")

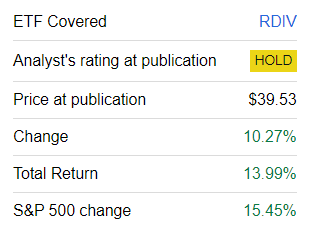

Continuing my series of updates on dividend ETFs, today I would like to offer a fresh look at the Invesco S&P Ultra Dividend Revenue ETF (NYSEARCA:RDIV), which I previously assessed in August 2023, concluding with a Hold rating.

Why we should discuss RDIV once again? As this is a high-turnover, highly selective dividend strategy with quarterly rebalancing, we should analyze the differences in portfolio composition that might have emerged and what factor changes they might have resulted in. Next, we should discuss whether the growth, quality, and value combination the ETF is offering at the moment is optimal for the current market regime or not.

What is RDIV?

According to its website, RDIV’s strategy is based on the S&P 900 Dividend Revenue-Weighted Index. As we know from the methodology summary provided in the fact sheet, the idea is to select 60 generous dividend payers from the S&P 900 (which is itself the S&P 500 plus the S&P 400) in four steps:

- remove the key 5% of the S&P 900 constituents with the highest dividend yields, which, as I have already explained in the previous notes, might have a function of a simple value-trap screen (assuming how robust RDIV’s quality characteristics are, this unsophisticated method is obviously working);

- remove “the top 5% of securities within each sector by dividend payout ratio;” I should add here that this is another value-trap, dividend durability screen;

- select 60 names with the highest dividend yields;

- adjust their weights using the revenue factor, also applying a 5% single-company cap.

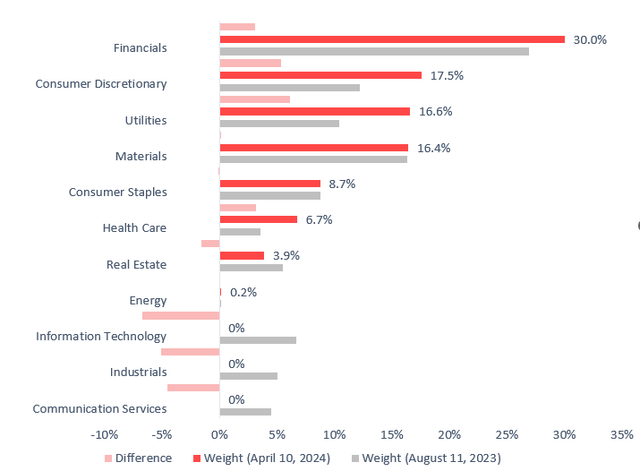

Importantly, the index is not supposed to provide exposure to all 11 GICS sectors. To corroborate, as of April 10, there were just 8 sectors in this portfolio, as communication, information technology, and industrials were absent.

Created by the author using data from RDIV

Moreover, RDIV’s weighting principles result in some peculiarities, as there were 18 financials in this basket that accounted for roughly 30% of the net assets as of April 10. At the same time, there were 16 real estate players with only 3.89% weight.

What has changed in the RDIV portfolio?

Since my August 2023 article, RDIV’s underlying index has been rebalanced twice, in October and January, with the next rebalancing due this April. As a consequence, holdings accounting for about 30.5% of the ETF’s portfolio as of August 11 were removed. The five most notable removals were as follows:

| Stock | Sector | Weight (as of August 11, 2023) |

| Intel (INTC) | IT | 5.25% |

| 3M (MMM) | Industrials | 5.08% |

| Paramount Global (PARA) | Communication | 4.5% |

| Truist Financial Corporation (TFC) | Financials | 4.37% |

| Advance Auto Parts (AAP) | Consumer Discretionary | 1.65% |

Created using data from the ETF

Below are the five largest additions:

| Stock | Sector | Weight (as of April 10, 2024) | DY TTM |

| Ford (F) | Consumer Discretionary | 5.695% | 4.6% |

| Nordstrom (JWN) | Consumer Discretionary | 2.198% | 3.8% |

| T. Rowe Price Group, Inc. (TROW) | Financials | 0.988% | 4.2% |

| Agree Realty (ADC) | Real Estate | 0.072% | 5.2% |

| Entergy (ETR) | Utilities | 2.007% | 4.2% |

Created using data from Seeking Alpha and the ETF

What are RDIV’s factor characteristics? Here, despite 19 holdings out of 60 removed, we see just minor, mostly cosmetic changes. Overall, this is a predominantly large-cap, high-yield, deeply undervalued, top-quality mix with unappealing growth characteristics (including nuances on the dividend front). Let me elaborate on that below.

Value

RDIV remains an excellent option for value maximalists who are on the lookout for dividend opportunities in the large-cap universe.

| Metric | April 2024 | August 2023 |

| Market Cap, $ billion | 45.59 | 44.25 |

| EY | 5.65% | 4.9% |

| P/S | 1.94 | 1.90 |

| DY | 4.72% | 4.88% |

| Quant Valuation B- or higher | 86.7% | 82.1% |

| Quant Valuation D+ or lower | 1.45% | 1% |

Calculated by the author using data from Seeking Alpha and the ETF

Its weighted-average market cap has risen slightly, mostly as a consequence of the capital appreciation of the holdings. In this mix, mid-caps account for 16.3% of the net assets, which is almost on par with the ETF’s allocation to mega-caps, 14.7%, as per my calculations. We also see a solid improvement in the WA earnings yield. The median EYs are on par: 6.2% in August vs. around 6% in April. Adjusted for the impact of loss-making companies, the EY stood at 6.9% in August and at 6.1% in April.

