Over the past year or so, there has been a flurry of merger and acquisition activity in the oil and gas exploration and production market. What’s interesting is that, despite having many different oil and gas producing regions across the nation, both onshore and offshore, one small region has been the source of much of all that has transpired. That’s none other than the prolific Permian basin, which is located throughout parts of Texas and New Mexico. This raises some interesting questions. For instance, why is all of this going on in the Permian? Will this kind of activity continue? What kind of prospects could there be for investors to focus on? And so much more.

In what follows, I will try to answer these questions as best I can. The fact of the matter is that the Permian is a massive playing field for the oil and gas exploration and production industry. The number of large transactions that have occurred as of late and that the number of potential deals moving forward is certainly lower than it was a year ago. However, I would argue that there’s plenty of potential for investors who believe that further industry consolidation will take place. Furthermore, it’s likely that the Permian basin, more so than any other basin, will continue to be a significant source of shareholder value creation for many years to come, though the ride along the way is certain to be bumpy.

Why the Permian?

Author – EIA

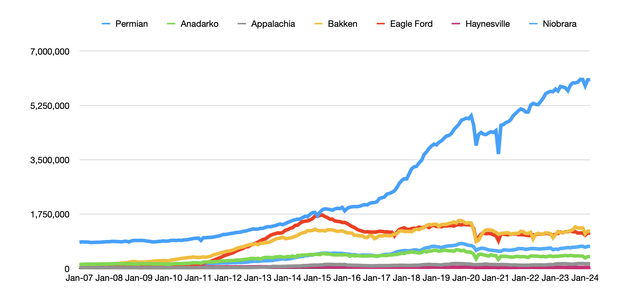

Seventeen years ago, there was nothing that was terribly special about the Permian basin. At that time, we were seeing a lot of drilling in multiple basins across the country. However, output from the Permian, while larger than it was in any of the other basins, stood at less than 850,000 barrels of oil per day. But significant investments have worked wonders in that region. It has been estimated, for instance, that for March of this year, total production from the region will be roughly 6.09 million barrels per day. That’s an increase of over 620% in the course of a decade.

Author – EIA

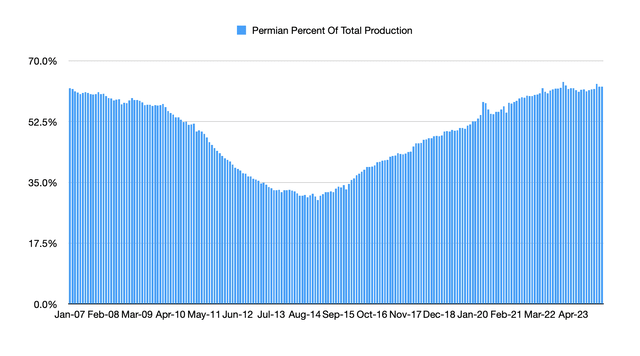

It’s worth noting that, relative to the other major oil producing regions that the EIA tracks regularly, the Permian has come, over the past few years, to account for an even larger share of total output from the regions in question. Seventeen years ago, more than 60% of all the oil that was extracted from the seven largest oil and gas producing regions in the country came from the Permian. Shortly after that time, as other regions started ramping up output and, later, as US energy production tumbled, this massive share of total output began to fall. That’s by the time it bottomed out. Just over 30% of all oil production was coming from the Permian. But as energy prices began rising again, fortunes quickly reversed themselves. As of this year, we are back north of the 60% range in terms of contribution.

Of course, the history of the Permian basin goes back more than a decade. In fact, it dates back to the first well that was drilled in the basin in 1920. From that single well sprouted an industry that has resulted in 30 billion barrels of crude oil, not to mention an untold amount of natural gas. Given how much crude has been extracted from the region, you would think that there wouldn’t be much left. But that would be incorrect. Just looking at the two most significant formations, the Wolfcamp and the Bone Spring plays, it’s believed that total recoverable reserves are around 50 billion barrels. This is in addition to 300 trillion cubic feet of natural gas. Even if we focus just on those two plays and assume that output remains unchanged from where it is today, that’s more than 22 years worth of reserves.

