")

Electrical System Control Cabinet

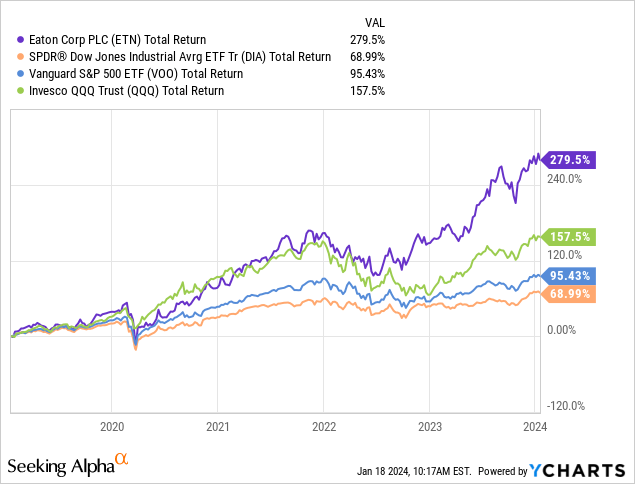

I am bullish on Dublin, Ireland based Eaton Corp. (NYSE:ETN) because the company is very well-positioned to benefit from the global secular bull-market in the electrical equipment supply-chain due to increased use of EVs, electronic devices, and data centers – the latter being primary due to migration to the cloud and the corresponding growth of AI and high-performance computing (“HPC”). All of these trends will require significantly more electric power generation and Eaton sells all the necessary electrical equipment necessary for electric power to be generated, fed to transmission-lines, distributed to homes & businesses, and eventually used by individual consumers. ETN stock has been on a roll:

As you can see from the graphic, over the past 5-years ETN has significantly outperformed the broad market averages as represented by the DJIA (DIA), S&P 500 (VOO), and Nasdaq-100 (QQQ) ETFs.

ETN stock has a relatively rich forward P/E=26.4x. Yet I rate ETN a BUY, and here’s why.

Investment Thesis

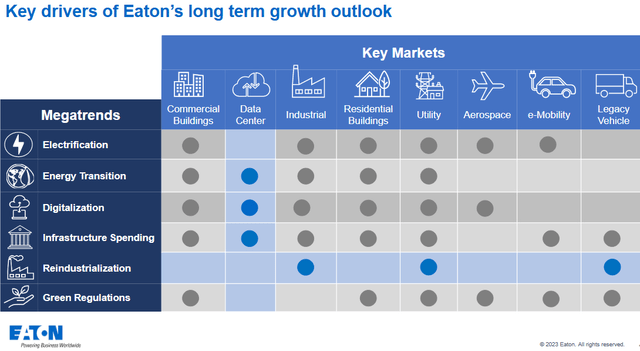

Eaton is a diversified industrial equipment manufacturer that specializes in electrical equipment, components, and systems. As the slide below from the Q3 presentation shows, that puts ETN in the cat-bird seat to supply growing demand from a plethora of key market opportunities:

Eaton

In particular, demand for ETN’s Data Center solutions will benefit from multiple “megatrends” while the “Re-industrialization” megatrend will positively impact multiple markets in which Eaton is a significant supplier of equipment.

From a high-level view, utilitydive.com reports that the U.S. electricity load growth forecast was recently increased by a whopping 81% (to 4.7% from the previous 2.6%) as compared to 2022 estimates. That implies that peak-demand could grow by a whopping 38 GW over the next 5-years. To put that into perspective for investors, that is equivalent to adding ~35 Vogtle nuclear power plants.

And, as an electrical engineer myself, I feel that forecast may actually still be too low. Indeed, at the Davos conference this week, AI rock-star Sam Altman said AI will consume vastly more power than people expect:

There’s no way to get there without a breakthrough. It motivates us to go invest more in fusion.

I think that the huge increase in Nvidia’s (NVDA) sales, primarily high-performance GPUs, is a signal that supports Altman’s opinion. My point is that, no matter what sources (nuclear, renewables, natural gas, etc) are used to generate the growing demand for more electric power in the coming years, Eaton is in a great position to benefit from the trend.

Earnings

Highlights from ETN’s Q3 earnings report (released on October 31st) are shown below:

- Record adjusted earnings of $2.47 (+22% yoy).

- Record quarterly sales of $5.9 billion (+11% yoy).

- Record quarterly segment margins of 23.6% (+240 basis pts yoy).

- Record operating cash-flow of $1.1 billion (+19% yoy).

