")

Murphy Oil (NYSE:MUR) generally keeps a conservative balance sheet while operating offshore. As an offshore operator, this company is one of the smaller offshore operators. This latest article will focus (in contrast to the last article) on the latest changes due to lower debt levels and new projects. The projects offshore tend to be large and so risk management is a big deal. A significant number of offshore operations also means that management will report “lumpy” growth rather than smooth growth because production increases tend to take years to happen, and those increases tend to be large when they do happen.

During the conference call, it was mentioned that the cash flow for the market cap should be number 1 for at least the time being. Murphy has some very profitable projects. Even considering that, offshore projects tend to cash flow at low prices due the large upfront fixed costs. Therefore, cash flow will be generous under a wide variety of industry scenarios.

Stock Price Discount

Questions also surfaced during the conference call about the stock price discount. In reply, management’s answer is to repurchase as much stock as possible. That will provide some downside protection to the stock price.

Now, production can vary by quarter as reworks and maintenance downtimes tend to involve relatively significant amounts of production due to the relative size of the offshore projects.

All of this overshadows the quarterly results (which are generally excellent). This part of the industry is seen as unpredictable. Murphy does have onshore production. But much of that production will generally provide cash for the offshore area of the company because that area can be very profitable.

So, the steadiness and predictability of unconventional onshore production appears to be more reassuring than the variations inherent in the more profitable offshore production when valuing this stock. Management believes that will change over time.

Profitability and Cash Flow

Profits dropped from the previous quarter largely due to noncash charges. Those charges include the write-off of an unsuccessful offshore well and an impairment charge. While these charges are generally considered nonrecurring, they do affect the ability of analysts to predict the future. A company that engages in relatively large projects will have significant unsuccessful well write-offs from time to time and those offshore wells are expensive. The same goes for impairment charges.

Cash flow actually advanced considerably over the previous fiscal year because those two charges were noncash. Those charges instead shielded cash flow from taxation due to other profitable activities. There is also a change in accounts that favorably impacted the GAAP cash flow from operating activities in the comparison.

Usually, the changes in noncash working capital accounts will even out over time. Therefore, there could be a negative cash flow effect in the future that reverse the current quarterly favorable comparison.

Growth Plans

Several conference call questions centered around the expansion of cash flow available for dividends and buybacks because the company only has $300 million of debt to repay before shareholders will receive 50% in benefits once that debt is repaid rather than the current 25%.

This model is a little different from many of the other companies I follow as Murphy has some potential “homerun” projects (sort of like what Guyana is to Hess (HES)). Murphy has hit a lot of “singles and doubles” since I began coverage. So, a “homerun” or elephant discovery is not out of the question.

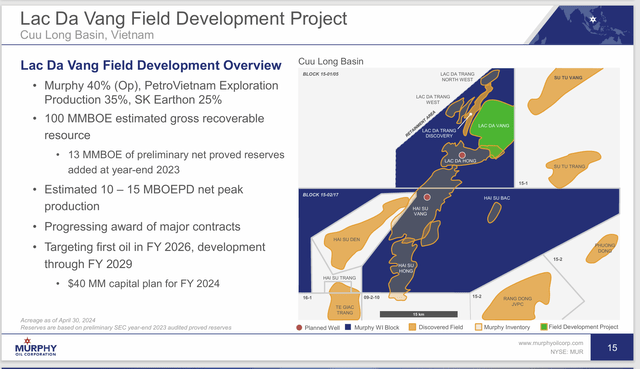

Vietnam

Probably the first project to consider is the Vietnam offshore business that is now proceeding to production. The company will also be drilling two exploration wells.

Murphy Oil Summary Of Vietnam Lease Possibilities And Development (Murphy Oil First Quarter 2024, Earnings Conference Call Slides)

Management has a long stalled offshore project moving again as shown above. The exploration wells provide considerable upside potential (as well as significant write-off risk if not successful).

This management has long managed offshore risk in an excellent fashion. The result of this is a long history of upside potential projects combined with write-offs (like the current quarter) that are easily handled by the company.

Mr. Market, of course, hates the unpredictability of quarterly write-offs. But loves the upside potential that large offshore projects bring to the table.

