")

MaxLinear (NASDAQ:MXL) had a year to forget last year. MXL started 2023 strong with record earnings and in pursuit of a merger with Silicon Motion (SIMO). However, the merger got canceled and earnings collapsed as the year went by due to a downturn in the industry. However, MXL rallied into 2024, although it may be too early to say MXL has found the solution to the challenges it faces. In fact, there are several reasons why the stock is likely to head lower in the short term, which is why standing on the sidelines by staying on hold is worth taking into consideration. Why will be covered next.

Why MXL dodged a bullet with SIMO

A past article from one year ago rated MXL a hold after concluding that MXL could be better off by not going through with the SIMO acquisition for a number of reasons. For instance, there was reason to believe MXL was heading for lean times due to a downturn in semiconductor demand, which would inevitably hit earnings and, by extension, the ability to pay off the debt MXL would have to take on in order to finance the acquisition of SIMO.

As it turned, MXL came around to the idea of not going through with SIMO because MXL decided to terminate the merger agreement with SIMO in July 2023, about 14 months after MXL made public its intention to pursue a merger with SIMO in May 2022. MXL cited several reasons in its statement for the termination, including material breaches of the merger agreement by SIMO. This is, however, in dispute, especially in light of the timing of the termination, including by SIMO itself.

Keep in mind the merger was supposed to have been wrapped up a lot sooner, but regulatory approval from China turned out to be a hurdle. China eventually granted approval in July 2023, which cleared the way for the merger to be completed, but MXL’s termination of the merger shortly afterwards put an end to it. Still, the delay meant that the environment in which the merger was to be completed had become very different from the one when it was first contemplated.

The semiconductor industry had entered a downturn, which was especially pronounced in the market for memory chips. This affected everyone along the food chain, including SIMO as a supplier of SSD controller chips. Both SIMO and MXL have been impacted, but MXL dodged a bullet because if the merger had been completed as scheduled, MXL would now find itself in much worse position for several reasons, including having to deal with a mountain of debt at a time when its ability to service debt is severely curtailed.

China’s delay in granting approval was thus a blessing in disguise for MXL. It prevented completion of a transaction, which would have put MXL in much worse position than it is right now, MXL would have essentially overpaid to acquire an asset at a bad time. MXL still has to deal with the consequences of the failed merger with SIMO, including arbitration initiated by the latter for compensation, but the alternative would have been so much worse. The previous article from January 2023 was prescient in arguing against the merger with SIMO.

The decline in the stock has ended or has it?

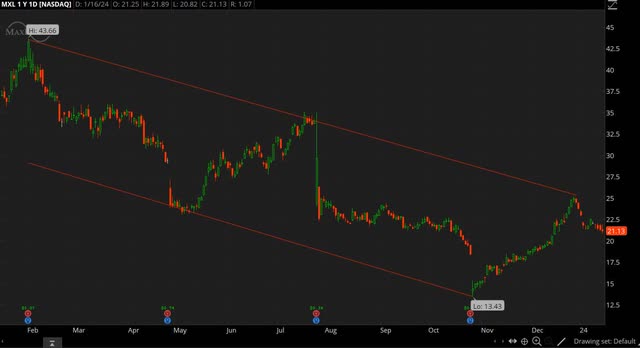

The process of arbitration is unlikely to be completed for another 1-2 years. It may, for instance, lead to MXL having to pay SIMO a breakup fee of $160M or nothing at all, depending on arbitration. In the meantime, MXL has to deal with other issues at hand. The stock, for instance, has gradually declined ever since the peak in late 2021. The stock reached as high as $77.89 in December 2021, which is ten times what it was worth 21 months earlier when MXL bottomed in March 2020 at $7.79.

The stock has fallen since then, but at the same time, it’s worth noting how the stock has rallied after hitting a 52-weeks low of $13.43 on October 26, 2023. This translates to a gain of an impressive 57.3% in less than three months since the stock closed at $21.13 on January 16. Keep in mind that if the stock had not pulled back in recent days after hitting a high of $25.14 on December 27, gains could have been as much as 87.2%.

Source: Thinkorswim app

The question that comes to mind is whether the recent rally has any legs to it or whether the rally was a temporary bounce and the slide continues. It’s therefore worth mentioning that the stock is still leaning bearish despite the recent rally as shown in the chart above. Both the lows and the highs are trending lower, something that points in the direction of lower stock prices.

There may be another reason as to why a move lower is in the pipeline. As mentioned earlier, the recent rally topped out after hitting a high of $25.14 on December 27, followed by a decline in the stock. This December 2023 high was preceded by the July 2023 high of $35.09 and the February 2023 high of $43.66, all of which were followed by declines in the stock as shown in the prior chart.

What’s interesting to note is that all three highs correspond very closely to Fibonacci levels. For instance, the 50% Fibonacci retracement of the uptrend, starting from the March 2020 low of $7.79 to the December 2021 high of $77.89, is $42.84, which is close to the February 2023 high of $43.66. Similarly, the 61.8% Fibonacci retracement of the aforementioned uptrend is $34.57, which is close to the July 2023 high of $35.09. The 76.4% Fibonacci retracement is $24.33, which is close to the December 2023 high of $25.14.

This suggests the reason why the stock topped out in February, July and December to decline each time afterwards is because that is when and where it encountered resistance. If this is correct and there is indeed resistance in or around the $24-25 region, then the path of least resistance may be for the stock to head lower since the path higher is blocked. This may lead to a retest of the October 2023 low of $13.43. The stock could go even lower taking into account the prevailing trend.

