")

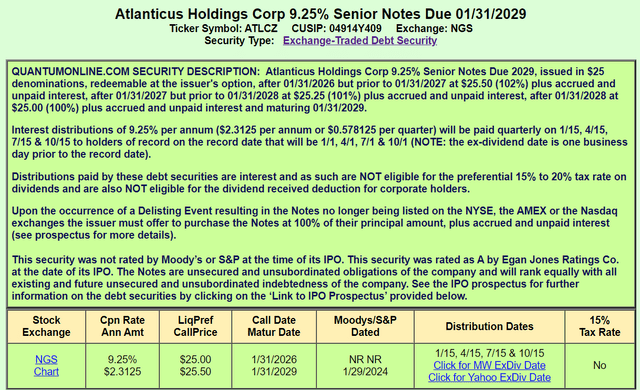

Atlanticus Holdings (NASDAQ:ATLC) is a niche consumer lending company that specializes in providing financial solutions to underserved communities. The company owns several consumer credit brands that partner with various health and retail corporations to provide credit solutions to their customers. Recently, the company issued a new baby bond with a 9.25% coupon (NASDAQ:ATLCZ). The bond is callable in January 2026, matures in January 2029, and is currently trading near par. Based on the company’s performance and the risks it faces, I believe the baby bond investment is the best avenue for income-seeking investors.

Earnings Presentation QuantumOnline.com

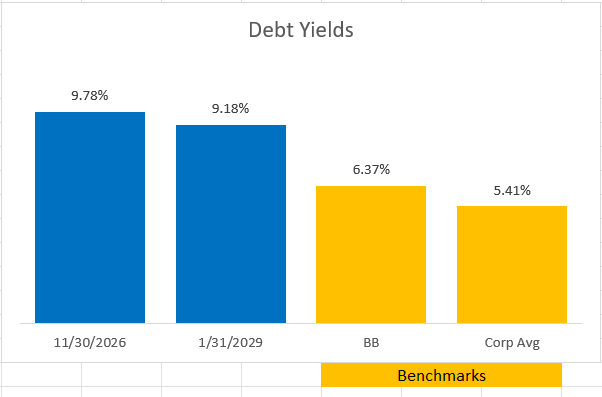

Atlanticus does provide a second baby bond that is currently trading at a slightly higher yield to maturity (ATLCL). This bond is currently callable but trades with a lower coupon of 6.125%. I believe the higher coupon baby bond is better in this situation because it will provide higher streams of income versus the lower-yielding baby bond, which will not provide a larger portion of its return until November 2026. While the baby bonds are not rated, they are trading well above the corporate averages and above the BB-rated averages.

FINRA

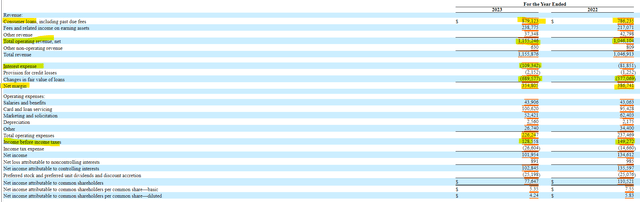

In terms of financial performance, Atlanticus experienced a similar trend to other consumer lenders in 2023 with both higher interest income and higher interest expense. The company was able to grow interest income by nearly $100 million on consumer loans and overall income by more than $100 million when including fees while growing interest expense by only $28 million. What’s interesting (and different) is that interest expense is a less important factor in net margin.

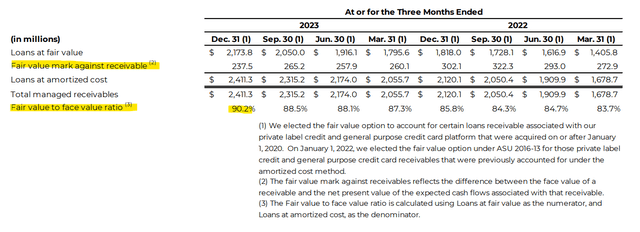

Atlanticus uses the fair market value method when valuing its loans. This method has advantages and disadvantages. An advantage is that the company does not need to maintain a credit loss allowance against its loans. When a loan is underperforming, the company either writes it down or writes it off. A disadvantage is when the performance of the loans is declining, the write-offs can become a headwind to earnings and strain the balance sheet. In the case of Atlanticus, declines in fair market value outpace interest expense by more than 6 to 1. Despite the headwinds, Atlanticus generated $355 million in net margin or 30% of interest income.

SEC 10-K Earnings Presentation

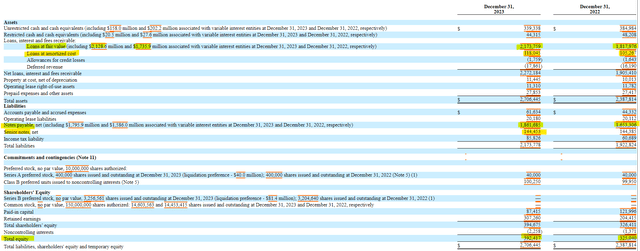

Atlanticus does hold loans at amortized cost, but when looking at the balance sheet, investors can tell those loans for less than 5% of total loans and consist of mostly automotive loans. The company grew its consumer loans by more than $350 million during 2023. A good part of the funding source for this was a $200 million increase in notes payable. The company shrank its leverage ratio from 5.9 to 5.5. Shareholder equity grew by more than 20% to $392 million.

SEC 10-K SEC 10-K

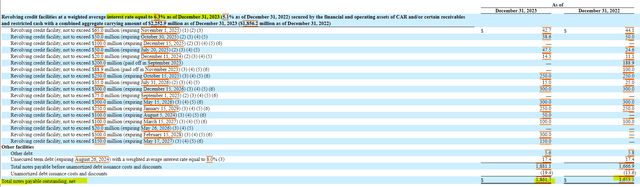

Atlanticus carries a variety of revolving credit facilities with maturity dates ranging from August 2024 through January 2029. The laddering of these loans allows the company to manage its debt maturities in an orderly fashion and avoid large balances of maturing debt. There are also rested lines of credit representing an ability for the organization to access liquidity on top of its $339 million in cash. The average interest rate on the revolving lines is a modest 6.3%. The company clearly has the liquidity in place to navigate a downturn.

SEC 10-K

While I’m not seeing anything in the current financials to negate an investment in Atlanticus Holding’s debt, there are risks that investors must be aware of. First, because of the market that Atlanticus serves, it is susceptible to spikes in defaults. These spikes are especially prevalent if macroeconomic indicators, such as employment, erode. The percentage of loans more than 90 days past due did jump to over 10% in the fourth quarter and investors should keep a close eye on this figure if unemployment begins to rise.

SEC 10-K

Another risk for Atlanticus Holdings is regulatory risk. Politicians have been setting their sights on “payday” lenders. Atlanticus is not necessarily in that category, but with an average yield of 40%, it is possible that politicians may try to cap interest rates on lenders below those levels. This is problematic as Atlanticus’ net interest margin is currently under 8%. A capping of rates would impact Atlanticus’ growth prospects and earnings margins.

SEC 10-K

The risks to Atlanticus are keeping me away from the common and preferred shares, as those equity instruments will bear the brunt of any macroeconomic changes. The company would need to default to impact the interest payments and principal on its baby bonds. Currently, I see default as a highly unlikely scenario. The 2029 maturing baby bond will give income investors a great income yield of over 9%.

Read the full article here