Stubbornly strong economic data has led to significant shifts in market expectations for when, and how quickly, the Federal Reserve will begin cutting policy rates.

Our own forecast is now for the first rate reduction to come in September, but the complications of starting an easing cycle just before the U.S. Presidential election does insert significant uncertainty.

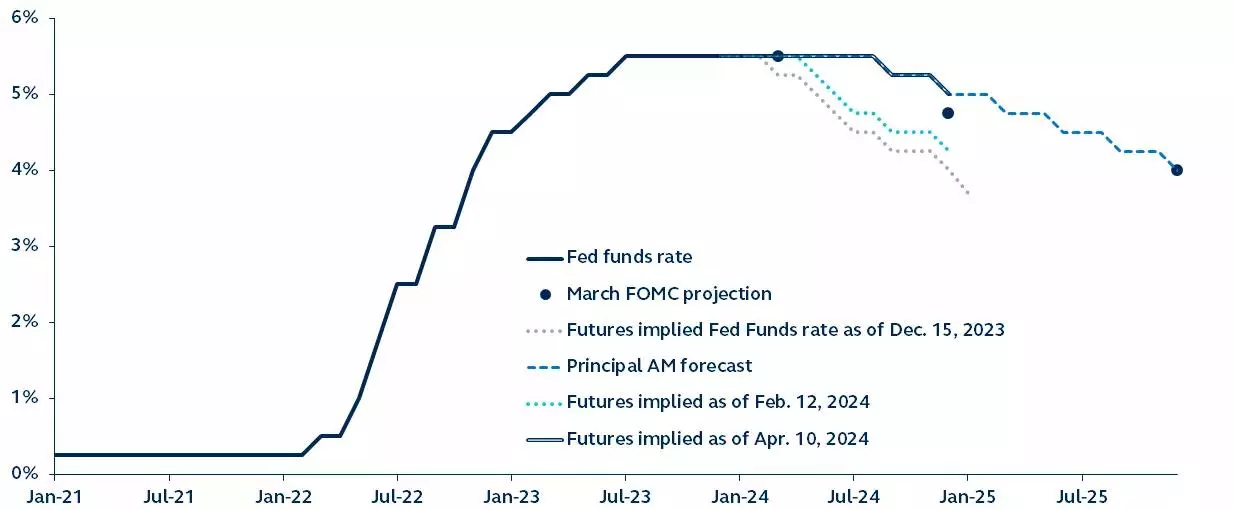

Federal Reserve policy rates path

Fed funds rate and projections, 2021–present

Source: Federal Reserve, Bloomberg, Principal Asset Management. Data as of April 10, 2024.

The past few months have been a particularly volatile period for Federal Reserve (Fed) policy rate forecasts. March’s CPI report was the latest in a series of upside inflation surprises, and means that the stalled disinflationary narrative can no longer be considered a blip.

Financial market expectations have now shifted from six rate cuts to just two cuts this year – fewer cuts than the Fed’s own projections.

Chair Powell has made it abundantly clear that he wants to cut rates this year. Not only has he been downplaying the importance of recent inflation prints, but upward revisions to the Fed’s growth and inflation forecasts have not prompted any changes to their near-term policy path projection. The Fed continues to expect 75 basis points of cuts this year.

The continued strength of the U.S. economy suggests that only one rate cut is likely required, yet the Fed’s clear desire to cut rates shouldn’t be overlooked.

As such, and assuming the resumption of 2023’s disinflation trend, we have revised our forecast from three cuts to two cuts in 2024, with the first reduction coming in September.

There is a significant risk to this forecast – November’s U.S. Presidential election – commencing a rate cutting cycle immediately ahead of November’s elections may be a bridge too far for the Fed.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here