")

Baker Hughes Company (NASDAQ:BKR) is currently in the process of turning around operations and creating a compelling story for the next megatrend for O&G as well as the next generation of energy. Despite the challenges faced in the post-spinoff & Covid-era impediments to operations, Baker Hughes is proving their operating strength in maintaining their dominance in OFS. Similar to Schlumberger Limited (SLB), Baker Hughes is finding value across their international customers, primarily in the Middle East and Asia, while domestic rig demand continues to pull back due to higher production efficiencies. I provide BKR shares a BUY recommendation with a price target of $40.57/share at 9.98x eFY25 EV/EBITDA.

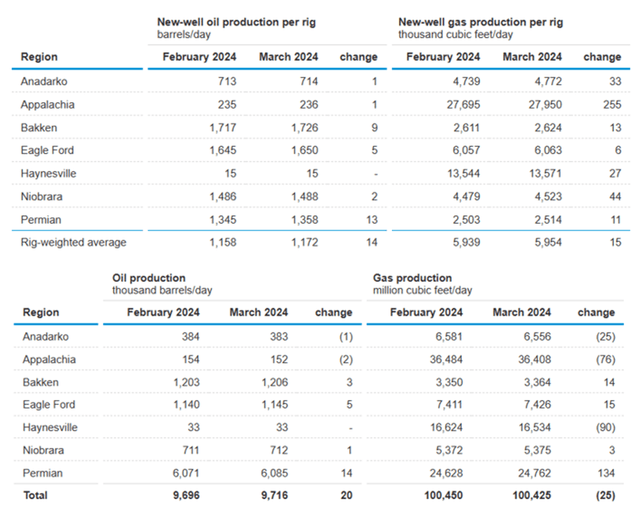

EIA

Baker Hughes found significant growth in LNG infrastructure as the firm received orders for 80MTPA in FY23 and expects projects to continue to move forward with an additional 65MTPA receiving FIDs in eFY24. Management anticipates FIDs for LNG capacity to grow between 30-60MTPA in eFY25 & eFY26 for total FIDs to reach 125-185MTPA through 2026. Management also anticipates capacity to reach 800MTPA by the end of 2030, a 75% increase from 2022 capacity. I believe that this large amount of capacity will be driven internationally by new developments in offshore gas basins in Latin America as Exxon Mobil Corporation (XOM) continues to develop the region, as well as the Middle East as Qatar seeks to fill the gap in LNG demand.

Corporate Reports

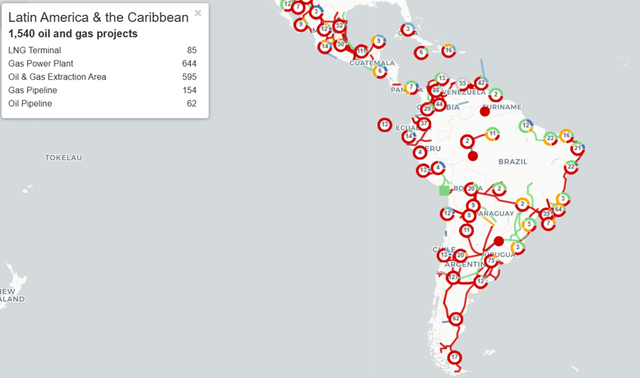

Management highlighted a multi-year contract in Latin America for D&C, plug, and abandonment services, which should push the necessity for OFS infrastructure across the basin as well as the potential need for LNG export capacity to cater to excess production capacity. I believe that with that, Latin America will be one of the larger areas of interest for gas production as the region is relatively underserved in clean power generation, per management commentary at New Fortress Energy Inc. (NFE).

Latin America Energy Portal

Baker Hughes has received strong growth in the FPSO market, with over $1b of awards received over the last two years, and expects 7-9 FPSOs to take FID each year through the latter part of this decade. Management sees offshore demand primarily driven by the Middle East and Southeast Asia. Strength in this region will be primarily driven by gas demand across Europe and may experience growth in conjunction with gas services in the region. Management also discerned growth in new energy in the region and noted that they’re seeing strong growth in geothermal awards.

Geothermal may drive growth domestically as frackers seek to expand their energy services into “green” power production. Though there are certainly headwinds for rig demand and D&C services on the domestic front, as outlined above, new energy may provide Baker Hughes strength as producers seek to further enhance well production, eliminate emissions/flaring, and generate in-basin power with new energy-producing methods. Devon Devon Energy Corporation Energy (DVN) is one example of a producer that is actively managing operations in this fashion. On a broader scale, management outlined a deceleration in growth for D&C spend in eFY24, down from low double-digit growth to high single-digit growth and named oil price volatility as the culprit.

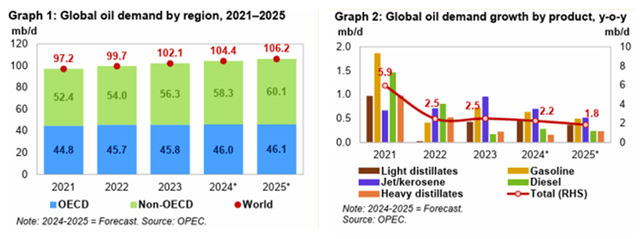

Despite the expectations for a slowdown in D&C services, some positive news has been reported since Baker Hughes reported FY23 results. OPEC+ issued their statement that the organization will maintain production cuts through the quarter to manage production to meet demand. On March 3, 2024, OPEC+ announced an extension of additional voluntary cuts of 2.2MMbbl/d for q2’24. Despite these cuts, the organization forecasted significant growth in the coming years for liquid demand with the expectation of 106.2MMbbl/d in 2025. This is up from 102.1MMbbl/d in 2023. Strength is anticipated to derive from China with growth in the range of 600Mbbl/d in 2024.

