate our first quarter of positive net income within the first half of 2024. Accelerating momentum could bring attainment of this milestone as early as the fourth quarter of 2023.

(CFO Yemi Okupe — H&H FY2023 Q3 Earnings Call)

Author’s Analysis

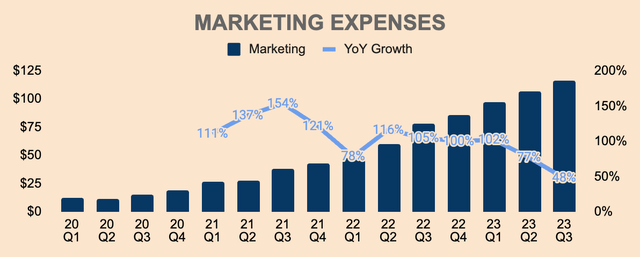

Regardless, one major reason why the company is not yet GAAP profitable is due to elevated Marketing Expenses, which grew 48% YoY to $116M. This reflects management’s focus on maximizing new Subscriber growth.

Author’s Analysis

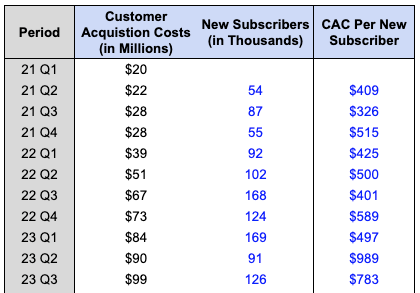

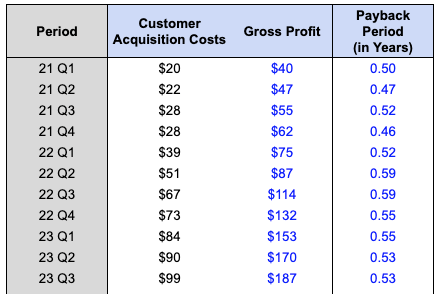

Embedded in Marketing Expenses is Customer Acquisition Costs, or CAC, which the company provided in its 10-Q filings. I’ve gone ahead and compiled the numbers below, along with how many New Subscribers the company managed to sign up in a given quarter.

If we take column 1 and divide it by column 2, we get the average amount that H&H has to spend in order to get a New Subscriber to join the platform.

Author’s Analysis

As you can see, CAC per New Subscriber has worsened over the last few quarters, with a peak of $989 in Q2. Fortunately, Q3 saw a lower figure. However, it is still substantially higher than its average of about $400 to $500.

Moreover, during the Q2 earnings call, management mentioned that “marketing investments were more heavily weighted toward the end” of Q2, which should “provide meaningful customer acquisition tailwind” in Q3.

Because of this heavy marketing spend toward the end of Q2, we should have seen CAC Per New Subscriber drop substantially to the $500 level, but instead, it remains elevated at $783.

Notice how in Q3 last year, H&H added 168K New Members with $67 Million of CAC. But in Q3 this year, H&H only added 126K New Members, despite spending 1.5x more in CAC.

That is a yellow flag for me and I will be watching this metric very closely.

On the other hand, bears like Spruce Point might argue that H&H is overstating its Payback Period and that the metric is actually getting worse and worse.

I object. Payback Period is actually getting better.

Per the company’s Investor Presentation,

Payback period defined as the time it takes quarterly cumulative online gross profit generated by Hims & Hers online customers to exceed the quarterly customer acquisition costs to acquire those customers.

Notice that there’s no mention of “new” customers.

Put simply, Payback Period is defined as CAC divided by Gross Profit.

Author’s Analysis

As you can see, Payback Period has been trending down over the last few quarters, which means that H&H is getting their money back faster. As of Q3, Payback Period was 0.53 years, or slightly over 6 months.

With that short of a Payback Period, maintaining high Marketing Expenses to maximize Subscriber growth is the right move.

In short, Payback Period looks great. However, CAC per New Subscriber must get better.

Regardless, H&H continues to expand Gross Margins, showing economies of scale and strong earnings potential. The company is on track to be GAAP profitable as well which should be a boost of confidence for investors.

As the company becomes more and more profitable, I expect H&H to pass on the savings to customers by cutting prices, which should help the company take even more market share.

Health

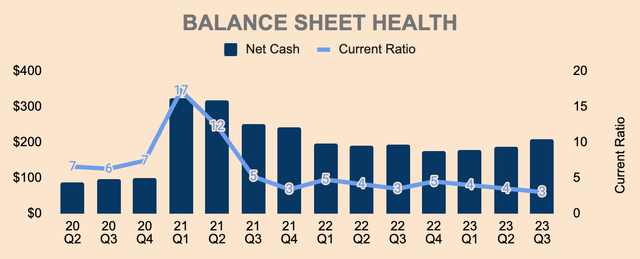

H&H has a pristine balance sheet with $212M of Cash and Short-term Investments with virtually zero debt. As you can see, Net Cash has been building up slowly over the last few quarters, which is great to see.

