")

I have written eight articles on Iron Mountain (NYSE:IRM) dating all the way back to June of 2017. All eight were bullish. This will be my first bearish piece on IRM.

The company has not changed.

The valuation has.

IRM’s market price seems to be driven by narratives which have caused mispricing in both directions.

Changing narratives

From 3-7 years ago, the overriding narrative on IRM was that it was risky due to its reliance on physical paper storage. The idea was that usage of paper for documentation was going away and since IRM got most of its revenue from storage and shredding of paper documents its revenues were at risk.

Due to this narrative, IRM traded at a very cheap multiple. Despite its AFFO/share growth, it was viewed as a declining asset.

Around three years ago, the narrative on IRM shifted. Its burgeoning data center division took center stage. Rapid development and lease-up of data centers began to drive growth for IRM and the market started to price IRM at a data center multiple. The price gains accelerated as artificial intelligence became synonymous with data centers.

S&P Global Market Intelligence

In the last three years, public perception of IRM went from an outdated physical paper company, to a cutting-edge AI company.

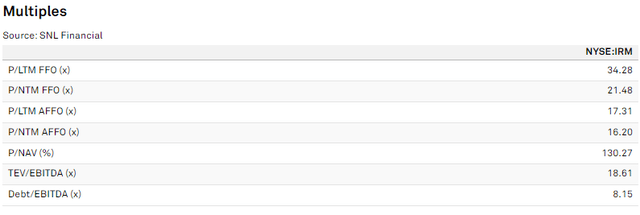

The AFFO multiple went from around 10X to 17X.

S&P Global Market Intelligence

Note that there are some improper items in the AFFO calculation and if we correct it to true earnings, the multiple is actually 24X today (more on this later).

In this article, I intend to demonstrate that IRM is neither a paper company nor a cutting-edge AI play.

The narratives went way too far in both directions and resulted in opportunistically cheap pricing 3-7 years ago and overvaluation today.

Actual Iron Mountain Business

Iron Mountain’s actual business has not changed much. It has always been an information management company. It adapts to whatever form its customers need their information with IRM’s main expertise being an extraordinary sense of organization and security.

IRM partners with just about every large company on the planet including nearly all of the Fortune 100 to protect and retrieve their data. Customers pay for this service because the speed and organization of IRM’s information retrieval facilitates their workloads.

As far as I can tell, this sort of service is equally valuable to the customer whether the data is on paper documents stored in an IRM warehouse or digitally stored in an IRM data center.

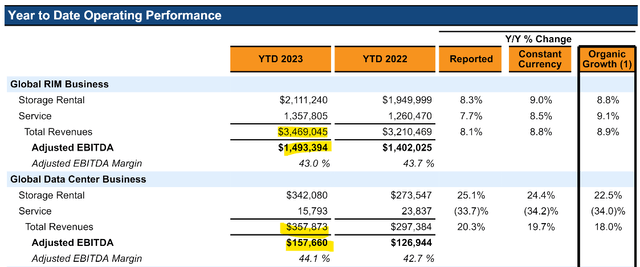

While the data center business is growing rapidly, the company is still close to 90% physical storage in terms of EBIDTA generation. Note the $1.5B of “Records Information Management” EBITDA which is their term for the paper and other physical storage legacy business.

IRM

This compares to $158 million in data center EBITDA.

Thus, I find it hard to justify pricing IRM as a data center or AI play when the vast majority of its business is still physical.

That said, I also don’t believe that data center or AI is necessarily better than the old tech business. Margins are almost identical in the low to mid 40% range and both businesses are growing nicely organically.

Iron Mountain’s operations and growth

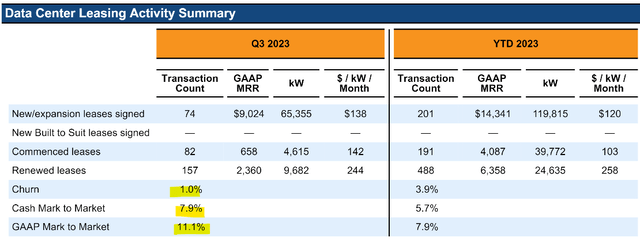

Over the last seven years, IRM has demonstrated operational excellence. Renewal rates on its existing business are extremely high indicating happy customers and these happy customers are becoming data center customers.

This shows up in superior lease-up of data center space even as compared to pure-play data center companies. The pace of new lease-up has been impressive with 65,355 kW of new leases in 3Q23.

IRM

Also impressive is the low 1% churn and 7.9% cash mark to market on renewals. Data centers have often struggled with mark downs on renewals so this being a positive number already sets it above Digital Realty (DLR).