Federal Reserve Bank of Dallas

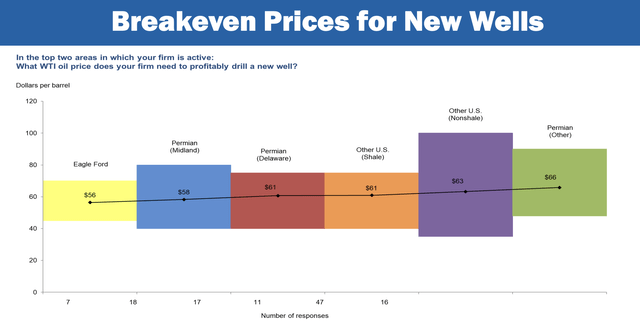

Its size is not the only thing working in its favor. There are a couple of other factors as well. For starters, oil production in the region is some of the cheapest across the nation. In the Midland basin, which is part of the broader Permian, it’s believed that the breakeven price on crude is roughly $58 per barrel. The Delaware, which is another part of the Permian, is only slightly higher at $61 per barrel. The only major region that looks cheaper than these two is the Eagle Ford with a breakeven price of $56 per barrel. Its proximity to major population centers and, most importantly, the Gulf Coast where at least 47% of all petroleum refining capacity and 51% of natural gas processing plant capacity in the country is located, also is a major plus.

Federal Reserve Bank of Dallas

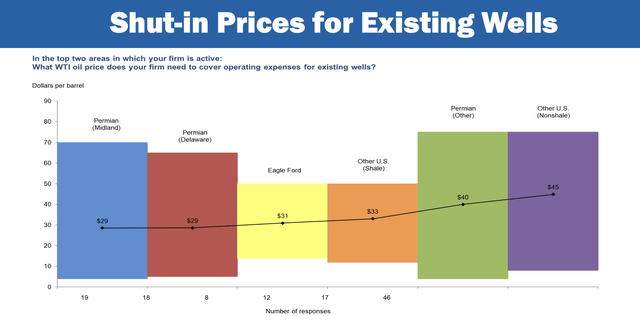

Although oil prices have been quite high for a while, at least compared to where they were several years earlier, it’s true that volatility is still present and will forever be that way. But this is where the Permian can remain competitive as well. The shut in prices for existing wells for the Permian vary based on region. But at the low end, we’re looking at average prices of around $29 per barrel. That’s below the $31 reported for the Eagle Ford and the $33 estimated for other shale that is outside of the Permian and equal forward basins. So in addition to being more profitable, they also can remain profitable at lower prices than other regions.

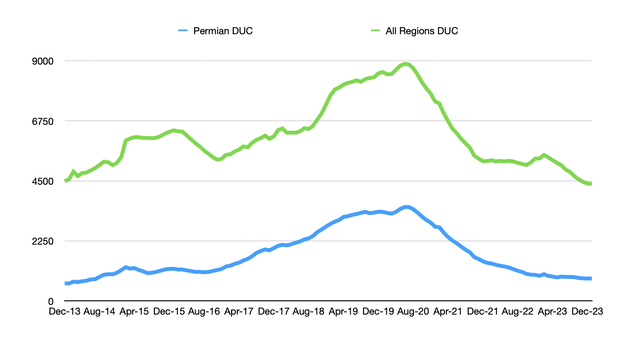

Current projections call for the Permian basin to eventually grow to around 7 million barrels of crude per day. However, the next couple of years will be very interesting. I say this because a lot of the easy, profitable fruit to pick in the Permian and elsewhere has already been picked. The EIA, in its Drilling Productivity Report, keeps track of three different measurements of wells. They keep track of the number of wells that have been drilled, the number of wells that have been completed, and what are called DUCs (drilled but uncompleted wells). This is important because about 73% of the cost of establishing a running well involves the drilling of that well. Only around 9% involves the completion process. When you have high amounts of DUCs, you essentially have significant inventories of wells that can be cheaply completed and put to work.

