")

Twilio (NYSE:TWLO) remains seemingly one of the few tech stocks which still trades at cheap valuations. That isn’t completely undeserved. The company has posted muted top-line growth during a period in which many tech peers have already begun to see some acceleration. Still though, there’s plenty of reasons to stick by the stock. The company maintains over $3 billion in net cash, making up just over 25% of the market cap, and management has committed to aggressive share repurchases alongside a credible timeline to GAAP profitability. TWLO is no longer the exciting and high-flying tech stock that it was during the pandemic, but at these valuations it doesn’t have to be. I reiterate my buy rating for the stock as the valuation remains too cheap.

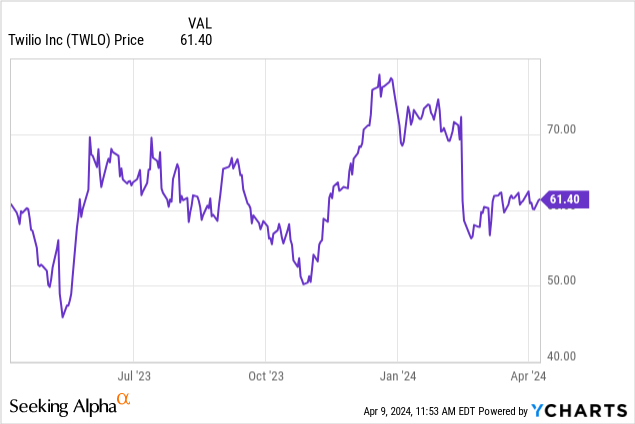

TWLO Stock Price

I last covered TWLO in January where I called it a “rare value stock in the tech sector.” The stock has since underperformed the broader market by around 20%.

Some of that underperformance undoubtedly is due to dampened enthusiasm for activist change, but it also creates yet another buying opportunity in the name.

TWLO Stock Key Metrics

TWLO is a customer engagement platform helping companies to advertise products and services to customers, often through SMS

Twilio

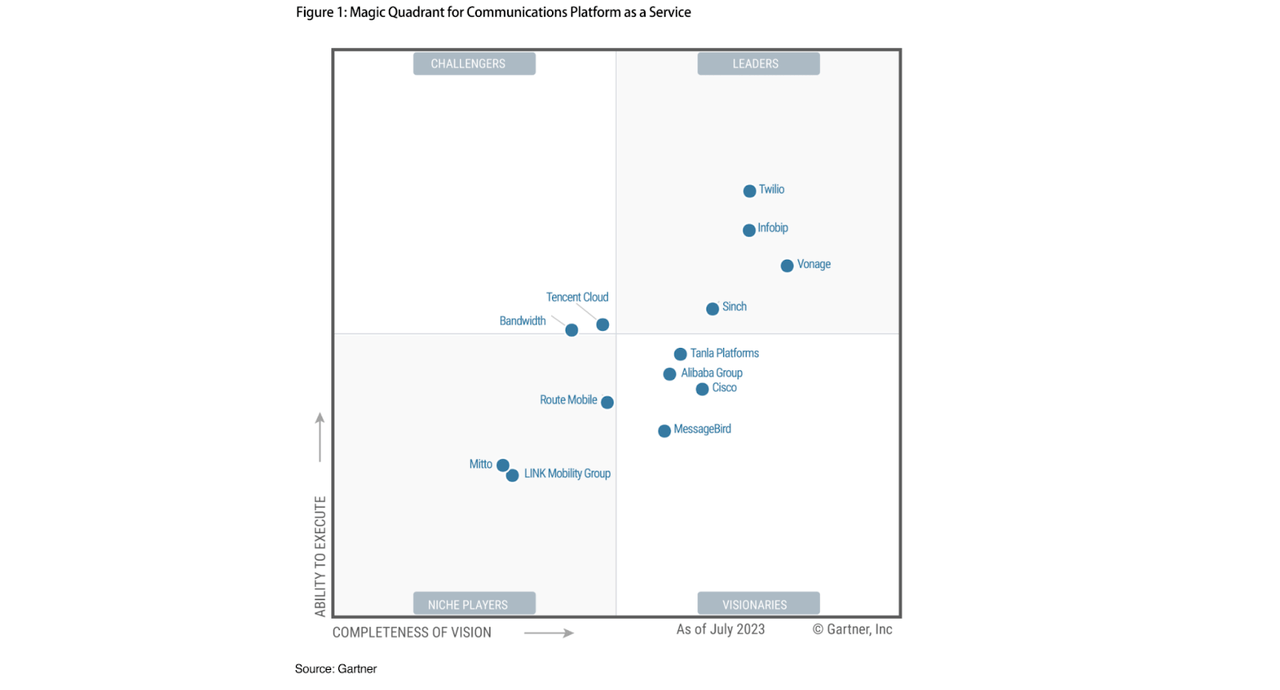

TWLO is among the most well known platforms in this highly competitive sector.