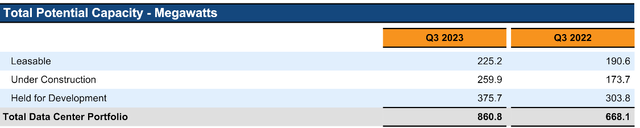

IRM is rapidly expanding its data center footprint with 259.9 megawatts under construction and another 375.7 megawatts ready to be developed.

IRM

Note that the pipeline is almost 200 megawatts larger than it was just a year ago.

Perhaps it is the pace of this growth that inspired the narrative.

We also find the growth impressive and have long thought IRM is a great company. Our sticking point today, and why we have sold our shares, is valuation. To get a better sense for IRM’s current valuation let us begin by correcting reported AFFO to get to a truer earnings number.

AFFO to true earnings

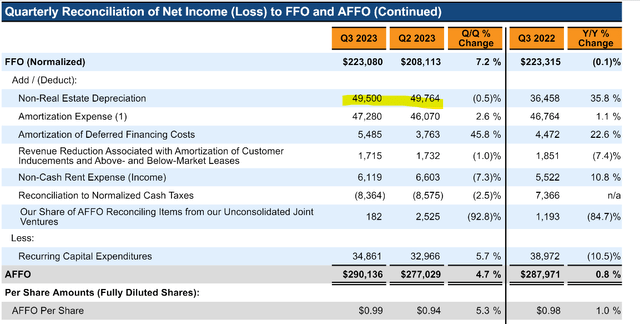

AFFO in 3Q23 was $0.99 per share.

Supplemental

There are a number of addbacks which we do not think represent true earnings.

In reconciling normalized FFO to AFFO IRM adds back $49.5 million of non-real estate depreciation.

As REIT analysts we are very familiar with adding back depreciation and usually such addbacks are kosher. Buildings tend to appreciate or at least maintain value over time so the accounting depreciation is not a real expense.

In this case, however, this is the non-real estate portion of depreciation and primarily related to IRM’s vehicle fleet. As we all know, vehicles lose a significant portion of their value the second they are driven off the dealer’s lot. Vehicular depreciation is a real expense.

Thus, I would subtract $49.5 million from AFFO.

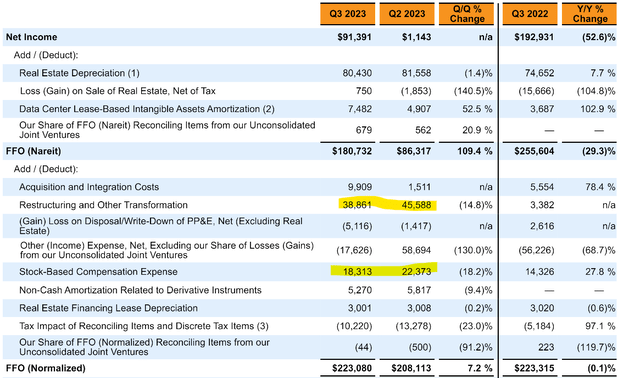

There are also some improper addbacks to get to normalized FFO. Share based compensation resurfaces as my perennial gripe.

Supplemental

Share compensation dilutes investors making it a real expense in this case to the tune of $18.3 million in 3Q23.

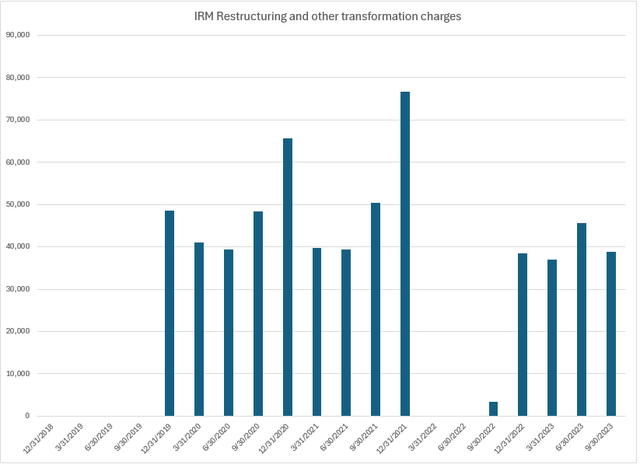

Finally, we get to the restructuring and transformation costs of $38.8 million. Such costs are often added back because they are viewed as one time in nature. For Iron Mountain they seem a bit more recurring to me.

S&P Global Market Intelligence

This company likes its transformations going from Project Summit to Project Matterhorn.