OPEC

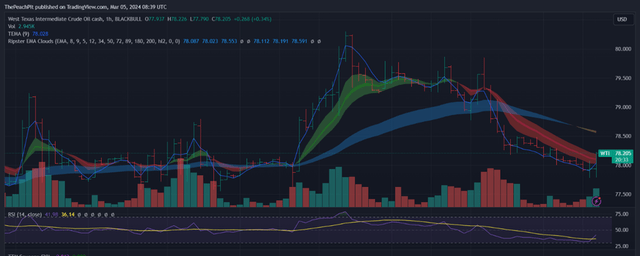

This is a huge positive for the broader energy industry as markets remain tight in terms of production. Contrary to the forecast presented by OPEC+, management at Baker Hughes sees a deceleration in oil demand growth going into 2024. Though on a percentage y/y basis this reads as a 1% growth rate, the incremental barrels are expected to grow by 4.1MMbbl/d through 2025 with 2.3MMbbl/d added in 2024. Looking at WTI prices, this appears to have been a positive turn as the price per barrel has been going, into the meeting.

TradingView

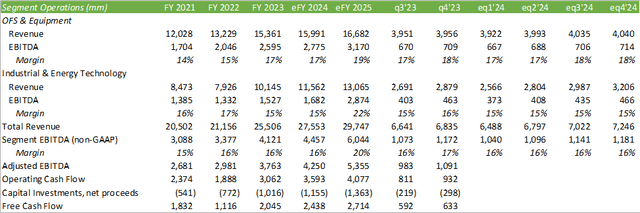

Turning to financials, management is actively managing operations to reduce operating costs to bolster margins. Management’s cost-cutting measures resulted in savings of $150mm in FY23 and are anticipated to reduce redundancies and other overhead costs in eFY24. Management laid out their target of reaching a 20% EBITDA margin across their OFSE and IET segments in 2025. This would be a significant improvement from their current state as margins are expected to be in the range of 16% in eFY24.

Corporate Reports

This would mark a significant improvement to operations when considering their current operating performance. Though this is a feasible target to achieve, significant operating improvements will be required either at the topline or through further cost-cutting measures. For comparison, Schlumberger reported a 24.5% aEBITDA margin in FY23, significantly above Baker Hughes’ current level. Considering Baker Hughes’ recent operating history, I believe that the firm has the capabilities of finding areas of operations to improve margins to reach their targeted 20% core EBITDA margin. In terms of an investment strategy, BKR can be seen either as a GARP or a turnaround play, or both.

Valuation & Shareholder Value

Corporate Reports

BKR has a strong outlay for shareholder benefits with an expected payout ratio between 60-80% of free cash flow. FY23 payout was 65% of free cash flow at $1.32b, split between dividends and buybacks. I anticipate management to follow suit with the rest of the industry in prioritizing buybacks as BKR shares trade at 9.72x TTM EBITDA. This valuation is relatively in line with OFS competitor Schlumberger Limited (SLB) who has a similar shareholder return policy.

At the broader scale, both SLB and BKR have underperformed Brent Oil, and each stock has deviated from their historical trend in moving with the price of oil.

TradingView

This may open BKR shares to a mean remediation strategy in returning to their historical trend. Considering that the company’s valuation is sitting at 9.72x EV/EBITDA, there may be room for multiples expansion going forward. I believe that in order for this to happen, the firm must reach certain benchmarks in achieving their 20% EBITDA margin target. On an incremental basis, I believe that Wall Street will recognize any improvements towards this goal and will bolster share value in tandem. BKR’s valuation converging with SLB’s valuation will require these steps as SLB has operated at a higher capacity in terms of operational efficiency.

Seeking Alpha

Considering Baker Hughes’ current positioning in the market and the necessity to turn around operations, I placed a heavier weight on the lower end of their historic valuation range at 8.75x EV/aEBITDA for a price target of $49.57/share at 9.98x EV/EBITDA.

I believe that there are significant risks to take into consideration when valuing BKR stock as the firm must expand EBITDA margins by 4% to reach their target. I believe progress towards this figure in tandem with WTI/Brent price improvement will drive share growth. The downside risk is Baker Hughes falling short of expectations as the broader macroeconomic headwinds suggest that there may be a major decoupling between the US GDP growth and Japan, China, and Germany going through recessionary pressures. Given that China is anticipated to be a major participant in the growth forecast for oil demand, a deeper recession may place further pressure on the price of oil. I believe that this has the potential to pose a challenge to Baker Hughes’ growth outlook despite operators turning to long-cycle oil production. I believe these factors justify the lower valuation target for BKR shares and if operations fall short of expectations, may place even further pressure on the share price than what I have presented. Despite this moderate outlook, I believe BKR shares are significantly undervalued based on my eFY25 forecast and provide BKR shares a BUY recommendation with a price target of $49.57/share.

Corporate Reports

On a tactical basis, BKR shares appear to be on a continued downtrend. As mentioned above, I believe that certain operational catalysts must be met before shareholders are rewarded. The stock may oscillate around its current valuation until the next earnings release or if oil prices experience an exogenous event that sends prices significantly higher. Given that BKR is a turnaround play, I believe that an investor will have the opportunity to dollar-cost average into a position before their next earnings release in mid-April.

TradingView

Read the full article here