Twilio

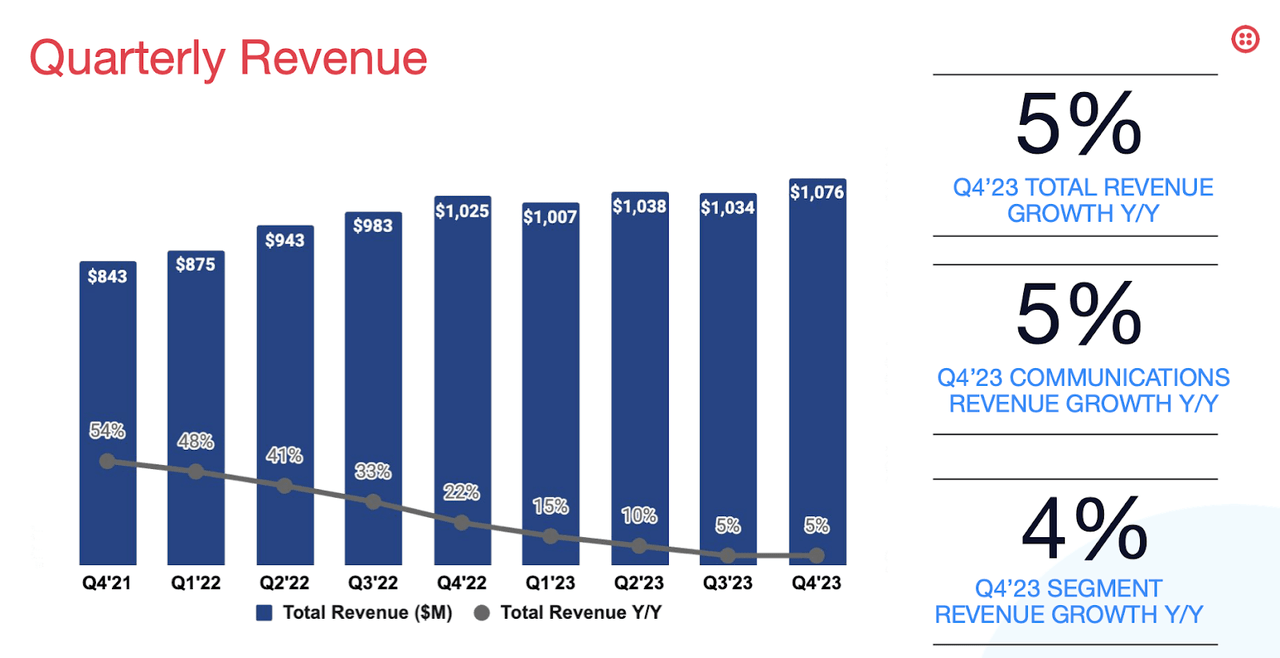

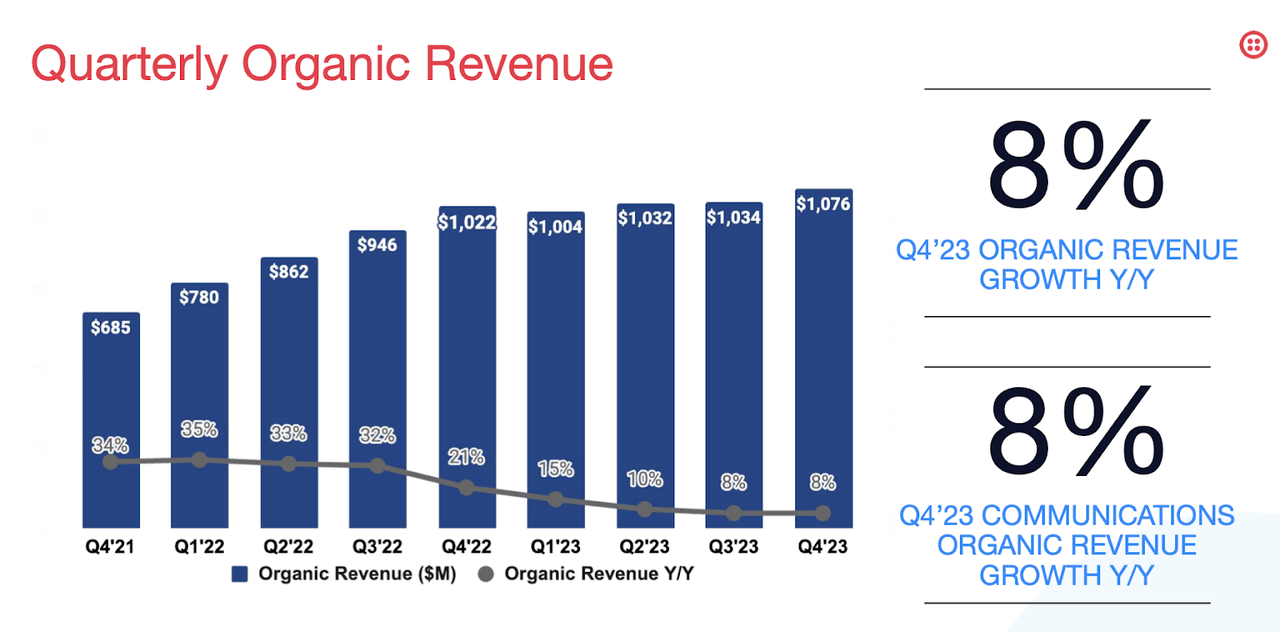

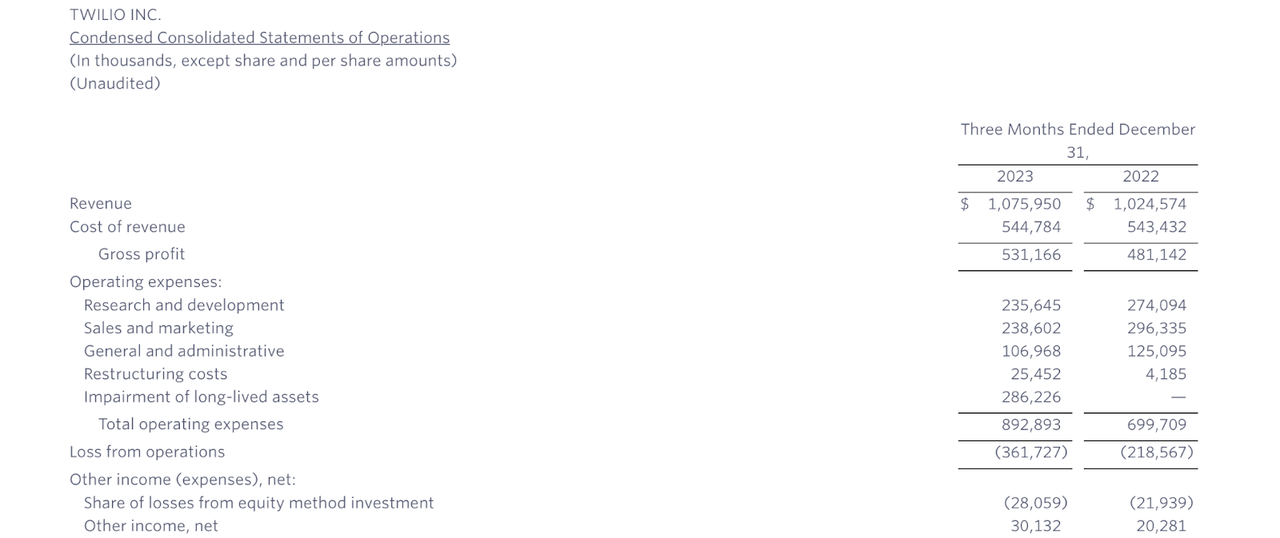

In its latest quarter, TWLO generated 4% YoY revenue growth to $1.076 billion, surpassing guidance for $1.04 billion.

2023 Q4 Presentation

On an organic basis, TWLO saw revenue jump 8% YoY. Recall that TWLO had exited some underperforming businesses last year.