These restructurings do indeed make sense in the long term as IRM is leaning its operations, but given that this non-recurring expense has appeared in about 15 quarters I would say it is at least partially recurring.

Thus, we will deduct $20 million from AFFO to get to true earnings.

In total, adjustments are:

- -$18.3 million stock comp

- -$20 million restructuring

- -$49.5 million non-real estate depreciation

That takes AFFO for the quarter from $290 million to $202 million.

True AFFO runrate is about 70% of what is reported which means the multiple is significantly higher than 17X.

We calculate AFFO run rate at $2.78 which implies a multiple of 24X.

Clean accounting

Please note that while we do not believe reported AFFO is representative of true earnings, there is nothing improper about it being reported in this fashion. It is extremely standard for companies to have their own AFFO calculations as it is a non-standardized metric.

Similar adjustments would need to be made for any company. IRM fully discloses all line items and makes it very clear how it can be reconciled to GAAP numbers. To my knowledge IRM’s accounting is 100% clean.

Iron Mountain’s Stock Valuation

Presently, the average REIT trades at 15.9X 2024 AFFO.

Certain characteristics lend themselves to certain multiples. REITs that trade above the average multiple should have superior growth, reduced risk or some combination of the two.

Thus, to justify IRM’s 24X multiple on true earnings, it would need to have these characteristics.

Its growth rate is indeed above average in my base case scenario which is steady moderate growth in the RIM business along with rapid growth from data center development.

On the risk side, however, I see IRM as above average risk for three reasons:

- Data centers are subject to oversupply given fairly low barrier to entry.

- While not my base case, there is a material chance that paper could still go away which would slow or even cause negative growth in RIM.

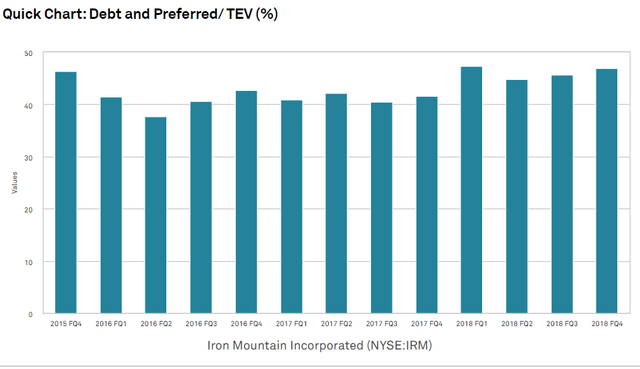

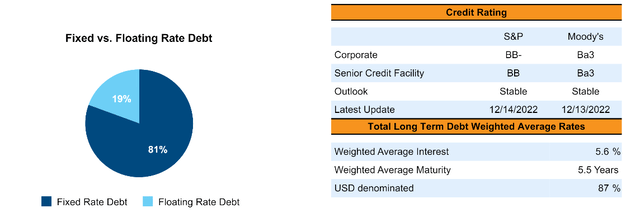

- High leverage

IRM, unlike most REITs, does not own a significant portion of its properties. On top of a normal amount of REIT leverage, they have lease obligations which take overall liabilities to nearly 50% of enterprise value.

S&P Global Market Intelligence

This higher level of leverage comes with a worse credit rating (BB- on corporation) and higher interest expense at 5.6% average cost of debt.

IRM

Looking at the combination of slightly above REIT growth rate and above REIT average risk, I think IRM should trade approximately in-line with the REIT average multiple.

At the current run-rate, IRM is trading at 24X AFFO which is a larger premium than I think is warranted.

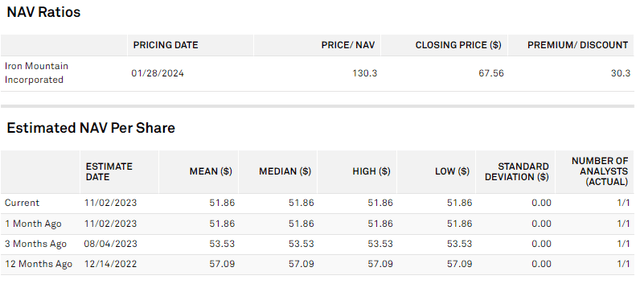

IRM also looks overvalued from an NAV perspective. In an environment where most REITs are trading significantly discounted to net asset value, IRM is at 130% of NAV.

S&P Global Market Intelligence

The bear thesis

While Iron Mountain remains a well-managed company with significant growth potential, the massive rise in its market price has made it overvalued. If and when IRM’s valuation comes back down to Earth, I would happily consider buying back in.

Read the full article here