Why the upcoming earnings report could power the stock lower

It’s no coincidence the stock hit the 52-weeks low of $13.43 after a 22% drop on October 26 because that was the day following the release of the Q3 FY2023 report on October 25. In fact, the stock sold off after each of the four quarterly reports in 2023. The most recent report missed estimates for the top and the bottom line and guidance was worse than expected due to demand not improving as MXL had previously suggested it would.

The consensus expected MXL to report non-GAAP EPS of $0.04 on revenue of $139.7M, but MXL reported non-GAAP EPS of $0.02 on revenue of $135.5M. In terms of GAAP, MXL reported a loss of $39.8M or $0.49 a share. The table below shows how the numbers declined in Q3 FY2023 compared to preceding quarters.

|

(Unit: $1000, except EPS) |

|||||

|

(GAAP) |

Q3 FY2023 |

Q2 FY2023 |

Q3 FY2022 |

QoQ |

YoY |

|

Revenue |

135,530 |

183,938 |

285,730 |

(26.32%) |

(52.57%) |

|

Gross margin |

54.6% |

55.9% |

58.6% |

(130bps) |

(400bps) |

|

Income (loss) from operations |

(17,818) |

(5,937) |

51,948 |

– |

– |

|

Net income (loss) |

(39,829) |

(4,351) |

28,408 |

– |

– |

|

EPS |

(0.49) |

(0.05) |

0.35 |

– |

– |

|

(Non-GAAP) |

|||||

|

Revenue |

135,530 |

183,938 |

285,730 |

(26.32%) |

(52.57%) |

|

Gross margin |

60.8% |

61.0% |

62.0% |

(20bps) |

(120bps) |

|

Income (loss) from operations |

7,317 |

29,753 |

96,730 |

(75.41%) |

(92.44%) |

|

Net income |

1,810 |

27,899 |

84,068 |

(93.51%) |

(97.85%) |

|

EPS |

0.02 |

0.34 |

1.05 |

(94.12%) |

(98.10%) |

Source: MXL

MXL had earlier suggested an improvement in Q4 was forthcoming with Q3 the trough, but Q4 guidance was weaker than expected with a QoQ decline as shown below. In fact, MXL had once suggested Q3 would present an improvement, which did not pan out either.

“I think we’re always conservative about how these things rebound. So, I mean, I think a modest improvement in Q4 would be where my expectations are.”

The consensus is that MXL will report non-GAAP EPS of $0.01 on revenue of $126.2M in Q4 FY2023 when it reports next, most likely in early February.

|

Q4 FY2023 (guidance) |

Q4 FY2022 |

YoY (midpoint) |

|

|

Revenue |

$115-135M |

$290.6M |

(56.99%) |

|

GAAP gross margin |

52.5-55.5% |

56.2% |

(220bps) |

|

Non-GAAP gross margin |

59.5-62.5% |

59.6% |

140bps |

Source: MXL

MXL is projected to earn $1.11 in FY2023, which translates to a non-GAAP P/E ratio of about 19 with a stock price of $21.13. In comparison, MXL earned $0.88 in FY2020, which implies a CAGR of 8.05% in FY2020-2023. If we extrapolate this rate of growth to the coming years and assume EPS continues to grow by 8.05% on average like in the past three years, then an argument can be made that fair value for MXL is around $8.94.

Guidance did not extend into Q1 FY2024, but excess inventories are likely to still be around. From the Q3 earnings call:

“I mean, there’s definitely more inventory. We saw more push outs. I mean, we saw bookings in the quarter. So we saw some improvements, but it wasn’t as much as what we had originally expected three months ago.

Honestly, we ourselves are sort of baffled if you will as to how much inventory is out there and just slow down and how to reconcile that.”

Investor takeaways

MXL is not doing that well lately, but an argument can be made that MXL lucked out with the SIMO saga because the company would be in much worse shape if SIMO had been acquired as proposed. MXL may still have to pay a breakup fee to SIMO, but the alternative would be much worse, including billions of debt to service at a time when earnings are way down.

The SIMO acquisition is no more, but MXL still has to deal with a slump in demand that has seen, for instance, earnings drop from $0.74 in Q1 to an expected $0.01 in Q4. MXL had once suggested the downturn would bottom out in H1 and Q3 and Q4 would show improvement, but neither turned out be correct.

MXL has been rather shaky in terms of its ability to accurately gauge the state of market demand recently. MXL was forced to go back on previous statements, which does not inspire confidence. The most recent guidance calls for a QoQ decline instead of an increase suggested earlier. The outlook also suggests there is still a lot of inventory out there that has yet to be used, which implies demand will remain in a slump for some time.

Charts are not infallible, but they do point to lower stock prices being in store. The trend has been for the stock to go down, temporary rallies notwithstanding. The latest rally came about without any real change at MXL, which raises doubts about its sustainability. While the recent rally in the stock is impressive, it does not change the direction of the prevailing trend. MXL went on similar rallies in the past, only to see the stock proceed to hit new lows. This might happen again with the rally into 2024.

I am neutral on MXL in light of all the above. A trip back to the low teens is not out of the question. MXL is scheduled to report next month and that may be the catalyst to get there. The last four reports were followed by selloffs in the stock. Odds are another one is coming.

Read the full article here