")

Amid a very expensive S&P 500 and benign market sentiment toward growth stocks, one style of tech investment has become very popular again: high price for high quality. And while these plays perform really well in an up market, my macro view is that we’re more likely than not to see downside in the major indices through the rest of the year as we contend with a number of uncertainties: the pace of the Fed’s rate cuts that is so critical to the market’s enthusiasm today, a volatile U.S. election cycle, and an uncertain macroeconomic recovery.

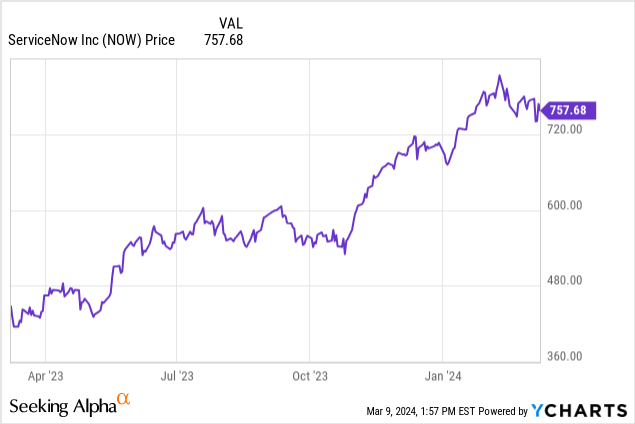

Against this backdrop, ServiceNow (NYSE:NOW) is a stock that bears careful monitoring. The Bill McDermott-led (former SAP chief) cloud company has seen an ~80% rise over the past 12 months, but the company’s strong earnings cycle in late January failed to generate any meaningful momentum for this name.

ServiceNow’s strengths are already embedded into its huge valuation

I last wrote a bearish article on ServiceNow back in September, back when the stock was trading in the mid-$550s (but before the broader market, especially tech stocks, rallied in the last quarter of the year). Since then, ServiceNow has glided upward alongside the rest of its software peers, accruing a much richer valuation – at the same time, the company has also managed to accelerate subscription revenue growth rates while maintaining high levels of profitability. I put all of this together at a neutral rating for the company.

There are, of course, a number of meaningful positives to point out for this company, which include:

- Impressive growth at scale. Despite hitting a >$10 billion annualized revenue scale, ServiceNow continues to grow subscription revenue in the mid-high 20s. That is a major testament to the largesse of its multiple end-markets, which include IT service management, customer service management, and security and risk management.

- AI tailwinds. ServiceNow benefits from AI innovation across many products in its portfolio, enabling virtual agent assistants that help to reduce time to issue resolution and identifying needed repairs in its field services business.

- Rule of 40. ServiceNow manages to grow in the mid-20s while also achieving a pro forma operating margin in the high 20s, squarely establishing the company as a “Rule of 40” software company that balances growth and profitability.

At the same time, however, we have to point out that these strengths are already more than compensated for in ServiceNow’s record-shattering share price – we note that the stock is sitting higher than its pandemic-era records, which not many tech stocks have been able to cross just yet. At current share prices near $760, ServiceNow trades at a market cap of $155.32 billion; and after netting off the $8.08 billion of cash and $1.49 billion of debt on ServiceNow’s most recent balance sheet, the company’s resulting enterprise value is $148.73 billion.

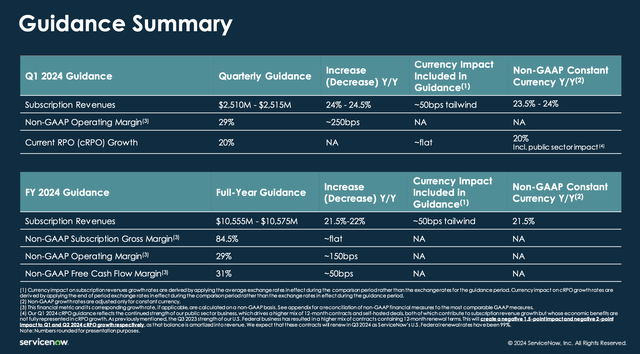

Meanwhile, for the current fiscal year FY24, ServiceNow has guided to ~22% y/y subscription revenue growth alongside a 250bps expansion in pro forma operating margins:

ServiceNow outlook (ServiceNow Q4 earnings deck)

Analysts, meanwhile, are projecting $10.89 billion in total revenue for ServiceNow this year, representing 21% y/y growth; and $13.23 of pro forma EPS. This puts ServiceNow’s valuation multiples at:

- 14.3x EV/FY24 revenue

- 57x FY24 P/E

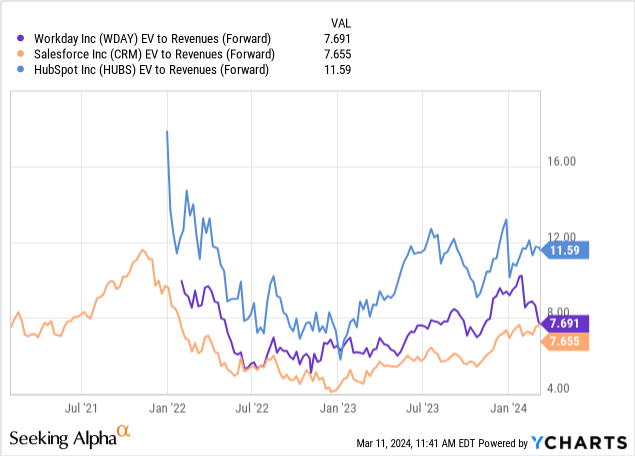

This compares quite richly versus other mid/large-cap software peers in a ~20% growth range:

With interest rates still at multi-year highs, we do have to ask ourselves: can ServiceNow’s premium really be sustained? Yes, the company is performing well; but are there really any catalysts that will meaningfully move the needle on growth going forward that would drive an upward re-rating of ServiceNow’s already-expensive valuation multiple?