Author – EIA

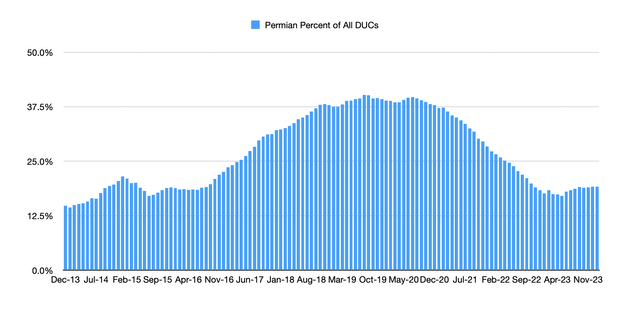

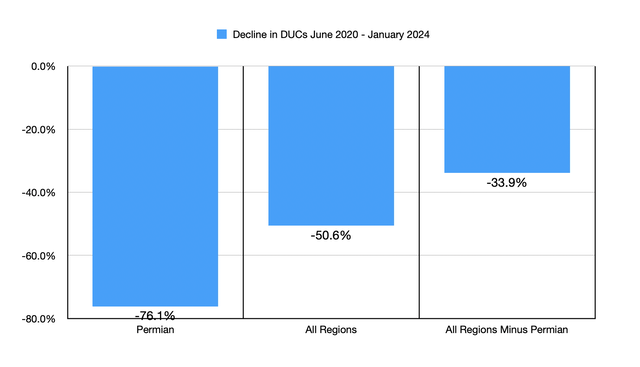

Several years ago now, prior to the pandemic when oil prices were at times less than $30 per barrel, one of the concerns was that the DUC count across the nation was off the charts. At its peak, there were 8,882 DUCs. The concern is that, even as oil prices would start rising again, producers would tap into this cheap and easy portfolio of DUCs, spend the money completing them, and cause production of crude to outstrip demand, effectively driving prices down over and over again. Today, we have a different sort of situation. Since that peak back in June of 2020, the number of DUCs has plummeted to just 4,386. Over that same window of time, the number of DUCs in the Permian specifically fell from 3,517 to only 839. That’s a drop of 76.1% compared to the 50.6% decline seen by the seven largest oil and gas producing regions in the country combined. In fact, the Permian went from comprising 39.6% of all DUCs in the nation to accounting for only 19.1%.

Author – EIA

Author – EIA

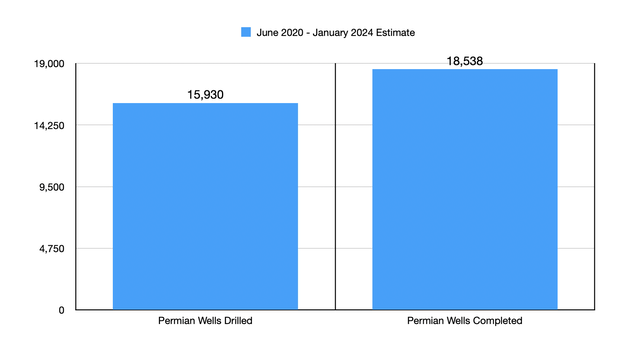

This is all thanks to a surge in both the number of wells drilled and the number of wells completed over that window of time. But at the end of the day, the number of wells completed far outpaced the number of wells drilled. For the companies that have been operating in the Permian, this has been an opportunity to generate significant cash flows. However, this cannot go on forever. At some point, drilling has to step up and that will bring with it much higher costs and lower margins. I have no doubt that the favorable economics of the Permian will make this justifiable. However, it will likely mean that companies operating there will be pressured even more to consolidate their operations in order to cut costs.

