Thesis

When rates are high, which now seem to be destined for a more persistent nature than originally thought, wouldn’t it be nice to invest vicariously through the best balance sheets in the world? When or if rates dive, M&A activity will pick up with lower costs of capital. Even with a pristine balance sheet, there’s usually some level of debt and some level of cash used while making the sausage. These 4 companies should not only be able to access the most rock bottom rates as they fall, but also avoid excessive syndication when making a deal, since cash reserves are a near bottomless pit.

The below portfolio is the strongest balance sheets I could find. Ones where liquid investments are normally double or more long-term debt. This results in a positive net interest expense where these companies are being paid to wait for a place to deploy capital. With so many “great idea, not great cash flow” tech companies in a cash crunch, diluting investors at the bottom, these companies can wait to strike like a viper. All the while swimming in a vault of cash like Scrooge McDuck. I own all these names and remain bullish on the majority, they anchor a good portion of my portfolio.

If we both fall into the camp that a secular bull will keep running combined with M&A starting up on the tail end of the year should the FED move to cuts, this portfolio provides an investor with companies that can take advantage of the high interim rates and non-organic growth opportunities as they come into view. Intelligent use of liquidity can keep the top line compounding for the foreseeable future.

The list of companies with my favorite balance sheets is the following four:

- Alphabet (GOOG)(GOOGL)

- Microsoft (MSFT)

- Meta Platforms (META)

- Apple Inc. (AAPL)

Low to no dividends with massive buyback power

If we are looking to add long-term growth and quality to our portfolios while still in a raging bull market, buybacks can be our friend should a sell-off ensue. These companies pay low to no dividends but are some of the most furious buyers of their shares, utilizing growth in cash flow and cash from the balance sheets.

Buying shares in the open market can stabilize prices should shares get into a sell-off and most importantly, continue to increase free cash flow per share. The retention of most of the cash flow rather than the funds being paid out in dividends will put these companies at an advantage over others as it pertains to price stabilization.

Alphabet

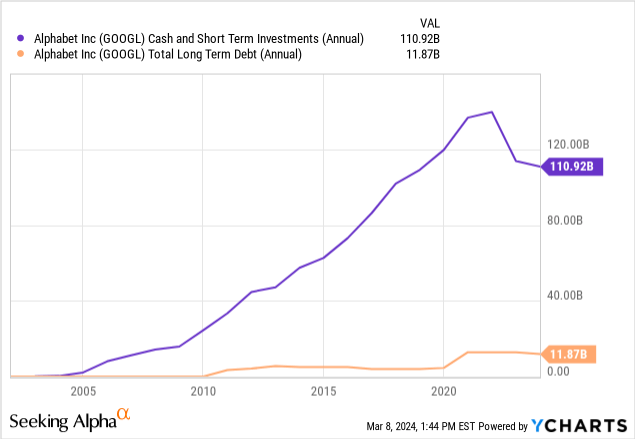

First up is Alphabet. This is the one stock out of the bunch that I would rate a strong buy. About $12 Billion in long-term debt against over $100 Billion in cash and short-term investments. This is the winner for the strongest balance sheet at the moment in my humble opinion.

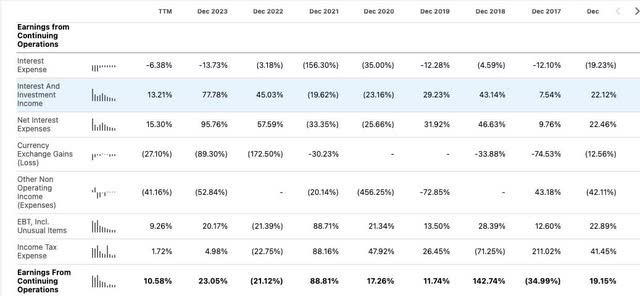

Let’s take a look at the net interest expense line:

Seeking Alpha

The company is in the positive to the tune of USD 3.55 Billion. The negativity as of late surrounding Alphabet’s AI failures is way overblown and has created a buying opportunity. They are ahead of Tesla (TSLA) when it comes to full self-driving taxis with Waymo and the ad business remains the strongest in the game. You just don’t end up with this much cash by chance. You have to have a very strong free cash flow-producing business.

