")

Verizon Communications Inc. (NYSE:VZ) is a free cash flow-strong Telco that supplies passive income investor with a well-covered 6% yield that can make a big difference for retirees that rely on growing dividend income from their passive income investments.

Though some investors see Verizon Communications’ considerable balance sheet debt as a burden, I think that the low dividend pay-out ratio leaves substantial room for dividend growth in 2024 and translates into a very high margin of safety.

With the underlying Broadband business also seeing robust subscriber growth and the earnings multiple being irrationally low, I think that the risk/reward relationship for passive income investors is exceptionally compelling.

My Rating History

In my last piece on Verizon Communications Verizon: A Steal At $37 I discussed the Telco’s FCF value proposition for passive income investors.

Taking into account Verizon Communications’ ongoing momentum in Broadband and FCF resilience, the Telco is poised to deliver solid dividend growth in the future. The stock remains a bargain, particularly if the company’s low pay-out ratio is considered.

Robust Free Cash Flow And Broadband Growth

As is the case with Verizon Communications’ main peer, AT&T Inc. (T), the Telco’s Broadband activities have been met with considerable success.

One element of Verizon Communications’ growth strategy is the ongoing scaling of its Broadband business which so far has been a significant success for the company. The Broadband segment has seen consistent growth in the last year, including in the fourth quarter which is when Verizon Communications added 413K new Broadband subscribers to its network.

The Telco is consistently adding new locations to its Broadband network and added 426K in new subscribers on average to its service per quarter in 2023. This momentum can clearly continue in 2024 as the Telco keeps investing into the expansion of its Broadband capabilities.

This growth, in turn, backs Verizon Communications’ free cash flow and dividend which is ultimately the primary reason why investors may want to own VZ in a passive income portfolio.

New Subscribers (Verizon Communications)

Strong FCF Growth, Low FCF Pay-Out Ratio

Verizon Communications’ Broadband growth is one reason to own the Telco’s stock. Another is the company’s low pay-out ratio based on free cash flow.

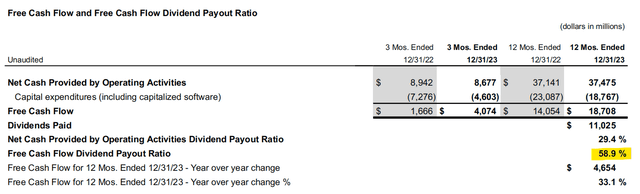

Verizon Communications earned $18.7 billion in free cash flow in 2023 which was $4.6 billion higher than in 2022. The Telco did not only see strong free cash flow growth YoY, but paid out less than 60% of its FCF in 2023, resulting in a very high margin of safety for passive income investors.

AT&T earned $18.6 billion in free cash flow last year and had a dividend pay-out ratio of 47%. Though AT&T offers passive income investors a lower FCF-based pay-out ratio than Verizon Communications, the latter’s dividend is growing, and AT&T’s is not.

Free Cash Flow (Verizon Communications)

Low Earnings Multiple + Low Pay-Out Ratio = High Margin Of Safety

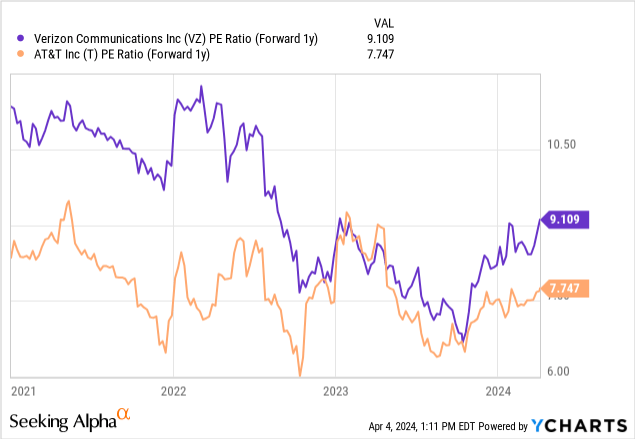

Verizon Communications is costing passive income investors 9.1x leading earnings whereas AT&T’s stock is presently selling for a 7.7x earnings multiple.

Both Telcos obviously make a solid value proposition to passive income investors as they pay out substantially less than they earn in free cash flow, but I think that Verizon Communications is the much better choice here, for one particular reason: Whereas AT&T has stopped to grow its dividend pay-out (primarily because of debt issues), Verizon Communications is still growing its dividend. The last dividend hike, in 3Q-23, yielded a 2% raise for dividend investors. While the percentage amount may not appear like much, over time a 2% annual dividend increase can make a big difference for retirees that live on fixed income. The Telco’s dividend growth rate between 2018 and 2023 was also 2% and investors more likely than not are going to get another 2% dividend hike later this year as well.

Verizon Communications’ higher earnings multiple is probably due to the fact that the Telco is making a stronger value proposition for passive income investors, at least in a direct comparison to AT&T.

Why The Investment Thesis May Disappoint

Just like AT&T, Verizon Communications has to work through a lot of debt issues. The Telco owed $150.7 billion in debt at the end of 2023 which was only $100 million less than what Verizon Communications was on the hook for the year before that. Put simply, Verizon Communications has way too much debt on its balance sheet which may prove to be anchor to the Telco’s valuation in the long run.

My Conclusion

AT&T is my biggest (non-BDC) income position in my passive income portfolio with a 5% portfolio weight, due primarily to valuation considerations. Verizon Communications is a close second with a weight of 4%, however, and I sleep well with both these Telcos in my portfolio.

Both companies supply passive income investors with very well-covered, free cash flow-backed dividend yields exceeding 6%.

Verizon Communications is driven forward by robust subscriber tailwinds that allowed the Telco to welcome more than 400K Broadband subscribers in every single quarter in 2023.

The main difference between AT&T and Verizon Communications is that the latter is growing its dividend while AT&T’s dividend has flatlined. I think that the 2% dividend growth rate is not as shabby as it looks and taking into account that the Telco’s free cash flow is sufficient to pay much more than the present dividend, Verizon Communications is worthy of a portfolio overweighting as well, in my view.

Read the full article here