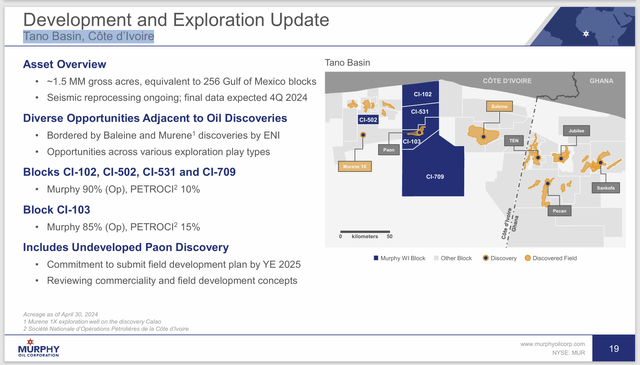

Tano Basin, Côte d’Ivoire

The acreage awarded here is equal to roughly 152 Gulf Of Mexico acres. Of course, the price was far cheaper than was the case with Gulf Of Mexico acreage. Right away that will lower the costs materially of any oil produced because the location costs of the wells drilled is lower for any potential successes. Likewise, failures will not hurt as much.

Murphy Oil Summary Of What Was Known As The Ivory Coast Projects (Murphy Oil First Quarter 2024, Earnings Conference Call Slides)

The sheer amount of acreage awarded to the company automatically makes this a large project. Typically, management will limit the risk by gaining partners until the percentage of the participation is in a range management feels is acceptable. It is not unusual in a situation like this for management to retain a small percentage of participation in a project like this, with larger percentages as the oil deposits become “known” so that future exploration wells carry less risk.

Already there is an advantage for an exploration well in that one of the blocks is “bookended” by discoveries on either side.

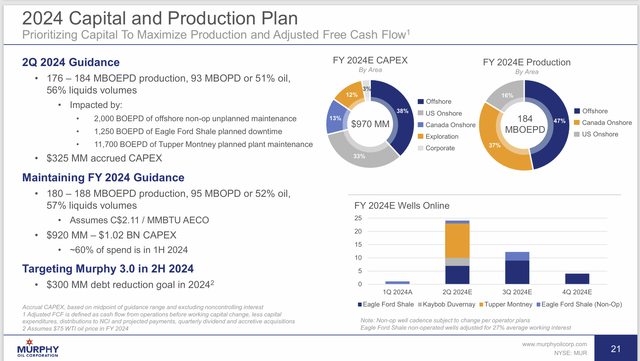

Guidance

The one thing that continually enters into the company valuation is that first part of the next slide where volume impacts are discussed. Even though the largest impact is onshore this time. The offshore business makes those impacts overall much more frequent than is the case with typical onshore unconventional companies.

Murphy Oil Second Quarter 2024 Guidance (Murphy Oil First Quarter 2024, Earnings Conference Call Slides)

Similarly, there is always an exploration or development well that can result in a quarterly write-off.

These “quirks” of this part of the business seem to overshadow that the cash flow is very generous as offshore projects require a lot of upfront cash. Those same projects then provide a very generous depreciation that results in a lot of cash flow compared to the unconventional companies.

But Mr. Market has long not liked unpredictable once and done quarterly occurrence that constantly recur with different projects. There is no easy answer to that dislike even though this management handles the risks well enough that the company is actually very profitable over time.

Summary

The strategy of the company is gradually changing from primarily debt repayment to a combination of shareholder returns and more exploration. This company is getting to the end of the debt market enforced “better debt ratios” even though those ratios were conservative to start with while heading towards a more growth-oriented future as well.

This is a change in strategy from the strategy primarily in place since 2020. Once the debt total falls to $1 billion or less (and that will be shortly), then 50% of excess free cash flow will be available to shareholders.

This management mentioned during the conference call that they would just love to buy back a lot of stock at that point because they view the stock price as a bargain.

However, several projects could demand more cash and many typical cash uses are included in the calculation before you get to excess free cash flow. That means that this company is likely to remain a growth story with a lot of “homerun” opportunities while continuing a steady parade of “singles and doubles”. The dividend is likely to increase in the future with less debt to service. But a major discovery could easily shift priorities.

The unusual nature of the company with that material offshore business for a relatively small player (and a successful one at that) makes it hard for the market to value. But the bright future possibilities make this a speculative strong buy with the idea that this company is more likely to find an elephant than most. It would be a strong buy for those that like slow growth and a likely increasing dividend.

Risks

Offshore exploration and development has got to be the riskiest and most expensive proposition of any part of the upstream business that I follow. There probably cannot be an adept management at handling those risks than this management. But that could change at any time. Expenses would then quickly balloon out of control.

Any upstream company is subject to the volatility and low visibility of commodity prices.

The part of Africa where the company is choosing to do business is known for its instability. Usually, the offshore business is somewhat immune to the onshore situation. Generally, whoever runs the government is supportive of the industry because it brings in badly needed foreign currency. But the instability is an inherent risk factor because things can quickly change.

Any company is at risk to suffering from the loss of key personnel.

Read the full article here