Author’s Analysis

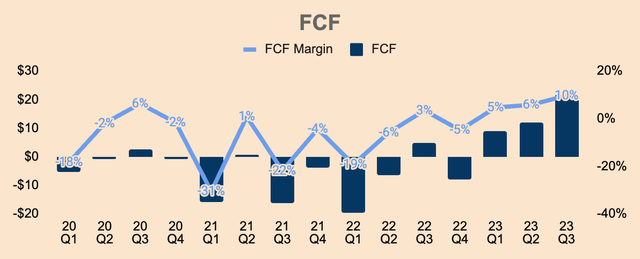

That’s because H&H’s Free Cash Flow generation has been ramping up. As of Q3, FCF was $22M, which is a FCF Margin of 10%. It’s safe to assume that H&H is now self-sufficient.

Author’s Analysis

With more cash in hand, management announced a 2-year $50M share repurchase program as well, citing that shares are “well below what we consider to be their intrinsic value”.

For me, I’m a little bit mixed about the buyback program since H&H is still a hypergrowth company that just turned cash flow-positive. I prefer the company reinvest their profits for future growth but considering the stock’s recent selloff, the company buying back shares may not be a bad idea after all.

Outlook

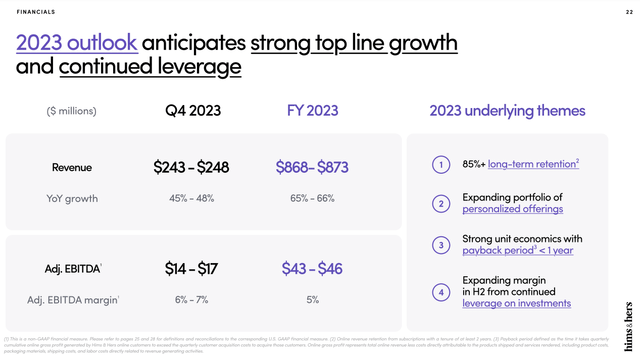

Management raised their guidance once again.

For Q4:

- Revenue of $248M, up 48%. Notice the deceleration from Q3’s growth of 57%.

- Adjusted EBITDA of $17M, which is a 7% Margin. This is an improvement from Q3’s $12M.

For the full year:

- Revenue of $873M on the high end, up 66% YoY. The previous guidance was $850, up by 61% YoY, so that was a sizeable raise. Additionally, this beat analyst estimates by $26M.

- Adjusted EBITDA of $46M, which is a 5% Margin, up from the previous guidance of $40M.

The raised guidance clearly means two things: strong demand and operating leverage.

HIMS FY2023 Q3 Investor Presentation

Whatever it is, H&H’s growth story remains intact.

There are so many categories left untapped such as testosterone, menopause, and Eczema, to name a few.

Management also recently launched MedMatch which is a service that leverages AI and machine learning to identify the most optimal treatment for patients based on H&H’s extensive dataset. With MedMatch, H&H aims to alleviate the time and energy wasted from trial and error, getting a second opinion, and finding the right treatment.

MedMatch is currently in Beta for customers seeking Mental Health support. If successful, H&H can deploy this service among other categories and even potentially license the software to health institutions.

In the next few weeks, investors can also expect the launch of H&H’s weight management offering, opening the doors for the company to enter a category that is worth hundreds of billions of dollars.

Given the company’s recent product launches, I have no doubt that H&H will become the one-stop shop for high-quality, personalized, multi-category medical treatment.

Valuation

In my previous article, I declared H&H’s stock price was irrational due to the fact that the stock sold off immediately after Q2 earnings where H&H posted a triple beat on analyst estimates.

My guess is that the stock sold off likely due to the price cuts that management announced which might have scared some investors. To them, “price cut” may be synonymous with “lower margin” or “softening demand”.

But H&H’s Q3 results say otherwise, with Gross Margins at an all-time high and Revenue growth beating estimates.

With that concern put to bed, H&H stock rallied following its Q3 results.

Rightfully deserved.

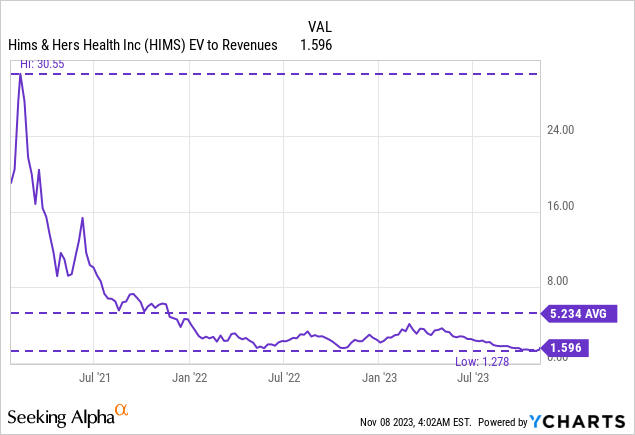

Today, the stock trades at just 1.6x its Revenue, which is a massive discount to its peak of 30.6x and even its average of 5.2x. Its lowest point was 1.3x, so the stock is still trading at the bottom of its range.