Author – EIA

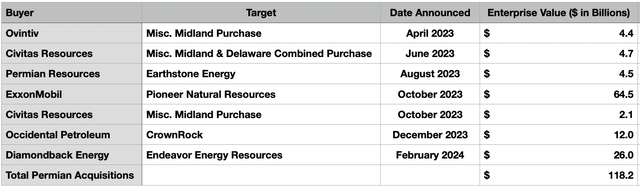

Keep in mind that one of the primary reasons behind these mergers and acquisitions is to capture operational synergies. As an example, let’s take the largest acquisition in the space. That’s the acquisition currently in progress of Pioneer Natural Resources (PXD) by Exxon Mobil (XOM) at an enterprise value of $64.5 billion. The management team at Exxon Mobil expects to capture $2 billion in annual run rate synergies as a result of this maneuver. Considering that Pioneer Natural Resources generated $8.49 billion of operating cash flow last year alone. That’s a magnificent improvement in the bottom line that is in store for shareholders if all goes according to plan.

Opportunities still abound

Author

In the table above, I did my best to list all of the major transactions that have either been completed or announced from the start of 2023 through the present day. This table focuses only on deals involving significant Permian basin assets. That’s why it excludes, for instance, the massive deal between Chevron (CVX) and Hess Corporation (HES). Although Chevron has exposure to the Permian, the company’s decision to purchase Hess had more to do with offshore opportunities abroad than with anything in the US. But I digress.

Author – Texas Railroad Commission

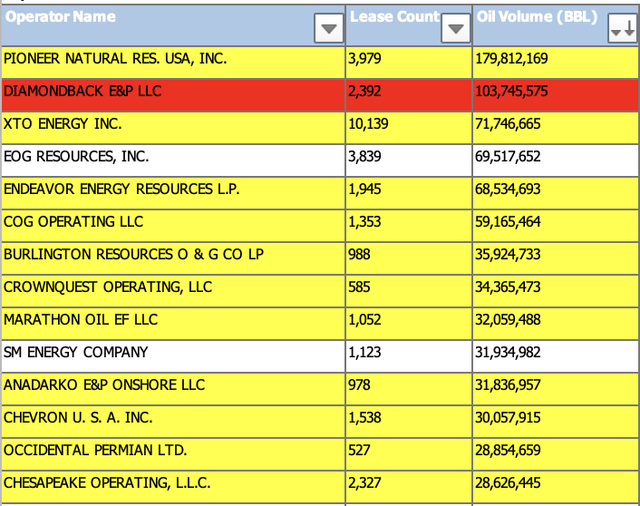

After establishing the transactions that have been announced and/or completed, I next set out to figure out what kind of opportunities might still exist. After several hours of digging, one source that I thought would be appealing but that only proved marginally helpful was the Railroad Commission of Texas. Using data from 2022, it lists out the largest oil and gas producers across Texas. But there are multiple issues with this list that make it impractical. Please see the image above as an example. Although some of the companies listed here might be familiar, many of them are actually smaller operating subsidiaries of larger players. Those that I highlighted in yellow have either already been purchased by another larger player or they belong to another company that does not prioritize the Permian basin in its operations. The one highlighted in red belongs to Diamondback Energy (FANG), which is listed in the aforementioned table because it is currently in the process of buying the privately held Endeavor Energy Resources in a deal valued at $26 billion on an enterprise value basis. That leaves only three companies that make sense to look into.

To increase my list further, I took inspiration from another author (Jennifer Warren) here at Seeking Alpha who referenced Enverus. According to that source, the top Permian producers that are publicly traded happen to be Exxon Mobil, EOG Resources (EOG), Occidental Petroleum (OXY), ConocoPhillips (COP), Devon Energy (DVN), Pioneer Natural Resources, Diamondback Energy, Permian Resources (PR), Ovintiv (OVV), and APA Corporation (APA). There’s some overlap here, and, naturally, some of these are also included in the first table in this section that shows various transactions that have been announced, and, in some cases, already completed.

Author – SEC EDGAR Data

If we assume that the companies that have already recently completed a transaction or that are in the process of completing a transaction are out of the running, we do still run into a few companies that make for interesting prospects. The first company I would like to discuss is the aptly named Permian Resources (PR). This is the one exception to my stipulation of not focusing on a firm that has already made a deal and that’s because of its purchase of Earthstone Energy for $4.5 billion. The reason for this exception is that, unlike other players like Ovintiv (OVV) or Civitas Resources (CIVI), Permian Resources is a “pure play” in the Permian. This makes the business highly desirable for any firm that might want to invest heavily into the region.

