")

Verona Pharma plc (NASDAQ:VRNA) has submitted a marketing application to the US FDA for its drug ensifentrine, for the maintenance treatment of chronic obstructive pulmonary disease (COPD). This article takes a look at some of the bull and bear case points for VRNA.

The Phase 3 studies

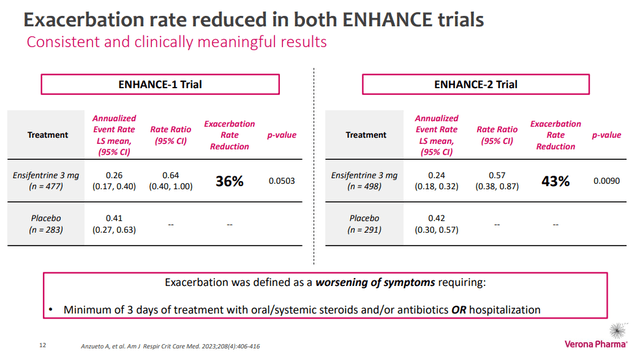

Ensifentrine, an inhibitor of phosphodiesterase 3&4, produces both an anti-inflammatory effect and bronchodilation. Ensifentrine demonstrated its potential in COPD across several studies, notably the phase 3 ENHANCE studies. In ENHANCE-1 (n = 763 patients), treatment with ensifentrine significantly improved lung function relative to placebo, as measured by forced expiratory volume in one second (FEV1). With regards to moderate to severe COPD exacerbations over 24 weeks, ensifentrine produced a 36% reduction compared to placebo patients. Unfortunately, this difference was just short of statistical significance (p = 0.0505). In ENHANCE-2 (n = 789 patients), however, this reduction in moderate to severe COPD exacerbations over 24 weeks, was 42% and was significant (p = 0.0109).

Figure 1: Results from the ENHANCE studies with regard to COPD exacerbations. Note this was not the primary endpoint. (VRNA Corporate Presentation, January 2024.)

Regarding the control/placebo group in the studies, that group took nebulized placebo twice a day, rather than nebulized ensifentrine twice a day. However, patients in the ENHANCE studies could be on a background COPD therapy, so many of the patients in the control group weren’t completely untreated. Indeed, in ENHANCE-2, VRNA noted that 52% of subjects received a long-acting muscarinic antagonist (LAMA) or a long-acting beta-agonist (LABA). Only 15% of all subjects were receiving an inhaled corticosteroid (ICS) in addition to the LABA or LAMA. In ENHANCE-1, 66% of patients received a LAMA or LABA and 21% received an ICS with their LAMA or LABA.

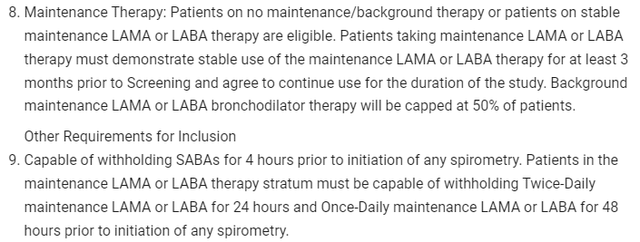

Notably, the inclusion criteria for both ENHANCE-1 and ENHANCE-2 capped the number of patients on background therapy, although the cap doesn’t appear to have been stuck to, and state that patients on a LAMA or LABA need to be able to withhold use of those drugs prior to spirometry. These features might be standard, but a design where ensifentrine has to beat a control group that has optimal background therapy in all cases would be better, in my opinion. Of course, VRNA’s trial design is influenced by the outcome of discussions with the regulator, and there is no point arguing about the marketing package if you can’t get the regulator to approve the drug first. As such a design that satisfies the regulator is a must. Still, I doubt the FDA would’ve disagreed with the idea of a third study with an even higher hurdle in terms of the control group being mandated an optimal therapy (perhaps LAMA/LABA with an ICS).

Figure 2: Screenshot of part of the inclusion criteria from ENHANCE-2 (NCT04542057) (Clinicaltrials.gov entry for ENHACE-2.)

My opinion: VRNA could have produced a more impressive marketing package, perhaps by adding on another phase 3 study. Nonetheless, the company will be running further trials with ensifentrine so it still has the chance to build the marketing package. That being said, if VRNA’s New Drug Application (NDA) isn’t approved, I don’t think that would be because of efficacy studies, I see them as sufficient. I do want the drug on the market for COPD.

Buyout potential

VRNA announced it had submitted a NDA to the US FDA for ensifentrine for the maintenance treatment of patients with COPD on June 27, 2023. VRNA announced the application had been filed on September 11, 2023, and noted a Prescription Drug User Fee Act (PDUFA) target date of June 26, 2024. At the time of writing then, that date is 132 days away.

Of course, there could be a buyout prior to approval, or indeed after. In late 2023, GSK plc (GSK) was said to be looking to make acquisitions, especially in respiratory and autoimmune diseases. However, on January 9, 2024, GSK announced that it was acquiring Aiolos Bio, a company with a drug for respiratory and inflammatory conditions. That acquisition seems to reduce the odds of GSK acquiring VRNA, unless GSK wants to build out its business further in the respiratory arena.

