")

Sports retailer JD Sports (OTCPK:JDSPY) has had a rocky start to 2024 and there could be worse to come. However, I think the current share price significantly underestimates the business’ long-term potential.

I last wrote on the name in September with my “strong buy” piece JD Sports: Strategy Looks On Course. Since then, it has fallen 2% and I have increased my position. I continue to see this as a strong buy.

Why the Shares have Fallen

Let’s begin with what has happened since my last piece. The main event was a profit warning in January. That sent the shares down sharply and as I write this, they are around 30% lower since the start of 2024.

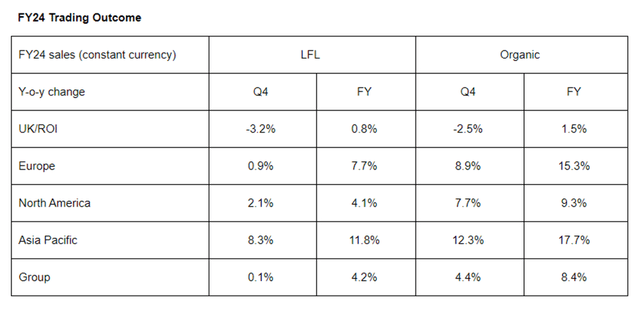

The profit warning was based on performance in the 22 weeks to 30 December. Constant currency organic revenue growth was 6.0% with like-for-like growth of 1.8%, and the company said this was slightly below its expectations. Milder weather was partly blamed although, more concerning in my view, the company also described the peak trading period for the market as a whole as “softer and more promotional than we anticipated, reflecting more cautious consumer spending.”

Gross margin was in line with the prior year period, but as JD expected better (blaming the shortfall on promotional activity levels), it said it now expects gross margin at the full year level to be “slightly lower” than last year.

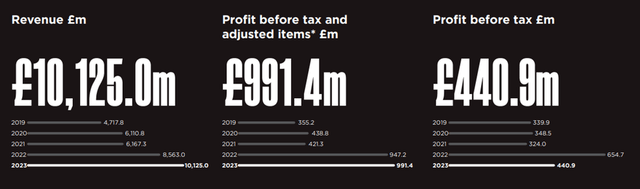

Adding in several other essentially accounting items, it said that it estimates full year pre-tax and adjustments profit to be £915-£935m. At the interim results stage in September, that number had been £1.04 billion. So the profit warning was a downgrade of 10-12%. Coming eleven months into its financial year, though, that downgrade is more substantial than it may at first sound, which I think explains the market reaction.

The concern, as I see it, is not so much about the current financial year, but whether such a dramatic drop-off in the final part of the current financial year suggests that the next financial year could be awful.

This week, the company updated the market on its 2023 performance. It delivered on the downgraded expectation, saying that “FY24 Profit before Tax and Adjusted Items (PBT) expected to be in line with the £915-935m guided range”.

Looking at the numbers, even in a challenging market, sales growth was positive though not spectacular.

Company full year trading update announcement

The Market Does Have Pricing Challenges

Is JD alone?

I don’t think so. Sports apparel has been feeling the pressure of tightening consumer spending. Stock Waves discusses some impacts in NIKE: Facing Global Growth Pressure (Technical Analysis) and there are other concerns popping up pointing in the same direction, as seen in Foot Locker Q4 Earnings: Promotions Drive Topline Beat, Shares Fairly Valued.

On an Adidas (OTCQX:ADDYY) earnings call last month, a similar message:

Again, I think we all know at the end right now, the most decisive factor on price is the discount. And that as very different from product-to-product and market-to-market. And I think it’s fair to say there is still the total trade, not necessarily our product, but there’s still a lot of inventory out there. And I would still say more in the U.S. than what you have in Europe, where at least our customers seems to be very clean on our inventories, which is very, very positive.

So, it seems that JD was communicating what the wider market was experiencing (which given its broad reach in the U.S. as well as Europe and elsewhere makes sense): for now, demand is holding up but is significantly driven by margin-eroding promotional activity.

That doesn’t look good in terms of outlook. Unless things pick up, either demand will continue to rely on discounting (setting up a less profitable market for several years, in all likelihood) or else will fall despite discounting as consumers reduce their buying.

Previously JD has indicated that its youthful customer base rides above such challenges. In the September interims, it said, “our core consumers remain resilient in the face of the ongoing global macro-economic challenges.” That, it seems, may now have changed.

A Moment for Strategic Decisiveness

Leaders are paid to lead and it will be interesting to see what JD does from here.

In January 2023 it set out an ambitious growth plan including adding hundreds of new physical stores annually, covered in previous pieces (like this one). Last year, JD opened 215 new shops.

If that is the right strategy (which I believe it is, but that is subjective), management will stay the course and stick with it, ignoring from the long-term perspective the current full-price demand wobble). Another option would be to start hedging its bets and cut back the plan while the market remains soft. That didn’t drive JD from market stall to behemoth in four decades, but we’ll see what happens. Cutting back on the strategy – of which for now there is no sign – could damage investor confidence both in the strategy and management.

At the interim stage, JD had £1.3bn of net cash. In the trading update this week it did not provide a specific number but said that it “ended the year with over £1bn of net cash.“

For a company with a sub £6bn market cap that is a powerful cushion and it means that, even in a weaker trading environment, the management maintains flexibility for maneuver.

Valuation Looks Attractive

In the short term, we do not know how bad things may get in the sportswear market. In its trading update, though, JD said that, “initial FY25 PBT guidance, pre-accounting adjustment, of £900-980m”. That suggests that profit before tax this year ought to be roughly in line with, or better than, last year.

It also said that, “(t)rading in the new financial year-to-date is in line with our expectations after seven weeks”.

Longer term, though, it is hard to imagine that there will be negative structural shifts in demand. JD has a tested and proven business model that thrived following the 2008 financial crisis and since.

The shares are down 32% in a year but the long-term story here has been one of gain. Over the past decade, JD Sports has been a seven bagger. Post-tax profit has been £230-265m in four of the past five years.

On that basis, the company is trading on a P/E ratio in the low twenties. That does not look cheap, especially given that the short- and medium-term outlook for profitability is worsening.

I continue to see value here though, hence maintaining my “Strong buy” rating. JD’s post-tax profits reflect substantial ongoing investments in growth. Those investments have driven significant growth in recent years, and I expect that to continue to be the case.

Company annual report 2023

Net cash increased over tenfold between 2019 and the end of last year.

Operating cash flows are routinely now around or above £1bn annually. The market cap is just six times that. Allowing for the net cash position, they are four to five times that. Yet the majority of JD’s non-operating cash flows are acquisition of property, plant and equipment and repayment of lease liabilities. Both help growth but could also be substantially reduced fairly fast if the company so decided.

Consider, alternatively, that JD stops investing in potential growth and simply ticks over as it is. In that scenario, operating income and earnings would be closer together, without the debt-free company needing to spend so heavily on items like opening hundreds of new shop. Trading at six to seven times operating income (and similarly for operating cash flow), the shares look cheap.

In other words, the company is very cash flow generative and is busily investing a large part of its cash flow in its own ongoing growth. Looked at from that perspective, if one believes in the long-term growth story, I see JD shares as underpriced.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here