")

My last article regarding Northwest Bancshares (NASDAQ:NWBI) was almost a year ago, and a lot has changed since then. The cost of deposits was rising but was not a concern at all; today, however, it is because it is not being offset by rising asset yields. All this is leading to a decline in net interest income/margin.

In addition, unrealized losses on fixed-rate securities have not improved, and the bank has decided to sell some of them at a loss.

Q1 2024 has disappointed my expectations and the price per share is heading for strong support at $10 per share.

- Non-GAAP EPS of $0.23 in-line.

- Revenue of $131.2M (-3.8% Y/Y) misses by $1.4M.

Profitability down but dividend still sustainable

Northwest Bancshares Q1 2024

Average loans receivable reached $11.34 billion, up 4.20% from the same quarter last year. The same growth was reported for average deposits, the latter amounting to $11.88 billion. As for average borrowed funds there was a reduction of 36.50%; much of these funds had been used to increase liquidity in the troubled period following SVB’s bankruptcy.

At first glance it would seem that not much has changed since last year; perhaps there was even an improvement given the debt reduction. In reality, this is not quite the case.

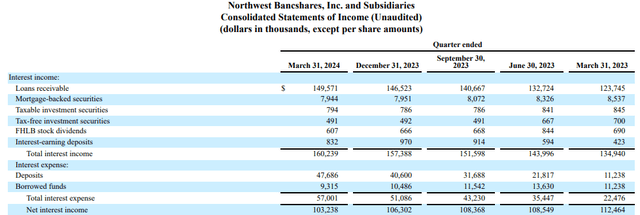

Northwest Bancshares Q1 2024

In this image you can see the total interest income and total interest expenses; compared to Q1 2023, the former increased by 18.74%, the latter by 153.60%. A huge difference and it has led to net interest income declining quarter by quarter over the last year. The speed with which this is happening has even increased in Q1 2024 compared to the previous quarter; thus, it is unclear when the bottom will be reached. But there is more.

TradingView

Our available data stop at March 31, but from April 1 onward the market has discounted only one cut in 2024. The trend does not seem to be stopping, and the scenario of zero cuts in 2024 is no longer so unlikely.

This means that the pressure on the cost of deposits will most likely continue at least until the end of the year, and if inflation worsens, it would continue into 2025. Since the yield on loans is not keeping pace, the solution to boost the net interest margin could be to increase the amount of loans. However, the Loan to Deposit ratio is already quite high, 95%, and demand for credit has taken a hit during the last few quarters-not everyone is willing to borrow at current rates.

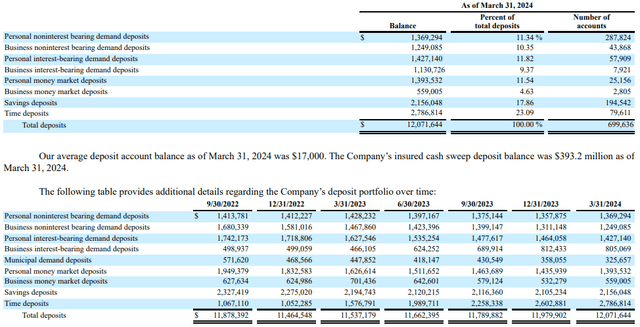

Northwest Bancshares Q1 2024

At the same time, more and more people are willing to get a yield on their savings in line with money market rates. Compared to last year, less expensive deposits have suffered and have been replaced by time deposits. The problem is that the latter have an average cost of 4.37% and negatively affect profitability.

The situation is not the best, but is the dividend at risk? For now, I don’t think so.

Seeking Alpha

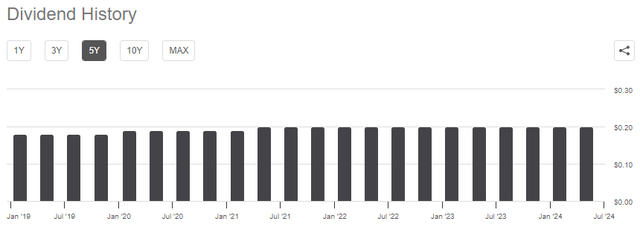

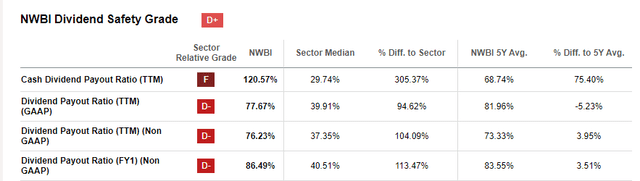

NWBI has been issuing a dividend for decades, and the current yield is almost 7%. This would seem like a golden opportunity, but consider that the growth rate is typically very low.