My opinion: The end of 2023 and the start of 2024 have produced plenty of M&A in biotech, so I don’t think a buyout is off the table.

Patent suite

Ensifentrine itself was invented a while ago and the composition of matter patent has expired. Nonetheless, the company still has various other patents covering the drug, one of which is the polymorph patent. Polymorph patents covering crystalline forms of the drug can be used to create a real headache for generic manufacturers seeking to launch a generic drug. Indeed, VRNA’s polymorph patent has an estimated patent expiry of 2031, according to the company’s January 2024 corporate presentation (slide 33). Further, the company notes up to 5 years potential patent term extension on select patents. Further, there is also regulatory exclusivity to consider in the US and Europe, which would allow many years of sales unencumbered by generic competition.

My opinion: Overall, when a composition of matter patent has expired, it becomes a little hard to refer to a patent portfolio as obviously rock solid, but there isn’t a lack of ability for VRNA to protect its market exclusivity.

Financial Overview

VRNA had cash and cash equivalents of $257.4M as of September 30, 2023. R&D expenses were $3M in Q3’23 and SG&A expenses were $13.4M in the same quarter. Net loss was $14.7M for Q3’23 and net cash used in operating activities was $39.8M in the first nine months of 2023. VRNA also had $19.9M outstanding on its term loan from Oxford Finance at the end of Q3’23. At the time of Q3’23 earnings, VRNA believed its cash, expected receipts from a UK tax program and the $130M it would be able to draw under the debt facility with Oxford would be sufficient to fund the company to the end of 2025 at least. Indeed, at the rate of burn in the first nine months of 2023, VRNA would have over four years of cash left. That being said, the rate of burn in the first nine months of 2023 isn’t a good estimate of cash burn going forward if ensifentrine is approved. Cash burn would surely pick up launching a drug, but I don’t find VRNA’s near-term cash burn to be a concern in any case.

On January 2, 2024, VRNA announced it had entered into a debt facility of up to $400M to replace its existing $150M facility. VRNA has already drawn $50M and can draw another $100M on the approval of ensifentrine, a further $150M can be drawn upon achievement of sales milestones and a further $100M if the lenders approve. The interest only period is 53 months and the $20M drawn under the original loan facility and the fees/costs can be paid at the closing of the debt facility. Taking all this together, VRNA has pro forma cash and cash equivalents of $307.4M, and ~$70M in debt outstanding on its loan.

VRNA had 639,520,054 ordinary shares outstanding as of October 27, 2023, but the stock trades on the NASDAQ as American Depository Shares, with each ADS comprised of 8 ordinary shares. As such, there could be up to 79,940,007 ADS outstanding, where all shares in ADS form. VRNA thus has a market cap of $1.36B ($16.96 per share). As of September 30, 2023, there were also 23,022,304 ordinary shares worth of stock options outstanding and 22,912,248 ordinary shares worth of restricted stock units outstanding.

Summing up

I think VRNA is a great drug with ensifentrine. From a trading viewpoint, VRNA is trading with an enterprise value of $1B+ already and their NDA hasn’t been approved. There is always the risk of a complete response letter (CRL) due to an issue with chemistry, manufacturing and controls. I’m not expecting a CRL, I’d actually predict approval, but there is room for the stock to fall if a CRL delays entry to the market.

A further risk is that once the drug enters the market, there is already competition there, and at least some of the competition has once daily dosing, not twice a day dosing like ensifentrine. Ensifentrine of course, has its own advantages, like a distinct mechanism of action that makes it an obvious choice for those not responding well to other drugs. Nonetheless, the point is ensifentrine doesn’t get the potential $10B COPD maintenance market to itself. As such, initial sales might not be huge.

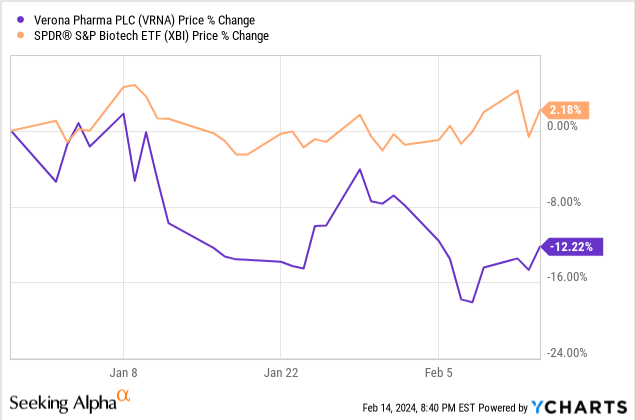

While VRNA rallied with the biotech sector in late 2023, year-to-date, biotech is trading sideways while VRNA is trading down. For a company with a PDUFA date in June, any run-up into a potential approval doesn’t seem to be happening in the first month and a half of 2024.

In the near term then, there is no trade on VRNA that seems particularly strong to me. I rate VRNA a hold, but I’d certainly consider changing that to a buy closer to the PDUFA date.

Read the full article here