")

Thesis

Shift4 Payments’ (NYSE:FOUR) stock saw a massive spike after reporting Q4 earnings. This was likely due to the combination of a good earnings report/guidance and M&A speculation. No M&A activity ended up taking place, and since then the stock has declined precipitously. We believe the recent selloff is overdone and that long-term investors can acquire shares at an attractive valuation.

The Basics

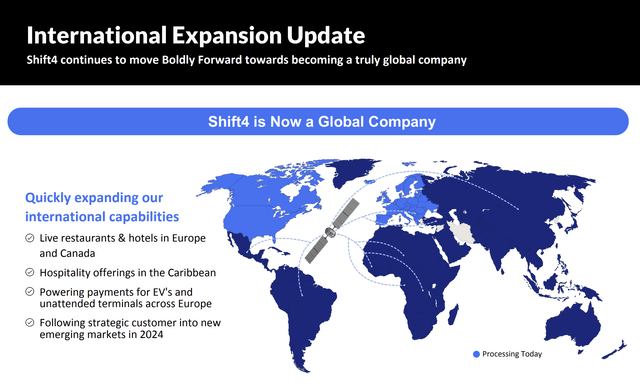

Shift4 is a payments processor, though they do have some software/website offerings through their SkyTab platform. Their main markets are located in the United States, Canada, and Europe. They are looking to continue expanding their international footprint, and investors should monitor how this expansion is progressing over the coming quarters.

Shift4’s Q4 2023 Shareholder Letter

Shift4’s main operating segments are SkyTab (restaurants), Hospitality, Specialty Retail, and Sports & Entertainment. The company is seeking to grow its presence in non-profit services as well as gaming (gambling), which are relatively new markets for them.

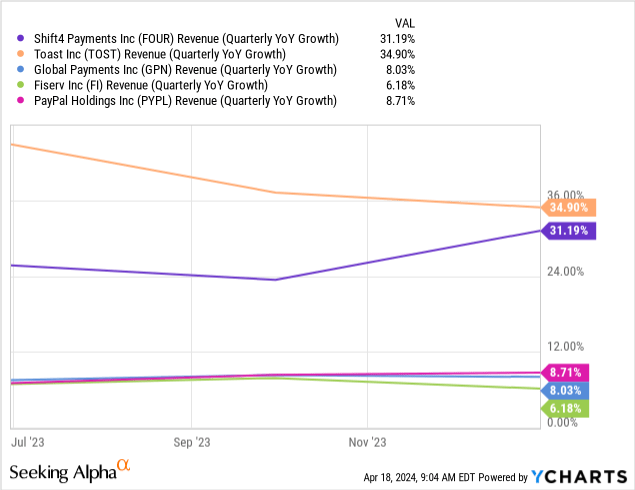

The strong financial performance and guidance is what draws us to the company. In their most recent quarter Shift4 reported gross revenue less network fees of $269.3 million, which was up 35% year over year. They also reported adjusted EBITDA of $136.1 million, which was up 44% year over year. These are healthy growth metrics when compared to other companies in their industry.

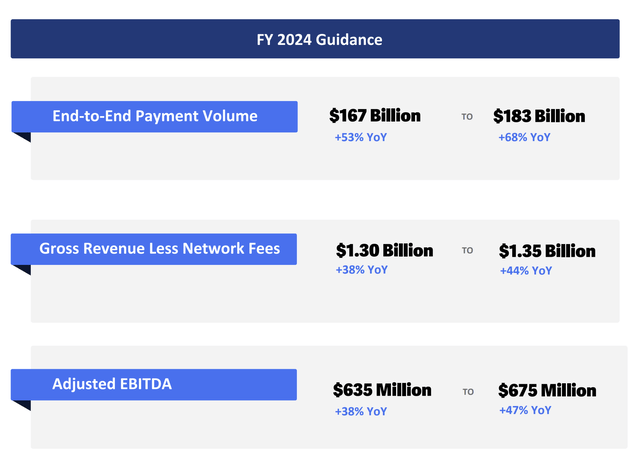

Shift4 provided strong 2024 guidance, which can be seen below. A midpoint of 41% growth in gross revenue less network fees suggests that growth is accelerating from the year-over-year growth reported in Q4. This top-line growth is expected to fuel similar levels of growth for 2024 adjusted EBITDA.

2024 Guidance (Shift4’s Q4 2023 Shareholder Letter)

Some additional factors to be aware of:

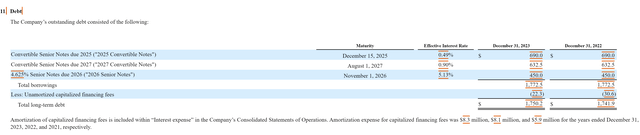

Shift4 has roughly $1.75 billion in debt, and this debt is a mix of convertible and non-convertible. Some of this debt will likely need to be refinanced at higher rates. We don’t see this as being a major issue over the long-term, as the company will either issue new convertibles or will issue new fixed rate debt. The company will be able to easily absorb higher interest costs thanks to their profitability, although it would be a drag on earnings over the short term.

Debt Summary (Shift4’s 2023 10-K)

Shift4 has a founder CEO (Jared Isaacman). Having a founder CEO is generally viewed as a positive because of the alignment of interest with shareholders as well as their substantial amount of skin in the game, both mentally and monetarily. It does, however, introduce the risk of the stock potentially having a negative reaction if the founder leaves.