Seeking Alpha

The year-over-year growth rates for interest income are striking. I’m happy to watch Alphabet collect cash and spit out interest until the next best thing pops up for them. Be it an internal creation or an inorganic acquisition, the balance sheet is the toolset to keep the future compounding machine alive.

Seeking Alpha

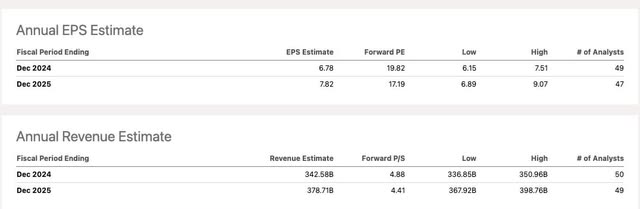

Analysts have a high end 2025 EPS estimate of $9.07 a share, I’m in the high-end camp.

- FY 2024 high end is at $7.51/share. High end 24 to high end 25 is a 20.7% GAAP growth rate.

- With the stock trading at $135, that’s 14.88 X 2025 GAAP high end EPS with a 20.7% growth rate.

- That’s a possible .71 FWD PEG ratio. Fair price at PEG 1 would be 20.7 X 9.07= $187.74.

This is the best buy and hold of the group in my opinion.

Revenue sources from FactSet:

| Source | Percentage |

| Web-based data and services [advertising] | 78.48% |

| Internet Hosting Services | 10.76% |

| Marketing and Advertising Services | 10.19% |

| Wireless Services | 0.50% |

| Multi-service revenue | 0.08% |

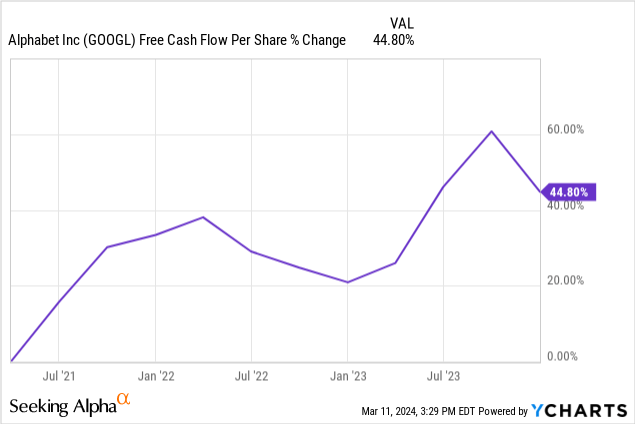

3 year Free cash flow per share growth:

At an over 44% increase in free cash flow per share growth over the past 3 years, this is an impressive number because Alphabet has consistently been one of the largest revenue generators on this list during this duration. They weren’t moving from a small number to a larger number, they were going from a larger to a larger number.

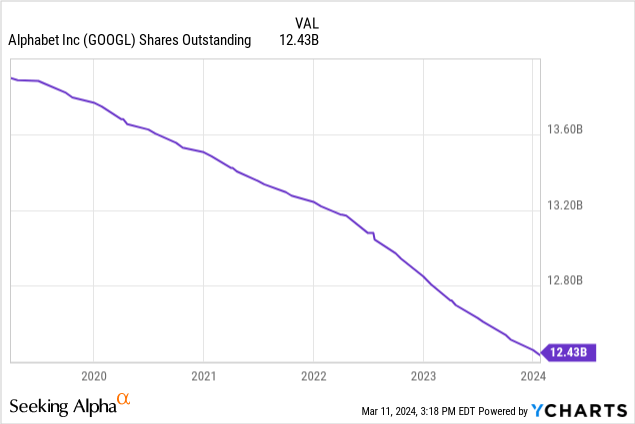

5 Year share reduction:

A common theme we’ll see in these names is a horizontal drop from corner to corner of the chart as it pertains to shares outstanding. Alphabet has reduced shares outstanding by 10.53% over the previous 5 years.