2023 Q4 Presentation

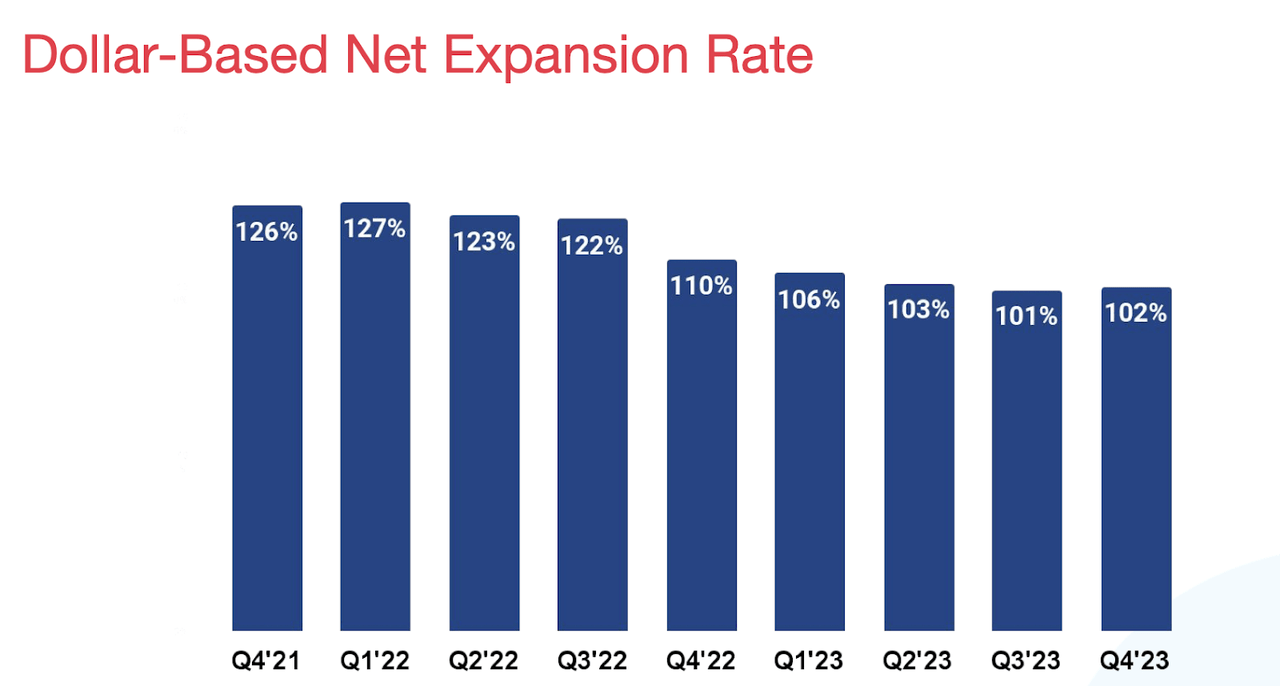

The company saw its dollar-based net expansion rate tick up slightly to 102%, with Segment dragging down results at 96%.

2023 Q4 Presentation

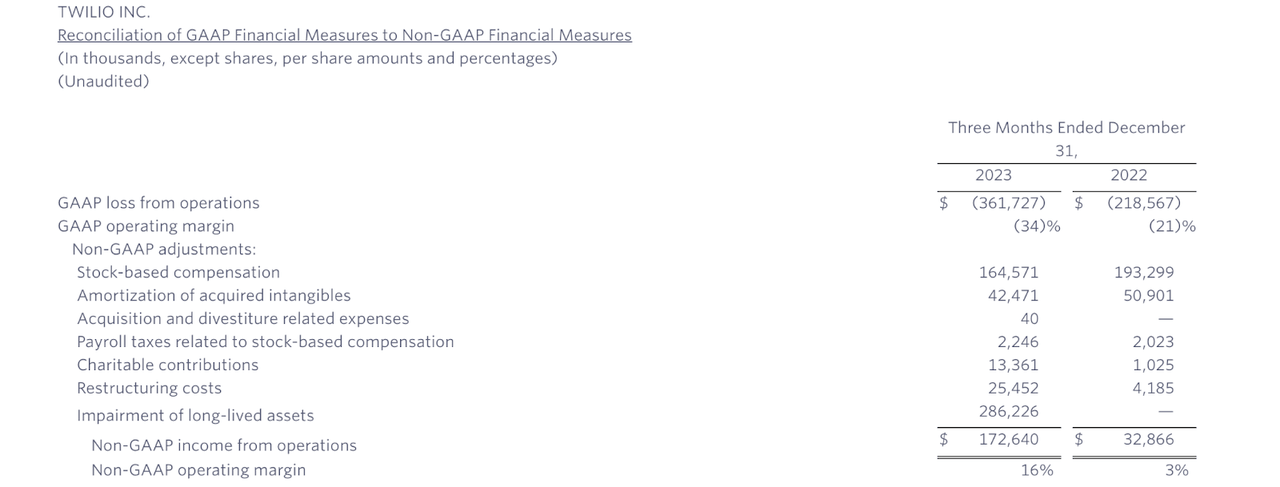

The company has sought to offset slow top-line growth with consistent margin expansion. Non-GAAP operating income totaled $173 million, surpassing management guidance for $125 million and representing a 16% margin. It is notable that non-GAAP margins have risen an astonishing 13% year over year, and the company essentially generated positive operating income even after including stock-based compensation.

2023 Q4 Press Release

TWLO ended the quarter with $4 billion of cash versus $989 million of debt, representing a pristine balance sheet.

