")

Introduction

In my previous article, I laid out a bearish thesis surrounding Ford Motor Company (NYSE:F). At the time, I believed Ford was fighting an uphill battle primarily due to the unfavorable macroeconomic conditions creating a headwind. Interest rates continued to increase along with the new car prices reducing the affordability and ultimately the demand for vehicles. Further, I projected this environment to continue for the foreseeable future. Today, I continue to stand by my previous argument. Interest rates and new car prices are still at an elevated level with no clear signs of easing creating a significant headwind in terms of demand for Ford going forward. Moreover, I believe the challenges surrounding Ford have worsened with a likelihood of the situation getting worse. Consumer confidence has been declining with an expectation for consumer spending sharply declining in the coming months, which complements the high interest rate environment. Finally, the labor contract with United Auto Workers will likely degrade Ford’s long-term competitiveness as some of the company’s competitors are not restrained by the challenging labor contracts. Therefore, considering both the macroeconomic risks surrounding higher interest rates and weakening consumer financials along with the long-term risks regarding labor contracts, I continue to believe Ford is a sell.

Macroeconomic Conditions

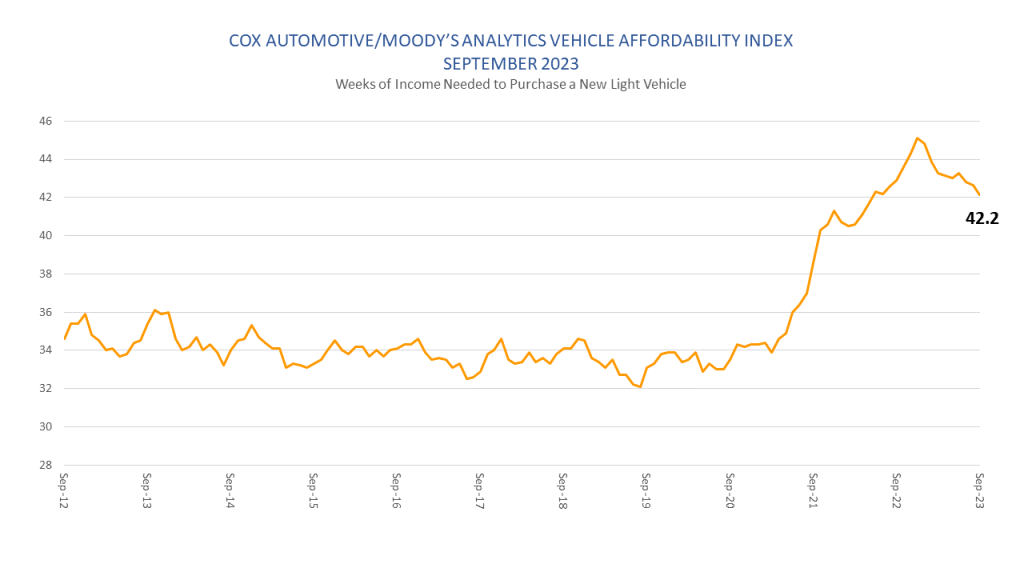

Macroeconomic conditions surrounding Ford have not improved. In fact, I believe it got worse. Starting with the new vehicle prices, according to the CPI data released by Bureau of Labor Statistics, the new vehicle prices increased 2.5% year-over-year with a monthly increase hitting 0.3% in the September month. The yearly increase in new car prices has indeed declined from 4.1% year-over-year at the time of writing my previous article, July, to 2.5% today, but investors must note that the growth in prices has only moderated instead of declining. As such, the new car affordability continues to be elevated compared to pre-pandemic times.