This is absurdly cheap for a company that:

- is growing 50%+

- has Gross Margins of 80%+

- has software-like Revenue

- is turning profitable

- has no debt

Ro, its closest and biggest competitor — though private — is valued at $7B. As of this writing, H&H has a market cap of about $1.5B.

Surely, there’s some sort of disconnect here.

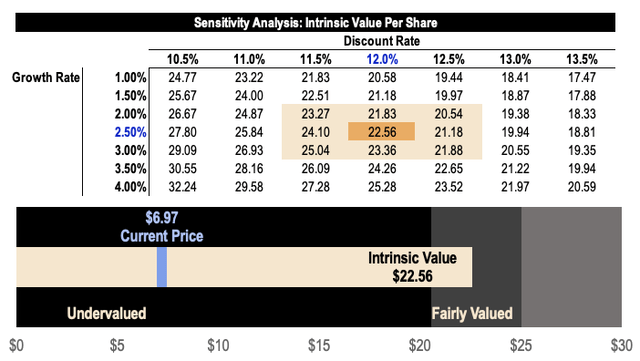

My DCF model says H&H should be valued much higher than its current price of $7 a share. Here are my key assumptions:

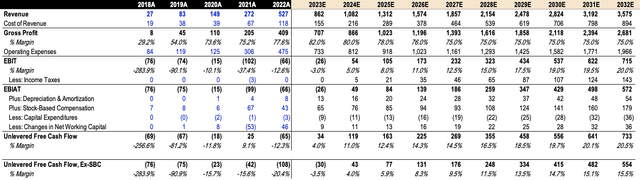

- Revenue: As always, I follow analyst estimates for the first three years, then ramp it down steadily to just 12% growth in 2032. By 2025, I expect Revenue to be $1.3B, which is slightly higher than management’s long-term guidance of $1.2B+.

- Gross Margin: Management guided for Gross Margins to be in the mid-70s so I’m projecting Gross Margins to drop from 82% this year to just 75% by 2027.

- FCF Margin: Lastly, management guided for a long-term Adjusted EBITDA Margin of 20-30%. I will take the low-end and use it to project H&H’s long-term FCF profile.

Author’s Analysis

That said, by 2032, I expect H&H to achieve a Revenue of about $3.6B, with a FCF Margin of 20.5%.

Author’s Analysis

Based on a discount rate of 12% and a perpetual growth rate of just 2.5%, I get a fair value estimate of $22.56 a share for HIMS stock, which is double the average analyst price target of $11.15.

Author’s Analysis

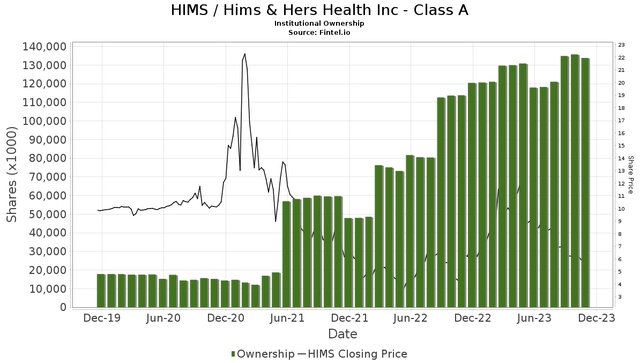

Institutions are loading up on the stock as well as the stock sold off in the last few months, which should be a confidence booster for investors.

Fintel

Add a $50M share repurchase program. Add the stock trading at the lowest multiple ever. Add a possible GAAP Net Income profitability in Q4.

For these reasons, I think the risk to reward on H&H stock is looking extremely attractive for investors.

Risks

Competition

I see Ro and Amazon (AMZN) as the main competitive threats for H&H.

For one, Ro offers a very similar offering to H&H, but I think H&H has superior branding.

The bigger threat, in my opinion, is Amazon, which has One Medical, Amazon Pharmacy, and Amazon Clinic. As I write this article, One Medical just rolled out a “health care benefit for Prime members for only $9 a month”:

Prime members get high-quality, convenient care from One Medical, including 24/7 on-demand virtual care nationwide and easy-to-schedule office visits at any of One Medical’s hundreds of locations across the U.S.— all while saving $100 on the annual membership fee.

(Amazon)

We know Amazon is the king of distribution, logistics, and fulfillment, so it won’t be surprising if some Subscribers switch to Amazon.

Marketing Expenses

As discussed earlier, CAC per New Subscriber remains higher than its historical averages — this metric needs to come back down. If it remains elevated, it could be a sign of saturation or competitive pressure. On the other hand, Payback Period remains healthy.

Thesis

I started following H&H ever since the company went public via a SPAC merger, and all I see is that the company — time after time — delivering and executing its mission of helping the world feel great through the power of better health.

We see this with its financial results. We see this with its innovative product launches. We see this with its consistent outperformance.

Beats and raises. Again and again. Quarter after quarter.

And yet, the stock is struggling.

But this just means that there’s even more time and opportunity for investors to build their positions in this telehealth giant in the making.

As it stands, H&H is probably the most undervalued small-cap growth stock today.

Take advantage of this opportunity.

Read the full article here