Looking ahead, management has guided for the first quarter to see up to 3% YoY revenue growth to $1.035 billion (versus consensus estimates of $1.03 billion) and non-GAAP EPS of $0.60 (versus consensus estimates of $0.59).

2023 Q4 Presentation

That implies a sequential decline in revenue, but as noted on the conference call, is due to “elevated seasonal activity” that is not expected to recur in the first quarter.

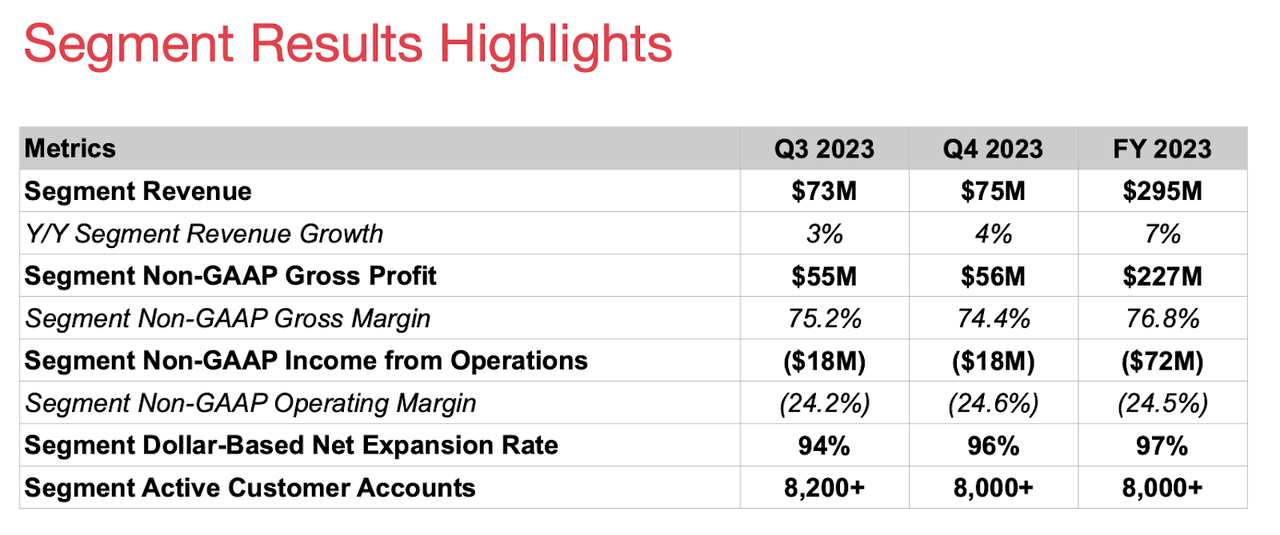

Much investor attention has likely been on the fate of Segment, which TWLO acquired for $3.2 billion in stock in 2020. Segment has been a disappointing acquisition and even 3 years later, generated just $295 million in revenues for the year.