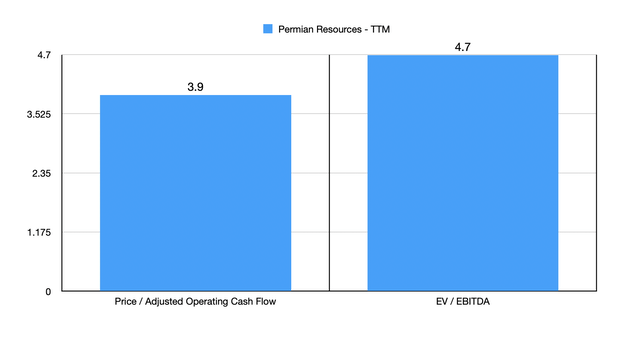

For context, the enterprise has a market capitalization of $11.72 billion and an enterprise value of $13.76 billion. But even since picking up that business, the company has engaged in transactions and land swaps to bring it another 14,000 net acres that it can produce on and another 5,300 net royalty acres, all in the Delaware basin. In total, the company has well over 400,000 net acres and produces over 300,000 boe (barrels of oil equivalent) per day. Unfortunately, shares are not exactly cheap. Because of the recent transactions, it’s difficult to get a good read on what cash flows might be moving forward. Be using trailing 12-month data, the company seems to be trading at a price to operating cash flow multiple of 6.2 and at an EV to EBITDA multiple of 7.6. However, if we make certain adjustments to account for its acquisition of Earthstone Energy, then these multiples come down to 3.9 and 4.7, respectively.

Author – SEC EDGAR Data

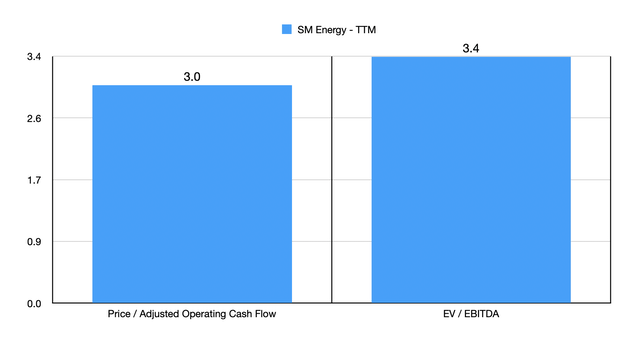

SM Energy (SM) is another interesting prospect that investors should be paying attention to. According to management, about 73.5% of the company’s oil production is in the Midland basin, with the rest in South Texas. With a market capitalization of $4.78 billion and an enterprise value of $5.74 billion, the company could make for a solid bolt-on acquisition for a larger player. The company also has a net leverage ratio of only 0.56, making it one of the least leveraged prospects out there today. Shares are also quite cheap. The company is trading at a price to operating cash flow multiple of 3 and at an EV to EBITDA multiple of 3.4.

The last player that I would like to bring up is unlikely to be acquired itself. Rather, it might be one that would be doing the acquiring. That’s none other than EOG Resources. With a market capitalization of $67.86 billion and an enterprise value of $66.38 billion, the company is a large player. It’s also heavily invested in the Permian basin. 64.1% of total production for the enterprise is in the Delaware basin. Earlier in this article, I mentioned the Wolfcamp and Bone Spring formations. Well, EOG is heavily interested in those areas. Last year, the business completed 188 net wells in the former and 140 net wells in the latter. Despite the fact that the Permian accounts for only 11.7% of all the net acreage of the enterprise, it accounts for 57.8% of net well completions using data from last year and is expected to account for 60% of net well completions, with 360 slated for the year, when it comes to 2024. Although the company has significant acreage outside the Permian, clearly this is the area that it sees the greatest potential in the near term.