Microsoft

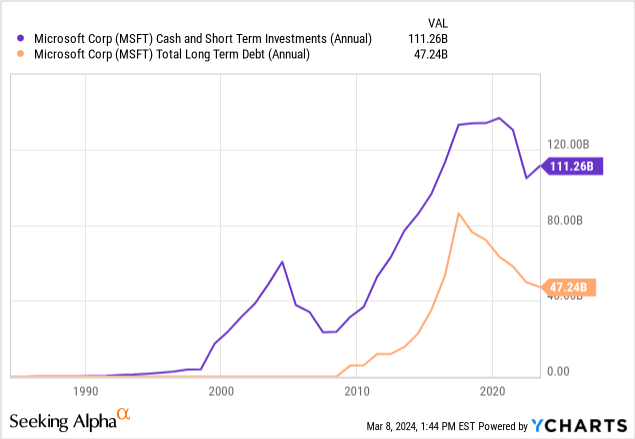

This is a stock I’ve owned for quite some time. Microsoft consistently churns out a high return on invested capital and consistent top-line and free cash flow growth. A very well-capitalized balance sheet, with over $110 Billion in cash and equivalents against only $47 Billion in long-term debt.

ChatGPT and the presumption that Bing, owned by Microsoft, may slowly eat into Google search with its advanced AI integration has pushed the stock up to fairly high multiples, making it the most expensive of the four. I still haven’t switched from Google to Bing. But hey, if the move happens, I own all these names as a hedge.

Seeking Alpha

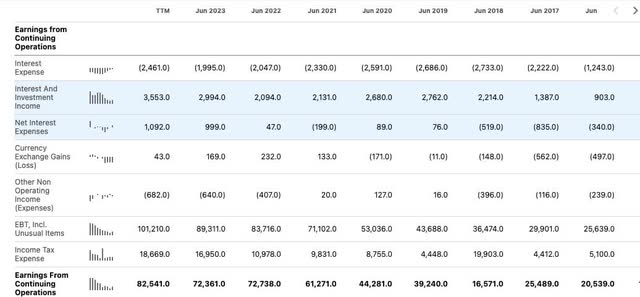

The net interest income is not as dramatic as Google’s with the higher debt load, but Microsoft is still collecting over $1 Billion in interest income over interest expense. With rates remaining chronically high, this is becoming one of my favorite margin of safety metrics.

Revenue sources from FactSet:

| IT Infrastructure Software | 37.74% |

| Home and Office Software | 33.14% |

| Web-Based Data and Services | 12.91% |

| Electronic Gaming/Entertainment Electronics Makers | 7.3% |

| Information Technology Consulting | 6.21% |

3 Year Free cash flow per share growth:

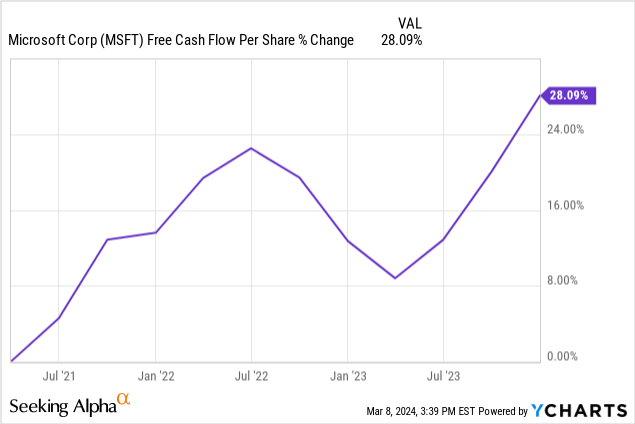

Microsoft has increased free cash flow per share by 28.09% over the past 3 years. We’re seeing a consistent theme in the group, with free cash flow dipping in early 2023 and recovering in 2024. The combination of buybacks, rightsizing, and decreased CAPEX spending tend to be the culprits.

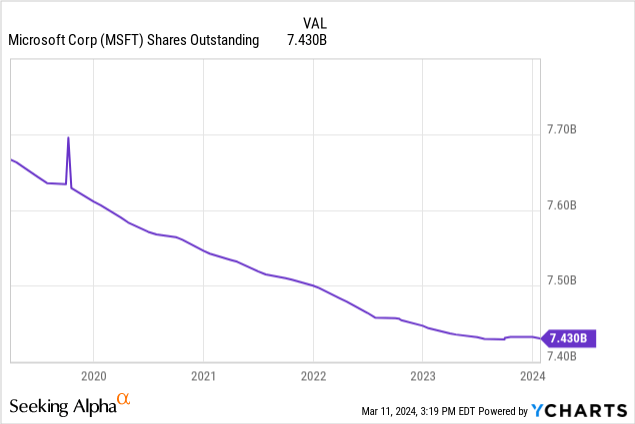

5 Year share reduction:

Microsoft has reduced shares outstanding by 3.07% over the previous 5 years. While this is the least impressive of the group, Microsoft does pay the highest dividend of the group at .74%. They also deployed a lot of cash into Activision, which should help the 7.3% revenue from gaming grow into double digit representation.