2023 Q4 Presentation

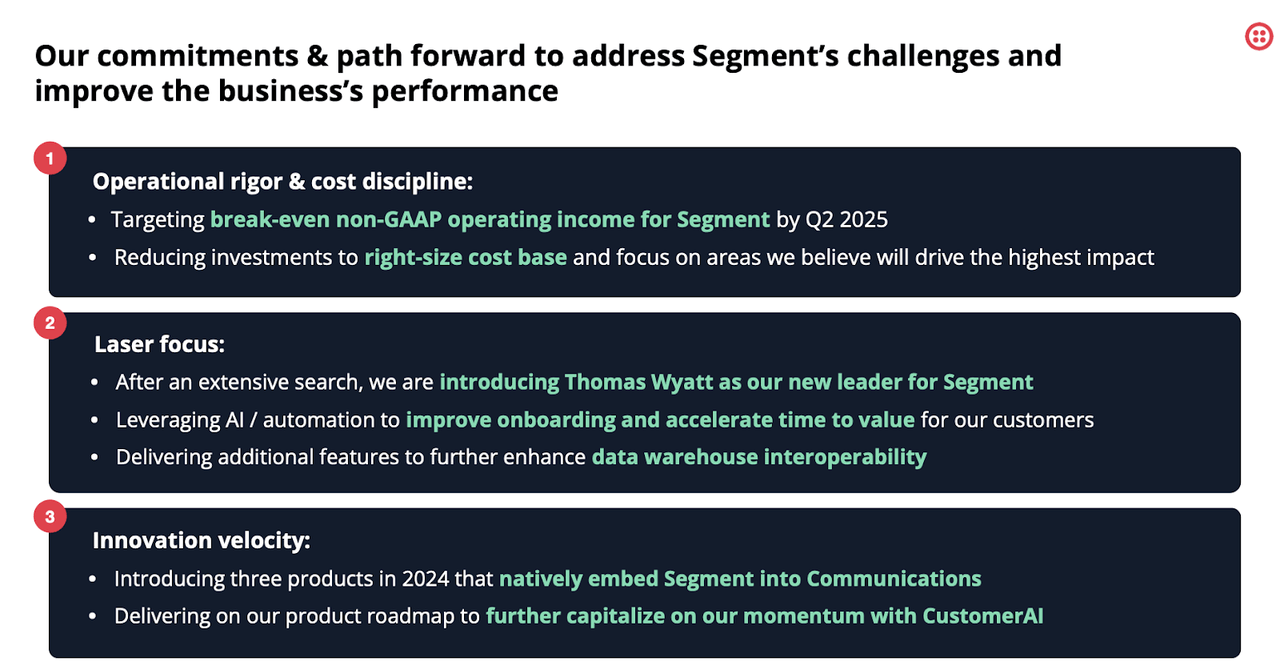

Management had hinted that they were considering selling off the business line, but has recently indicated that they instead intend to stay together. Management gave ambitious targets for Segment, including break-even non-GAAP operating income by the second quarter of 2025, as well as integrating generative AI into the product.

March Investor Update

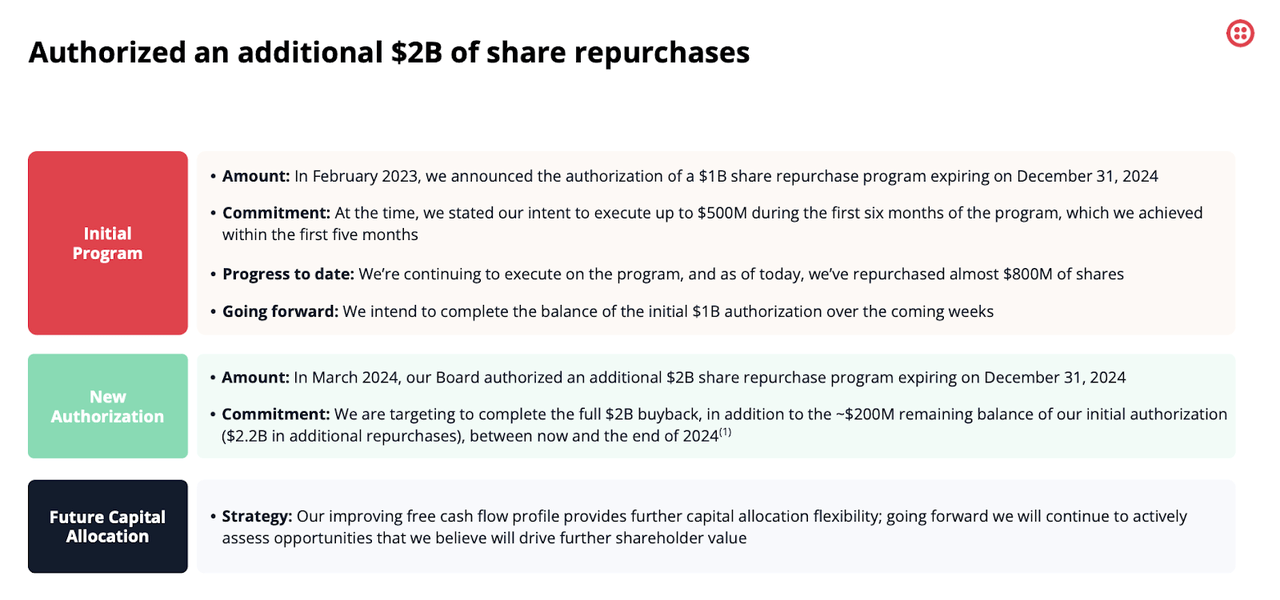

Management also authorized an additional $2 billion share repurchase program, which they expect to complete this year (there’s also $200 million authorized under the prior program). My guess is that management is hoping that the increased share repurchase program might appease investors who were otherwise hoping for a sale of Segment. This implies that the company might acquire roughly 19.7% of shares outstanding this year.