Cox Automotive

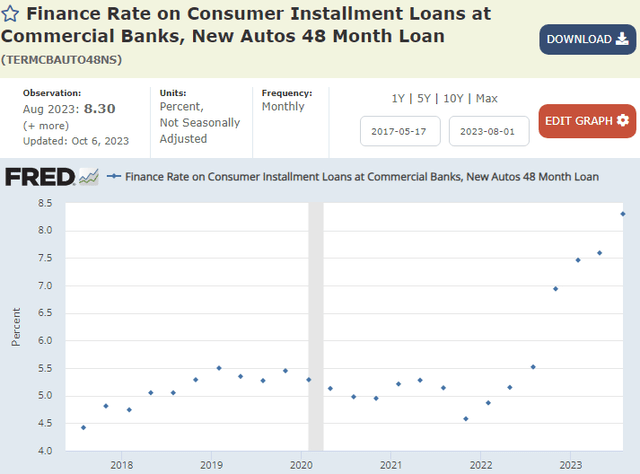

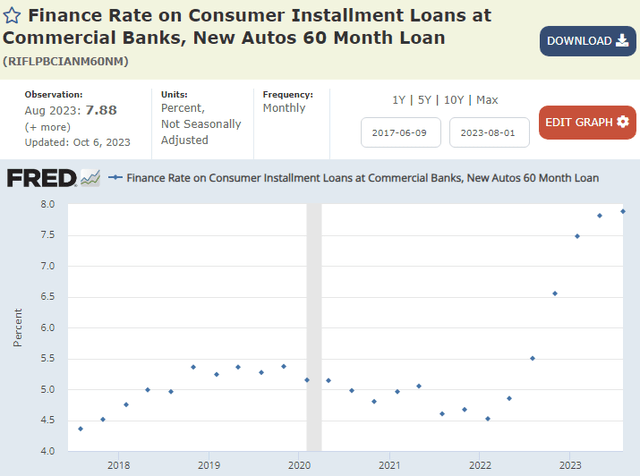

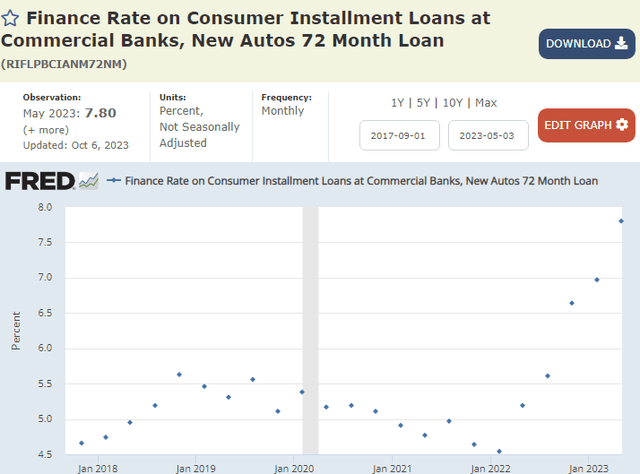

Beyond the price of the new vehicle, financing a vehicle continues to create challenges for potential buyers. The interest a consumer pays is dependent on each consumer’s unique situation, but the St. Louis Federal Reserve data, as shown below, shows that the average interest rate to finance a new vehicle has continued to increase in the past few months with no clear signs of moderating yet.

St. Louis Federal Reserve

St. Louis Federal Reserve

St. Louis Federal Reserve

As the charts above portray, the cost to finance a new vehicle for all lengths, 48 months, 60 months, and 72 months is continuing to increase creating a higher barrier to entry to potential consumers contributing to the macroeconomic headwinds for Ford Motor.

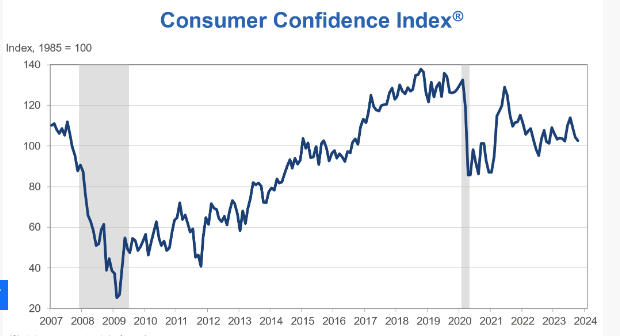

Further, likely as a result of higher costs, consumers’ financial health and consumer confidence have been declining potentially worsening the already straining environment for Ford.