For context, below are the earnings yields of the S&P 400 and the S&P 500 indices, calculated using P/E data from the websites of the SPDR S&P MIDCAP 400 ETF Trust (MDY) and the SPDR Portfolio S&P 500 ETF (SPLG).

| Index | EY |

| S&P 400 | 5.6% |

| S&P 500 | 3.9% |

Also, I should note that the share of holdings with the B- Quant Valuation rating or higher is so large that I would call RDIV an ETF with pure-value characteristics.

Quality

RDIV’s portfolio is a perfect illustration of how a profound value tilt can be achieved without compromising on quality, as illustrated by the weight of the holdings with a B- Quant Profitability rating or better.

| Metric | April 2024 | August 2023 |

| ROE | 9.34% | 22.1% |

| ROA | 2.45% | 6.69% |

| Quant Profitability B- or higher | 76.73% | 81.1% |

| Quant Profitability D+ or lower | 8.33% | 6.5% |

Calculated by the author using data from Seeking Alpha and the ETF

However, there are nuances. For example, Return on Assets is obviously too low, with the key detractors being the financial and utilities sectors.

Growth

Nevertheless, when it comes to balancing inexpensiveness, quality, and growth, something must be sacrificed, and in the case of RDIV, it is the growth factor.

| Metric | April 2024 | August 2023 |

| EPS Fwd | -1.22% | -9.4% |

| Revenue Fwd | -0.07% | 1.3% |

| Quant Growth D+ or lower | 45.6% | 71.9% |

Calculated by the author using data from Seeking Alpha and the ETF

The key reasons for the weighted-average growth rates being negative are that 41% of the holdings are forecast to deliver lower revenues going forward, while EPS contraction is likely for 42% of the companies, as we can deduct from pundits’ estimates.

Dividend characteristics: sizable yields at the expense of growth

RDIV’s portfolio is offering a fairly appealing weighted-average dividend yield of 4.7%. To give a bit more color, the DYs range from Ally Financial’s (ALLY) 3.16% to Crown Castle’s (CCI) 6.45%. RDIV itself has a TTM DY of 4.09% as of writing this article.

On the negative side, the dividend growth characteristics of its high-yield holdings are rather lackluster, and they have even deteriorated since August 2023.

| Metric (weighted average) | April 2024 | August 2023 |

| Div Growth 3Y | 4.72% | 6.06% |

| Div Growth 5Y | 4.03% | 6.69% |

Calculated by the author using data from Seeking Alpha and the ETF

However, a nuance here is that the key contributor to the dividend CAGRs was AAP, which is no longer in the portfolio. The adjusted 3-year CAGR as of August was 3.8%, while the 5-year CAGR stood at 5.3%.

Investor Takeaway

In sum, RDIV’s portfolio comprises mostly large-cap, high-yield, grossly underpriced, top-quality companies with unappealing growth characteristics.

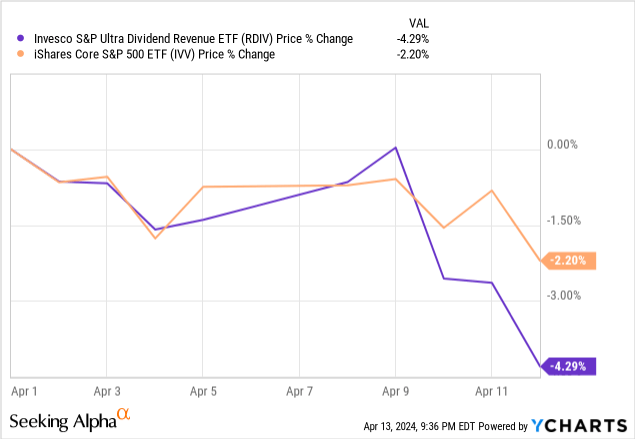

Does RDIV’s exceptional deep-value profile offer an opportunity at the moment? It may offer it. The market is hardly happy with the recent CPI surprises and Brent price currently teetering around $91 a barrel, which is obviously an inflationary factor that will continue playing out going forward. It is no surprise investors are nervous, as the very narrative of this market rally based on a probably excessively optimistic interest rate cut schedule is jeopardized. This nervousness is percolating into stock prices, with the iShares Core S&P 500 ETF (IVV) down by around 2.2% in April. And RDIV might look like an excellent play for a value rotation. For context, the ETF performed phenomenally during hawkish and bearish 2022, delivering a 7.14% total return, while IVV was down by 18.16%. However, there are a few reasons why I am still neutral on RDIV.

First, it seems the ETF has been even more sensitive to the recent softness than IVV.

RDIV has also underperformed the S&P 500 index since my August article.

Seeking Alpha

Second, since its reorganization in 2019, it has underperformed both IVV and MDY, delivering a maximum drawdown of 40.4% and a disappointing downside capture ratio of 112.7%.

| Portfolio | IVV | RDIV | MDY |

| Initial Balance | $10,000 | $10,000 | $10,000 |

| Final Balance | $20,643 | $15,904 | $17,884 |

| CAGR | 16.18% | 10.08% | 12.78% |

| Stdev | 18.31% | 26.29% | 22.13% |

| Best Year | 28.76% | 27.93% | 24.21% |

| Worst Year | -18.16% | -10.37% | -13.28% |

| Max. Drawdown | -23.93% | -40.38% | -29.63% |

| Sharpe Ratio | 0.8 | 0.42 | 0.56 |

| Sortino Ratio | 1.27 | 0.63 | 0.86 |

| Market Correlation | 1 | 0.82 | 0.94 |

Data from Portfolio Visualizer. The period is June 2019–March 2024

Besides, its growth exposure and soft dividend growth are worrisome. All in all, the Hold rating is maintained.

Read the full article here