March Investor Update

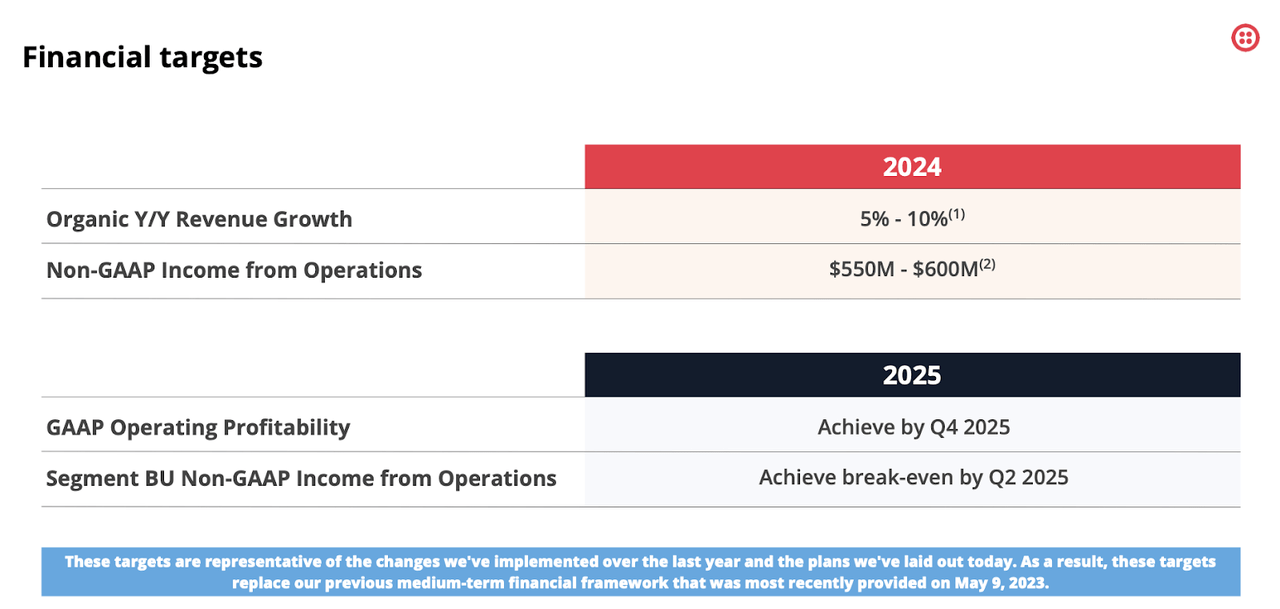

Management also gave new targets, including up to 10% organic revenue growth and $600 million in non-GAAP operating income for the year, as well as achieving GAAP operating profitability by the fourth quarter of 2025.

March Investor Update

That GAAP operating profitability target looks achievable, given that the company posted a 7% GAAP operating margin loss (excluding impairment costs) in the fourth quarter. I expect operating leverage and continued cost discipline to allow the company to achieve this profitability milestone, if not sooner. I also note that the company generated $77.7 million in interest income for the full-year, meaning that the company might reach positive GAAP net income even sooner.

2023 Q4 Press Release

TWLO had previously seen its stock jump due to activist involvement. Activist Anson Funds commented that while they were encouraged by some of the recent changes, much work is left to do. But I think that the large share repurchase program is already a big concession and represents the most important near term catalyst for the stock.

Is TWLO Stock A Buy, Sell, or Hold?

TWLO has joined the ranks of seemingly every other tech stock in embracing generative AI in its products – it touts being able to seamlessly create marketing campaigns for customers.

Twilio

Even so, TWLO has not bounced as strongly as many other tech stocks and this is reflected in the conservative valuation, with the stock trading at 22x non-GAAP earnings.

Seeking Alpha

The low valuation is even more evident on a price to sales basis, with the stock trading at 2.5x this year’s sales estimates. The stock looks cheap even after adjusting for the low 50% gross margin.

