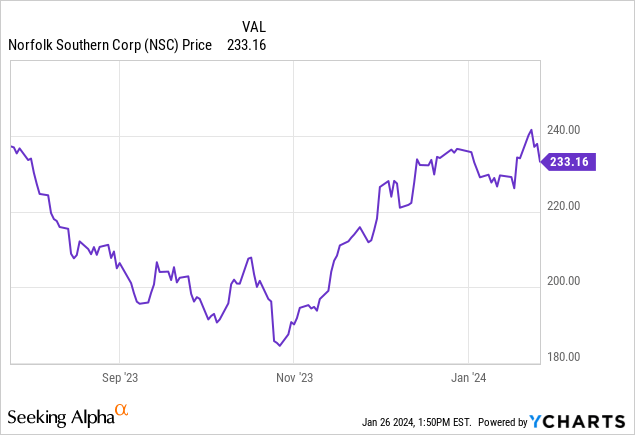

Norfolk Southern Corporation (NYSE:NSC) is a stock that we covered at our investing service for a trade, initiating in mid-September and completing the position within a few weeks into October. We offloaded at $220 for trading gains. As a number of our traders are now holding a house position with portions of the profit, the just-reported Q4 earnings were of interest.

Frankly, they left something to be desired. We rate Norfolk Southern shares a hold, as rail data has been softening, but the company navigated a tough and transformational year with macro pressures. Let us discuss the Q4 earnings.

Right now, the economy continues to be resilient, but Norfolk Southern Corporation is still facing some headwinds. The thing is, rail data looks like volumes are falling badly. The stock had a nice bounce from our buy call and hit our exit in December. Long term, there is an upside in a strong economy, but the economy is softening a bit. Perhaps a softish landing, but the economy, while resilient, is not on fire. The market is stretched, too, and the Q4 earnings season has been unimpressive. Norfolk Southern’s fourth quarter showed some key strengths and weaknesses.

First, revenues were down from the year-ago quarter. Operating revenues were $3.1 billion, down $164 million, or 5%, compared to Q4 2022. For the year operating revenues were $12.2 billion in 2023, also down 5%, or $589 million, compared with 2022. Total volume came in at 6.7 million units, a 1% decrease from 2022. Volume declines were most significant in intermodal and energy-related chemical commodities. On the positive side, lower ocean freight rates, advanced demand for international intermodal, and rising vehicle production activity drove growth in the automotive franchise, both of which contributed meaningfully to offsetting larger declines.

Factoring in operating expenses, Q4 net income was $808 million. However, there was a $150 million charge associated with the Eastern Ohio derailment from last year, so this was a 32% decline compared to $1.2 billion a year ago. If we make adjustments for the costs associated with that incident, we still see a 19% decline in income to $958 million, dropping 19%. Adjusted EPS for the quarter was down 17% to $2.83. For the year, operating expenses were $8.2 billion (controlling for the accident in Ohio), which were up 3% compared to 2022. This is an issue when revenues were down, so margins were crimped, leading to 2023 income lower than in 2022. Adjusted income was $4.0 billion, down 18% compared to 2022, while 2023 adjusted EPS was $11.74, falling 15% from 2022.

As we move ahead to 2024, we expect management to focus on controlling operational costs. We are most interested in seeing if the railroad can boost cash flow. This was a big problem in 2023. In 2023, free cash flow was $1.4 billion lower than the prior year, representing the impact of the $650 million derailment-related costs, as well as the lower operating income, coupled with higher CAPEX. We do like the ongoing shareholder-friendly nature of the company, with $1.8 billion in return to shareholders, with about two-thirds being driven by the dividend and the remainder from share repurchase activity.

The company did issue debt in November to boost the cash on the balance sheet to $1.6 billion at year-end. This will be used to fund the strategic Cincinnati Southern Railway acquisition, scheduled to close in March of this year. However, this will mean the company will face higher interest expense in 2024 than in 2023, and to make matters a bit more precarious, the repurchase activity will cease as this purchase is done.

Make no mistake, the acquisition is a key artery for the railroad, so it will increase operational efficiency and offer synergies. Management sees modest volume growth in 2024. In merchandise markets, overall volume growth is expected to be driven by gains in steel shipments while automotive will grow on continued strength in vehicle production, including new EV business. Over in the intermodal business, they see international trade improving, which will boost demand for domestic and international services.

However, weakness in the consumer could pressure growth if the economy softens meaningfully later this year. It is a real risk. And there is still of course coal activity for railroads. For 2024, management sees flat volume levels compared to last year for coal. Demand for export coal is forecasted to be high. In the merchandise market for 2024, strong pricing conditions are expected, but there is a weak truck market that will hurt intermodal prices.

In terms of fiscal performance, we are looking for 1-4% growth in revenue from 2023, while management sees about 3%. This growth will still be below 2022 results. Perhaps the biggest disappointment is that EPS will fall again in 2024. Net income and EPS growth will be weighed down by higher interest expense and no share repurchases. That said, H2 2024 should see a bit of a ramp-up as rate cuts should spur some economic activity.

Overall, we are in a wait-and-see approach for Norfolk Southern Corporation. We had a very nice gain on a rapid-return trade. For the long term, we would hold, collect the dividend, and wait for improving conditions. Integration of CSR will be a long-term benefit, though it comes with short-term costs that will weigh on 2024 performance.

Read the full article here