M&A Speculation

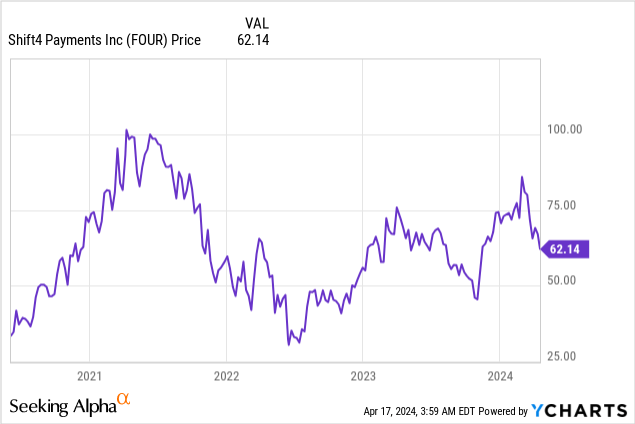

There has been M&A speculation regarding Shift4 for a couple of months now. On February 28, there was news of an apparent bidding war for the company. The combination of this news and the strong earnings report likely contributed to the strong surge in their stock over the following two days. This M&A premium quickly began to deflate when Amadeus stated they were not interested in a deal. Over the March 16-17 weekend, the Shift4 CEO sent out a memo to staff stating that the company had rejected all potential bids, and that they received multiple bids over the stock price (at the time). Since then, the stock has been on a relentless decline, and is now trading well below where it was before reporting Q4 earnings.

We believe that much of the volatile price action this year has been influenced by M&A speculators, and that the company’s rejection of all offers has led to many of these speculators dumping their position. The buyout rejection and share price decline may have also spooked some buy and hold investors, resulting in more selling pressure on the stock.

Important to note is that payments company Nuvei was recently taken private at an EV/EBIDTA premium to where Shift4 is currently valued. Given Shift4’s higher growth rates, this seems to bode well for the value of Shift4 if it did end up getting acquired.

At the end of the day the M&A discussion is just noise. Long-term investors can use moments of uncertainty such as these as a time to pick up discounted shares in good companies.

We do believe that M&A remains possible over the next 24 months. However, it’s not core to our investment thesis.

Price Action and Valuation

Shift4’s stock has been trending sideways over the past couple of years, and remains well below the all-time high reached in 2021. The stock is down 16.4% year to date and is down 32.6% from its 52-week-high.

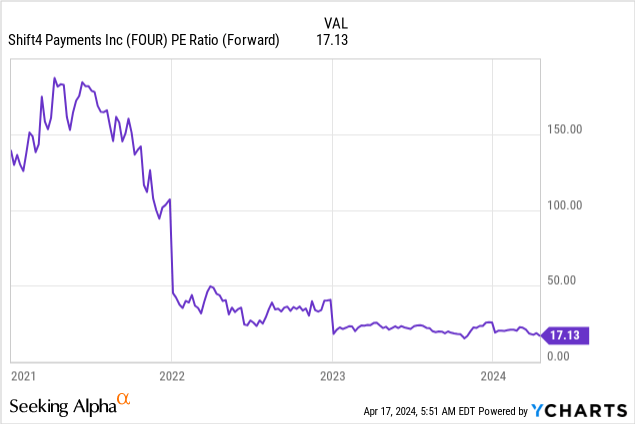

While we normally stick to GAAP net income, in this case, we view adjusted EBITDA as being a reasonable metric to use. This is because the company has a substantial amount of non-cash costs such as depreciation/amortization and impairments. For those solely interested in GAAP metrics, Shift4 trades at a forward PE ratio of 17.13, which looks more than reasonable considering the expectation for top and bottom-line growth to exceed 40% over the next 12 months.

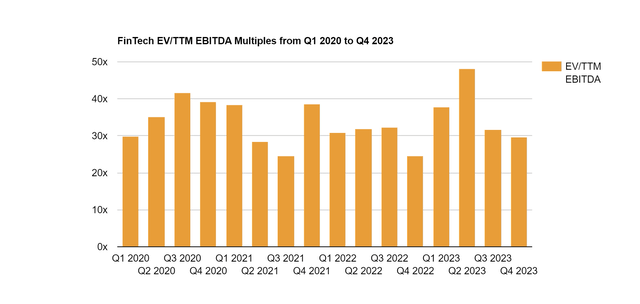

As far as adjusted EBITDA is concerned, the company currently trades at a trailing EV/EBITDA valuation of 14.4, and a forward EV/EBITDA valuation of 10.1. This looks cheap when compared to the industry average multiple of around 30x trailing EV/EBITDA.

Fintech Industry EV/EBITDA Multiples (Software Equity Group)

This valuation discount to their sector appears unwarranted, given the company is expecting to grow their top and bottom line by 40%+ over the next year. For reference, Fiserv (FI) trades at a forward EV/EBITDA of 12.7 while forecasting topline growth of 15-17%. PayPal (PYPL) trades at a forward EV/EBITDA of 9 with revenue growth guidance of 6.5-7%.

We believe that Shift4’s stock should trade at a forward EV/EBITDA multiple of 15 times given their expected growth rate. This would equate to a share price of around $93 at the midpoint of EBITDA guidance. We would consider selling our position at that level if growth expectations remain the same.

Risk Factors

A risk to our bullish thesis is the competitive nature of the payments industry. It’s possible that Shift4 is unable to achieve their ambitious growth targets. Competition could also pressure their margins going forward.

Another risk is the possibility for the CEO to take the company private in a transaction that benefits himself more than it benefits shareholders. This seems unlikely to us but it’s never completely off the table.

We view the overall risk/reward as being favorable.

Key Takeaway

Shift4 Payments has been involved in M&A speculation which ultimately never materialized, and the stock has since sold off. The fundamentals of the company remain intact and we view this sell-off as a buying opportunity.

Read the full article here