Seeking Alpha

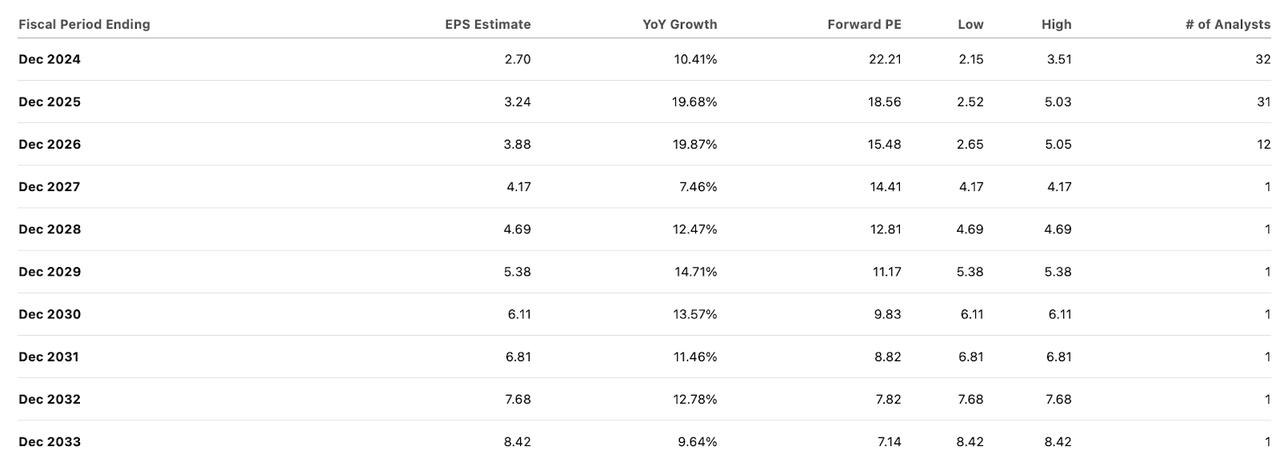

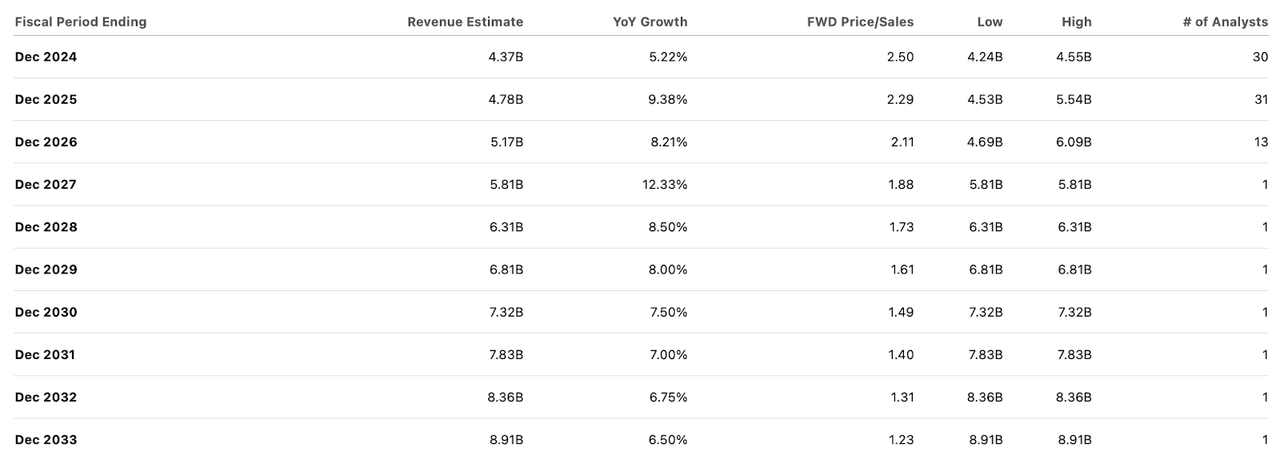

If management is able to execute against the high end of their 5% to 10% organic revenue growth target for 2024, then overall revenues may hover in excess of $4.56 billion, which would surpass consensus estimates of $4.37 billion. However, investors can not be blamed for having low confidence in management’s ability to outperform revenue growth targets, as revenue growth has been a real struggle since the pandemic. I no longer expect a return to management’s target of 15% to 25% revenue growth, as outlined in their 2022 Investor Update. I instead target a 15x earnings multiple which, assuming 20% long term net margins implies a 3x sales target. That implies solid upside between multiple expansion and ongoing growth. I view 3x sales to be an appropriate target due to the net cash balance sheet and management commitment to driving further profitability gains. Management’s revamped $2 billion share repurchase program ($2.2 billion inclusive of the previously authorized program) is the main near term catalyst.

What are the key risks? Whenever we are faced with a slow-growing tech stock, an important risk to consider is for the slow growth to turn negative. While management appears optimistic that revenue growth can accelerate, I again note that management has not had a great history of exceeding or even meeting top-line growth expectations as of late. It is potentially concerning that top-line growth has not yet accelerated given that many other tech names in my coverage universe have already been reporting an improvement in the macro environment. While management has not conducted any significant M&A in recent years, I mustn’t ignore management’s poor track record of M&A with Segment being the most notable. It is possible that management does not follow through on their share repurchase plans and instead embarks on an expensive acquisition. If the company is unable to drive further profitability gains, then the valuation may come under pressure, as my target hinges on management’s ability to continually work towards long term margin targets.

Conclusion

Management continues to promise accelerating top-line growth but Wall Street appears skeptical. Even so, between the net cash balance sheet, improving profit margins, and huge share repurchase program, there are enough reasons to buy the stock at 2.5x sales. I reiterate my buy rating for the stock.

Read the full article here