Conference Board

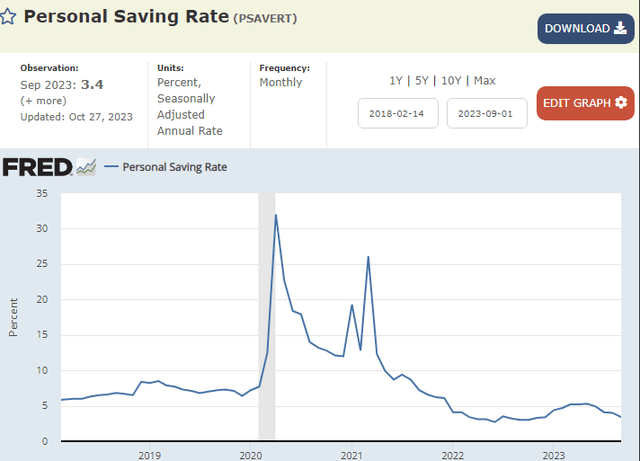

As the chart above portrays, the consumer confidence level has failed to recover to pandemic time highs or even pre-pandemic times. And, in recent months, consumer confidence has been showing signs of a decline. This could likely be the result of consumer finances worsening shown by the personal savings rate. As the chart below portrays, the personal savings rate is on a declining trend.

St. Louis Federal Reserve

Therefore, considering that the new vehicle prices and cost of financing a vehicle are continuing to increase along with the declining consumer sentiment and consumer financial health, I believe it is reasonable to argue that the macroeconomic conditions will create a headwind for Ford going forward, especially as the Federal Reserve chair Jerome Powell is still “not confident” that the Federal Reserve has done enough to bring the inflation down.

Labor Contract

In the past few months, United Auto Workers, UAW, and Detroit automakers including Ford have been negotiating a new labor contract, and the two parties have reached a deal. For will raise the base wage of its full-time employees by at least 25%, enact a ratification bonus of $5,000, increase contribution to 401K plan, and restore cost of living allowances for its workers. Further, Ford will invest $8.1 billion in a new plant.

The amendments to the new labor contract, in my opinion, significantly weakened Ford’s competitiveness in the automobile industry. Ford’s trailing twelve-month net income was about $6.16 billion; however, the new labor contract is estimated to cost the company about $1 to $2 billion annually for the four-year duration of the contract. This means that, at the midpoint, the effect on the company’s bottom line could be 25%.

Ford will either have to offset the increased costs through increased prices or accept a lower margin and weakened bottom line. So it is likely inevitable for the company to escape challenges going forward.

This situation, in my opinion, will significantly weaken the company’s competitiveness in the automobile market. General Motors (GM) and Stellantis (STLA) are also affected to a similar magnitude by the new labor contract; however, major competitors including Hyundai (OTCPK:HYMTF), Toyota (TM), Honda (HMC), Nissan (OTCPK:NSANY), Tesla (TSLA), and more are not affected. Therefore, these competitors will likely have a relative advantage in terms of pricing for the coming few years, which could degrade Ford’s bottom line or market share.

Valuation

The massive price declines in recent months brought Ford’s valuation multiple down. The company currently has a forward price-to-earnings ratio of about 5.34. The low valuation multiple may seem attractive; however, I do not think this is the case.

Looking forward to analysts’ estimates for Ford’s 2024 and 2025 earnings, the company’s EPS is expected to decline by 3.92% in 2024 and 0.38% in 2025. In other words, the company is not expected to see growth for the foreseeable future. As such, no matter the valuation multiple, unless there are signs that Ford could address and solve the current risks associated with the company, I believe there will not be a significant upside potential for Ford leaving the company with the risks discussed above. Therefore, despite the valuation multiple being low, I do not think it warrants a buy thesis.

Summary

Ford may be experiencing a perfect storm. The macroeconomic conditions are expected to create headwinds as the combination of rising new vehicle prices and financing costs are met with weakening consumer financial health and sentiment. Further, on top of the macroeconomic risks that have no clear signs of slowing, the company is facing higher labor costs that will exclusively affect Ford and a few of its competitors leaving the rest of the industry peers to be relatively free from the cost increases creating a relative weakness for the company likely degrading the company’s competitiveness. Therefore, despite the company trading at a low valuation multiple, as there are no clear signs of a turnaround from this situation for the foreseeable future, I continue to believe Ford is a sell.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here