Seeking Alpha

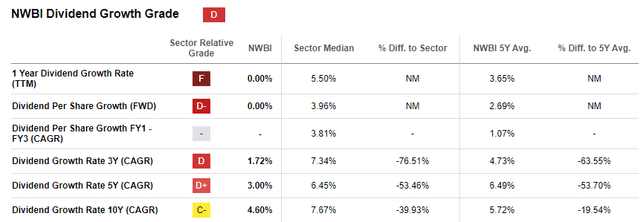

A 4.60% per year over the past 10 years is low, and frankly I would look at other companies with a lower dividend yield but more growth prospects.

Seeking Alpha

Regarding sustainability, the current payout ratio is less than 100% but much higher than the industry median. This does not mean that it will be cut anytime soon, but that in case of earnings distress you cannot rule out a cut. After all, more than ¾ of profits are distributed to shareholders and sooner or later there will be a recession. At that point I am not sure NWBI can sustain the dividend.

News related to the securities portfolio

The main change in this quarterly is management’s willingness to sell at a loss some of the securities purchased when interest rates were close to 0%.

As part of the Company’s ongoing efforts to enhance future profitability, we have proactively chosen to reposition our securities portfolio. By executing this strategic securities transaction, we will significantly improve the Company’s future earnings potential while simultaneously maintaining our robust capital levels and liquidity. This strategic move aligns with our commitment to long-term financial stability and growth, ensuring that we are well-positioned to capitalize on future opportunities and navigate any potential challenges in the market.”

Louis J. Torchio, President and CEO

In a nutshell, underperforming securities will be sold and the proceeds will be used to purchase new ones at current rates, as well as reduce debt. The securities that will be sold will have an average yield of less than 2% and a remaining maturity of more than four years. Those that will be purchased will have a yield up to 400 basis points higher, which will provide a boost to profitability.

Management’s intention is clear, which is to raise liquidity to improve the securities portfolio. Probably, there is not enough demand for new loans. In addition, investing in risk-free bonds positively impacts the calculation of risk-weighted assets, a key component for measuring capital ratios. The latter must necessarily be kept above the minimum threshold, which is something NWBI complies with.

This maneuver will likely result in an after-tax loss of $30 million, which compared to the total unrealized losses, represents only a small fraction.

Northwest Bancshares Q1 2024

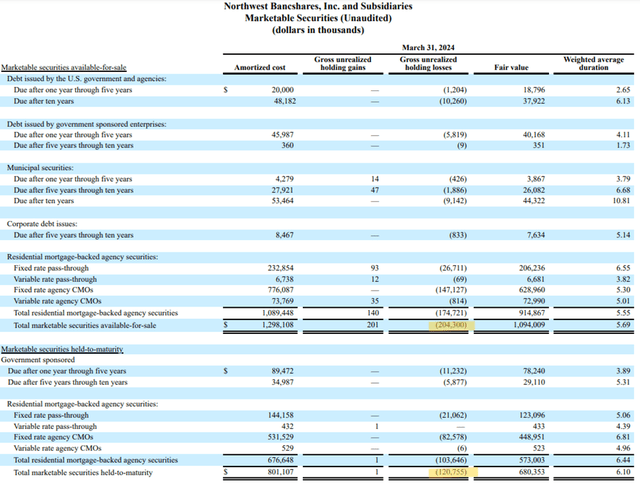

AFS securities at the end of March 2024 had unrealized losses of $204 million; HTM securities of $120 million. By the way, the latter are not accounted for in equity, so they do not impact TBV per share.

If we considered all unrealized losses, they would amount to $325 million, a high figure considering that total equity is $1.55 billion.

Finally, these figures are current as of the end of March, so they do not consider the recent increase in the 10-year T-Bond yield.

TradingView

Unrealized losses in Q2 2024 are likely to be higher, and a loss greater than $30 million regarding the securities portfolio reallocation plan cannot be ruled out.

Conclusion

Over the past year, NWBI has experienced significant deterioration due to a sharp increase in interest expenses. Customers gradually shifted to alternatives that could better remunerate their savings, including time deposits. The latter negatively impacted profitability as the increase in loan yield was not enough to keep the net interest margin stable.

Unrealized losses are a factor not to be overlooked and likely to worsen in the next quarter. Management is intent on selling high duration and low yielding securities at a loss, but this will result in realized losses in the income statement. The dividend is sustainable as long as earnings do not worsen too much, which is not a given considering the current macroeconomic environment.

In my previous article the rating was a hold, but following the deterioration in profitability, combined with the increasingly concrete scenario of higher for longer rates, I think a sell is more appropriate at this time.

Read the full article here