Meta

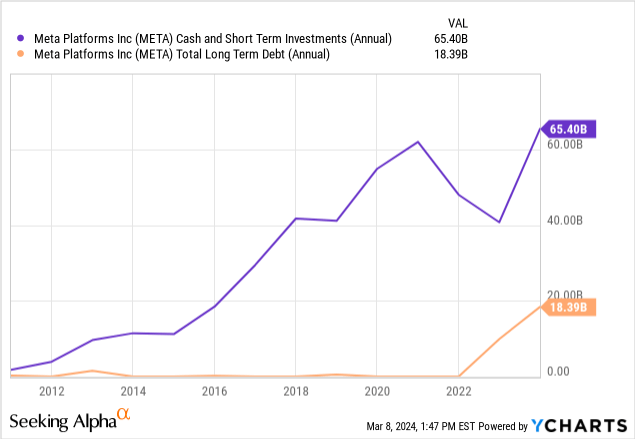

Meta Platforms is one of my largest holdings and has an excellent balance sheet. The company boasts cash and short-term investments of $65.4 Billion, compared with $18.39 Billion of long-term debt. This is all being maintained in the face of Reality Labs’ investments that significantly decreases operating income. From the most recent Meta Platforms 10K:

We are also continuing to increase our investments in new platforms and technologies, including as part of our efforts related to building the metaverse. Some of these investments, particularly our significant investments in Reality Labs, have generated only limited revenue and reduced our operating margin and profitability, and we expect the adverse financial impact of such investments to continue for the foreseeable future. For example, our investments in Reality Labs reduced our 2023 overall operating profit by approximately $16.12 billion, and we expect our Reality Labs investments and operating losses to increase meaningfully in 2024. If our investments are not successful longer-term, our business and financial performance will be harmed.

Talk about a cash printing business. Creating losses that exceed most other companies’ total operating profit and still maintaining a balance sheet that would create envy amongst its peers. That’s how good Facebook is.

Seeking Alpha

At $1.193 Billion in interest income, Meta Platforms ranks second on this list for interest income more than interest expense. Keep in mind that most of these companies are so low debt not because they are diluting shareholders with equity sales, it’s because they have the cash to be self-funding.

Seeking Alpha

The growth in interest income is again staggering for Meta. They stuck to the short end, cash, and equivalent end of the yield curve rather than put money into long-duration bonds and the patience and payoff worked. We may be in a chronic short-term high interest rate environment, and to be able to have your cash earning you a significant yield and be same week liquid at face value is an advantage over competition when your bank account is this big.

Revenue sources:

| Source | Percentage |

| Web-based data and services [advertising] | 98.59% |

| VR equipment | 1.41% |

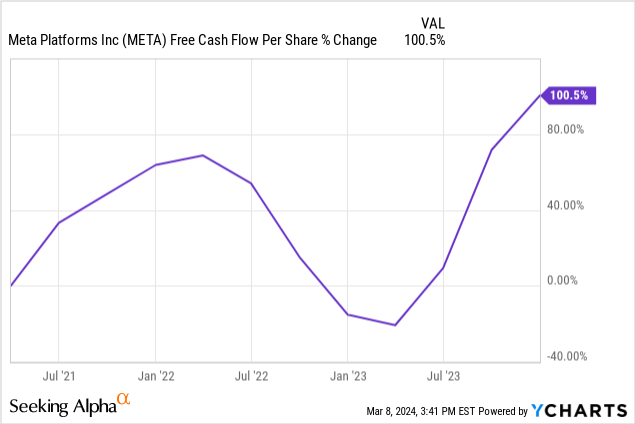

3 Year Free cash flow per share growth:

Meta has done a great job growing free cash flow, being the most nimble on this list at over a 100% increase in the past 3 years. The buying opportunity around $100 a share was amazing, and Meta’s confidence in their cash flow and balance sheet, buying back shares, helped you as an investor get back to all-time highs.