Author – SEC EDGAR Data

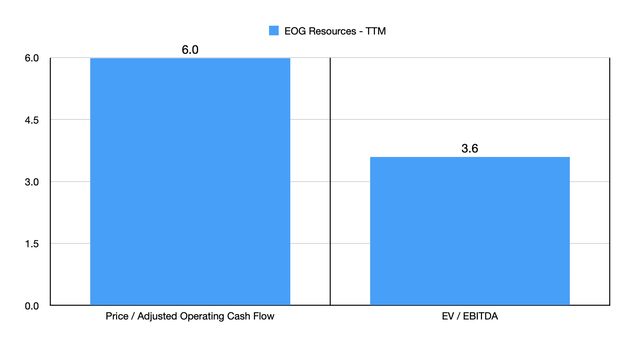

The company also is a cash cow. Operating cash flow last year was $11.34 billion. And EBITDA totaled $18.28 billion. This translates to a price to operating cash flow multiple of 6 and an EV to EBITDA multiple of 3.6. The reason why the latter is so small is because the company actually has a net cash position of $1.48 billion. That means that the enterprise has plenty of fuel with which to make purchases if it so desires. And given its size, it could buy almost anything it wants.

Of course, it’s highly likely that some of the transactions that will occur over the next year will also involve private companies or might even involve firms selling off bits and pieces of themselves. The aforementioned Diamondback Resources / Endeavor Energy Resources transaction is an example of a publicly traded company making a big purchase of a privately held one. There also are plenty of other players out there that are only marginally attached to the Permian. As an example, Marathon Oil Corporation (MRO) is a rather sizable oil and gas company with a market capitalization of around $13.84 billion as of this writing. However, only about 10.1% of its volume involves the Permian basin. There are probably countless other examples that could be looked at of companies with only limited exposure to that region.

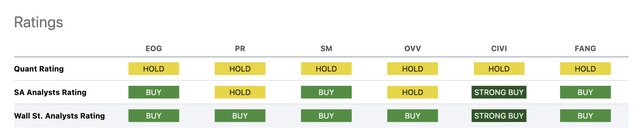

In the first image below, I decided to take our three primary candidates, as well as three other major players in the Permian basin that are not in the process of being acquired and are probably not likely to be acquired. I then compared them using the three different ratings systems promoted by Seeking Alpha. What I find interesting is that all of them are rated a “hold” according to the Quant system, while the ratings associated with Seeking Alpha analysts like myself, as well as those associated with Wall Street, are more generous. This is especially true when it comes to Civitas Resources, which two of the three systems rate a “strong buy.”

Seeking Alpha

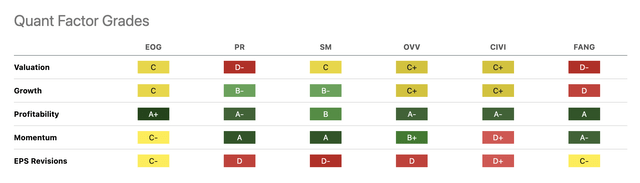

Digging a bit deeper, we can see what goes into the decision-making process for the Quant system. It does appear as though profitability and, to a lesser extent, momentum, have a pretty big influence on the systems results. This makes sense to an extent since profitability is one of the most important traits a company can have. And since energy prices have been elevated for the past couple of years, many of the players in this market truly are cash cows at this time. On a personal level, I put greater emphasis on valuation. In fact, that’s probably the most significant attribute to me. And for those who think likewise, a prospect like Ovintiv looks appealing. But of the three primary ones that I am looking at, the crown would ultimately belong to either SM Energy or Permian Resources.

Seeking Alpha

Takeaway

Although many don’t like to admit it, the days of oil and gas reliance are numbered. Natural gas will last longer than oil does from a practical use perspective. I’m turning 35 this year but I would wager that, by the time I’m in my 80s, global oil consumption will be far lower than it is today. The good news is that, until we get to the point of being able to rely on alternative energies, prolific areas like the Permian basin still exist. A growth in output, particularly economically attractive output, will help to bridge that gap. But as we approach that time and as we deal with higher costs because of a reduction of DUCs and other factors like inflation, I believe that further consolidation in that basin and in other oil and gas producing regions is inevitable. Those who get in now and can capture the right kind of opportunities should benefit nicely.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here