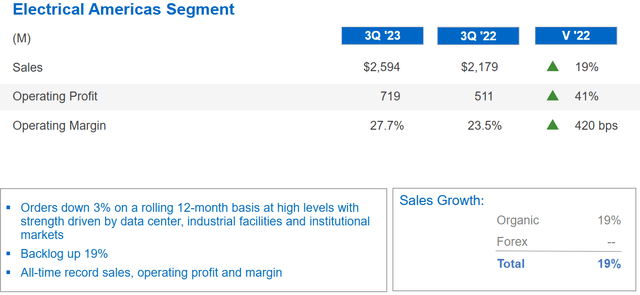

As you can see, from a financial performance perspective, ETN is hitting on all cylinders. The company is seeing particularly strong growth in Data Centers & Distributed IT, Utility, Commercial Aerospace, and EVs. ETN’s Electrical Americas Segment (its largest segment) demonstrated robust growth in sales and operating profit, with margin up a whopping 4.2 percentage pts yoy:

Eaton

Going Forward

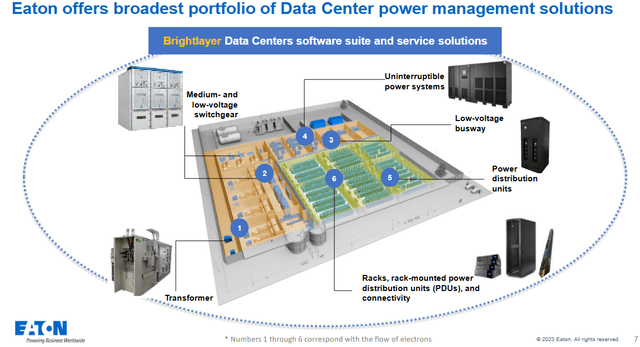

As mentioned in the ETN’s Q3 report referenced earlier, the company’s backlog at the end of the quarter hit $9.4 billion, which was +18% yoy, and +4% from Q2. That bodes well for continued strength this year, with top-line sales likely to grow in the 6-8% range on a yoy basis. The acceleration of AI in the data center arena provides the potential for an upside growth catalyst, one that could be significantly underestimated.

I say that because ETN has a strong, broad, and diverse set of power and equipment solutions in the data-center space:

Eaton

In addition, Eaton is well-positioned to benefit from the Biden Administration’s 2021 Infrastructure Bill, Inflation Reduction Act, and Chips & Science Act. All are accelerating investment in such key growth-areas such as EV charging networks, power grid expansion/hardening/modernization, as well as new clean-tech, battery, and semiconductor plants. Commercial aircraft production should also continue to ramp-up as defense orders grow and Boeing works through its seemingly never-ending issues with the new MAX jet.

Valuation

ETN’s midpoint for Q4 EPS guidance was for $2.44/share and operating margins of 22.5%; the midpoint of full-year FY23 earnings is $9/share. At the current pixel time price of $237.84, and the expected $9/share in earnings equates to a TTM P/E = 26.4x.

The Q3 dividend was $0.86, that was +6.2% versus $0.81 in the year earlier period. The current yield is 1.45%.

In Q3, ETN generated $913 million in free-cash-flow (+10% yoy). For FY24, ETN could easily deliver as much as $3.75 billion in free-cash-flow, or an estimated $9.39/share based on the 399.4 million shares outstanding at the end of Q3. That obviously bodes well for shareholders moving forward and indicates significant room for strong dividend growth as well as for significant share buybacks.

Note that ETN has been generating margins consistently above its original 2025 margin-expansion target and now appears to be on track to hit an operating margin of 23% by 2025, and it is quite possible the company could exceed 23% in FY25.

Summary & Conclusions

Investors looking for an opportunity to invest in the long-term secular growth opportunities based on the global electrification thesis should take a good look at Eaton. Unlike many of the much riskier commodity producers and EV manufacturers that investors typically use for investing in the electrification thesis, in my opinion, Eaton presents a relatively clearer line-of-sight toward increased returns and dividend growth. As mentioned at the beginning of this article, ETN stock has outperformed the broad major averages over the past 5-years, and I think it will continue to outperform the DJIA and the S&P500 over the next 5-years as well. ETN is a BUY.

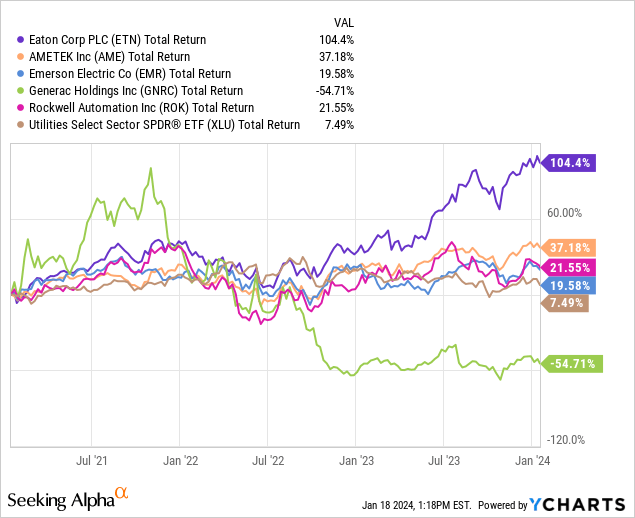

I’ll end with a 3-year total returns comparison of Eaton and some of its competitors in the electrical equipment sector: AMETEK (AME), Emerson Electric (EMR), Generac Holdings (GNRC), and Rockwell Automation (ROK) – as well as to the SPDR Utility ETF (XLU):

As you can see from the graphic, while all the equities used in the comparison should be benefiting from the same secular growth trends mentioned earlier in this article, Eaton has significantly outperformed them all. In my opinion, that is because ETN has a broader and more diverse set of solutions, a strong brand, and generates superior and consistent free-cash-flow as compared to the others.

Read the full article here