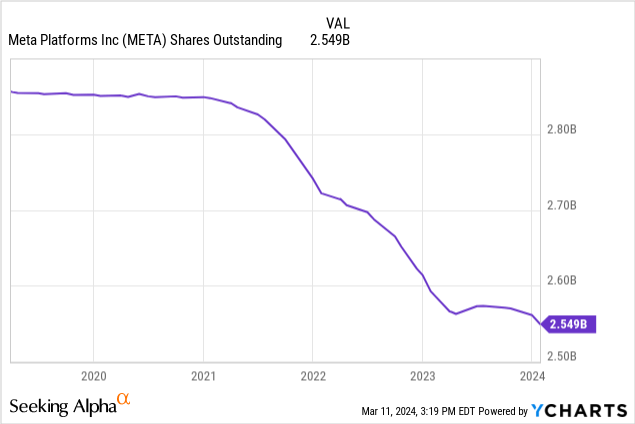

5 Year share reduction:

Meta has reduced shares outstanding by 10.74% over the previous 5 years.

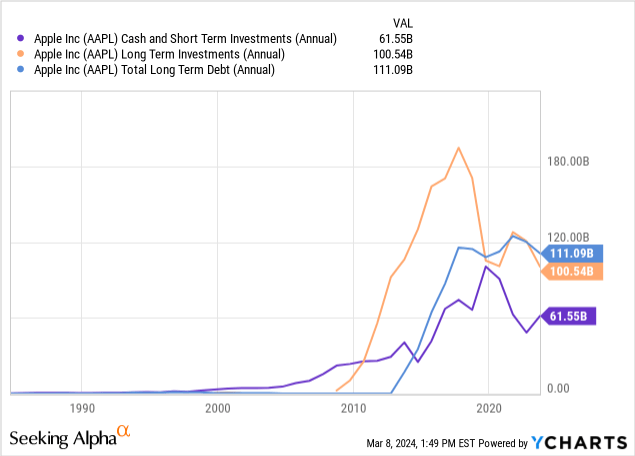

Apple

Apple is interesting. Out of the group, you will find that Apple has one of the largest long-term investment lines on the balance sheet. Long-duration investment-grade bonds run through Apple’s Braeburn Capital located in Reno, Nevada has been a staple home for excess cash on Apple’s balance sheet. Unfortunately, Apple was generating too much excess cash during the zirp period and decided to plunk what now equates to over $100 Billion in long-term bonds. They probably would have been better off-putting those funds into R&D like the other 3 companies mentioned here, but it is a source of liquidity nonetheless.

While there is no 13F filed for Braeburn’s holdings, I assume since these are all fixed-income orientated, we can’t surmise the face value of the bonds. We can assume that the average rates are lower than what is currently available and Apple will be stuck holding these to maturity. It would take a mighty emergency to tap this resource.

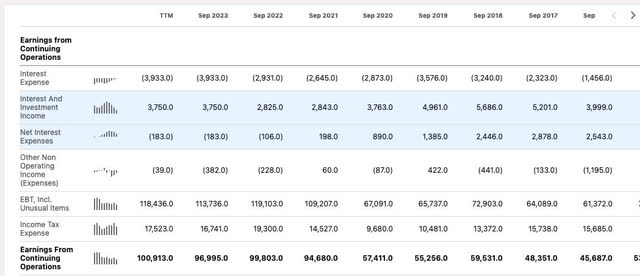

Seeking Alpha

The assumption of the relatively low-yielding nature of Apple’s long-duration investments is revealed when seeing that Apple has a small, but existent interest expense liability while the others on the list are collecting interest payments over interest expense.