In my view, the answer is no. I’d stay on the sidelines here and wait for a better price to avail itself.

Q4 download

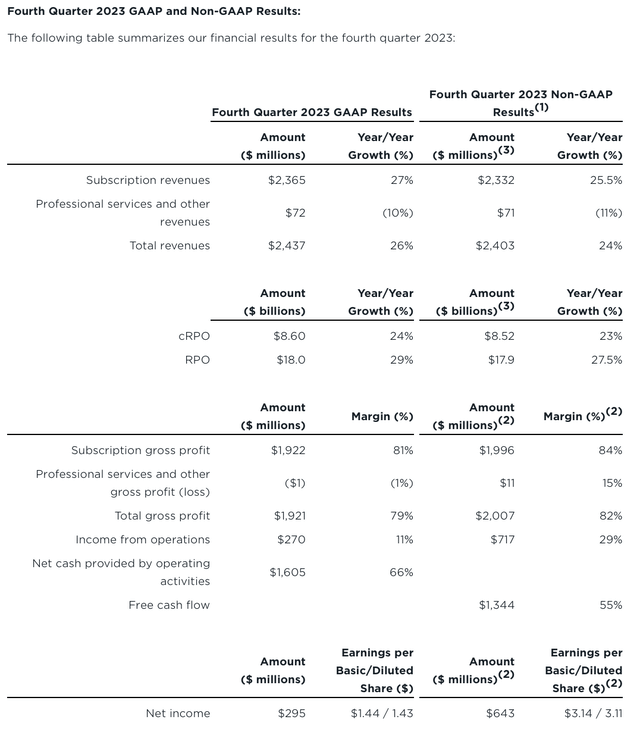

Let’s now go through ServiceNow’s latest quarterly results in greater detail. The Q4 earnings summary is shown below:

ServiceNow Q4 results (ServiceNow Q4 earnings deck)

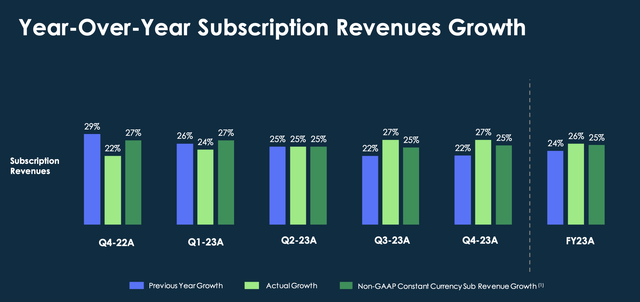

Revenue grew 26% y/y to $2.44 billion, ahead of Wall Street’s expectations of $2.40 billion (+24% y/y). The impressive thing here is that ServiceNow has managed to maintain the same 25% y/y growth pace in subscription revenue (on a constant currency basis) over the past few quarters, as shown in the chart below:

ServiceNow growth trends (ServiceNow Q4 earnings deck)

Many software competitors, meanwhile, have continued to cite challenged IT budgets as the reason for deceleration. Deals including generative AI-fueled products have been one of the core reasons that ServiceNow has been able to sustain its growth trajectory. Per CFO Gina Mastantuono’s remarks on the Q4 earnings call:

In Q4, our Gen AI products drove the largest net new ACV contribution for our first full quarter of any of our new product family releases ever, including our original Pro SKU […]

We are raising our 2024 outlook to reflect the strong momentum with which we exited 2023. This partially reflects the early success we’ve seen with our Gen AI products as those investments are accelerating the build of our already robust pipeline with customers lining up to be first movers in this next wave of business transformation. As always, we continue to be prudent around our assumptions for incremental customer budgets and the macro cost in our guidance.”

From a profitability standpoint, pro forma operating margins in the fourth quarter rose 1 point to 29%. We do note the concern that ServiceNow is still aggressively adding headcount, adding ~500 (or ~3%) net-new heads to its staff in Q4, ending the quarter with 22.7k full-time employees. We like the fact that ServiceNow is projecting operating margin expansion in FY24, but it does seem that belt-tightening and picking up the pace of margin expansion isn’t as high of a priority for ServiceNow as it is for other software giants like Salesforce (CRM), which has done a 180-degree turn on its attitude toward the bottom line.

Key takeaways

Unfortunately, I don’t see much upside for ServiceNow when the stock is already trading at a rich mid-teens revenue multiple despite growth expected to slow down to the low 20s. And with margin expansion occurring but at a slow pace, it’ll be awhile until we can reconcile ServiceNow’s valuation from an EPS basis as well. Steer clear here and invest elsewhere.

Read the full article here