Revenue sources from FactSet:

| Source | Percentage |

| Wireless Mobile Equipment | 52.33% |

| Web-based data and services | 22.23% |

| Computer Systems | 15.04% |

| Wearable Technology | 10.40% |

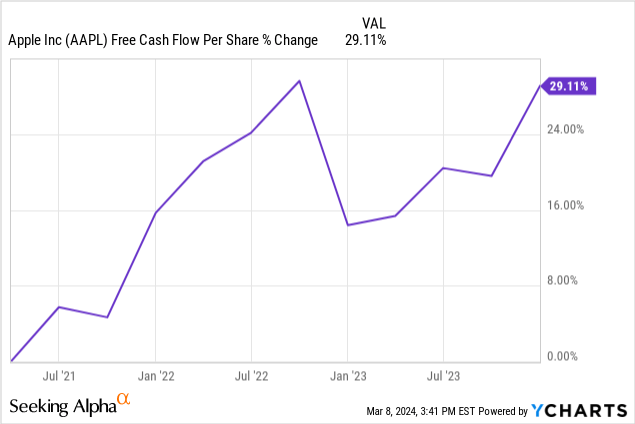

3 Year Free cash flow per share growth:

Although the top line has stalled out a bit, Apple continues to grow its free cash flow per share. This and earnings per share can continue to grow even in the face of a shrinking top line, if buybacks keep going at a rate faster than revenue shrinkage. Apple is top on this list for returning capital to investors via its buyback program.

The recent canceling of the EV program and the shift of focus and workforce toward AI should help the company return to top-line growth through enhancements of software-related offerings and iPhone improvements.

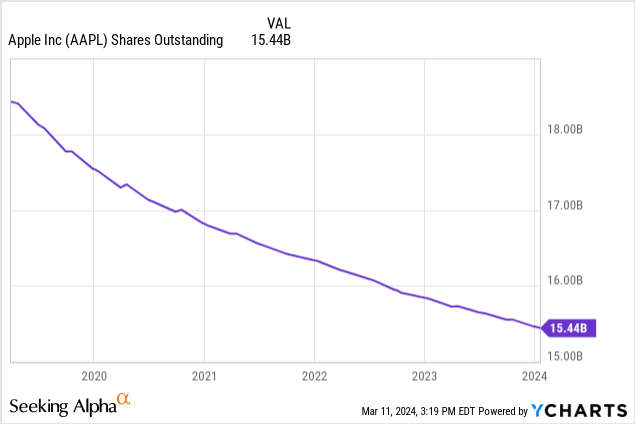

5 Year share reduction:

Apple has reduced shares outstanding by 16.21% over the past 5 years.

With the rate at which Apple buys back shares at any price, we should all be hoping for a bit of a sell-off to give both ourselves and Apple some extra opportunities to buy shares at more attractive prices.

Risks

These stocks trade at multiples over the long-term market average. That being said, many quality stocks do. While the balance sheet strength is intended to prevent downside risk in this thesis, it’s not certain that the companies listed herein will execute buybacks on the way down if the market falls. Companies have been and are still criticized for buying back too many shares at the top and too few at the bottom. Time will tell, and only Meta truly went through a crash period where it was able to buy back its shares at clearance sale values.

Here is an example of what Meta did at the 2022 lows:

Seeking Alpha

Pointing out 2022, the company [Meta] bought back 4.75% of the shares year over year, which was excellent execution and the highest during these 5 years.

Google had a similar, but not as extreme of a dip in 2022 and bought back 3.12% of shares year over year. The highest in the same 5-year period as above but not as aggressive as Meta.

As for Microsoft, they have been the weakest share repurchaser but also arguably the most expensive name. Should they experience a pullback to bring their multiple more in line with the other names on this list, it will be interesting to see if they hit the buyback button harder.

Even Jeremy Grantham couldn’t deny this group is special

Listening to a recent interview by Jeremy Grantham, the British investor who has been known to be bearish more often than not, could not deny that this group is an abnormal compounding machine. Whilst he will never give into the “this time it’s different” narrative, he still admits that this group produces consistent and enduring returns on invested capital that have never before been witnessed in market history. He attributes this to a weak anti-trust system that allows these companies to grow unchecked. He maintains that the biggest risk for the group remains regulatory risk.

Summary

Out of the “Fab 7”, these are the strongest balance sheets of the group in my opinion. While Amazon remains one of my top buys amongst the group, they admittedly have a weaker balance sheet in comparison to these 4. For a new or recently abstinent investor looking to involve themselves in long-term tech investments at fair prices, these are the 4 to look to in my opinion. Their free cash flow keeps growing and all but Apple are still compounding the top line.

Read the full article here