")

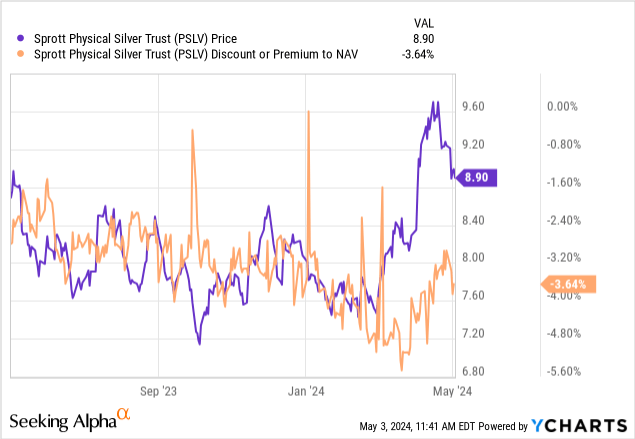

It has now been over a year since I last covered the Sprott Physical Silver Trust (NYSEARCA:PSLV) for Seeking Alpha. In my last piece, I said it was “time to buy the dip” and the timing of that call was quite good. At the time the article was published, PSLV shares were just over $7 and within a few weeks PSLV ripped up near $9. Following that rip, PSLV chopped around a bit for several months but we have since broken out of that range.

Today, we find PSLV again near $9 per share but this time $9 is potential support rather than resistance. In this update, I’ll get into why I think this is another dip to buy for PSLV bulls.

Technical Case for PSLV

While it’s probably not as useful long term as a clear fundamental setup, I think technical analysis is a great way to assess sentiment in the market at a given time.

Silver Weekly Chart (TradingView)

Looking at the weekly chart of Silver (XAGUSD:CUR), I’m seeing a clean 20 year uptrend with large spikes during times of central bank intervention. We see a parabolic rise in response to GFC and 150% rip in response to COVID-era stimulus.

Silver Weekly Chart (TradingView)

Zooming in at the weekly provides some additional insight into the shorter term action. More recently, Silver has broken out over resistance at $26 and is now back-testing that zone to establish support. Given the strength in metals broadly, I expect this area to hold before the metal makes another attempt at $30. And again, this is just a technical opinion. I think the fundamental case for Silver is actually quite strong.

Fundamental Case for PSLV

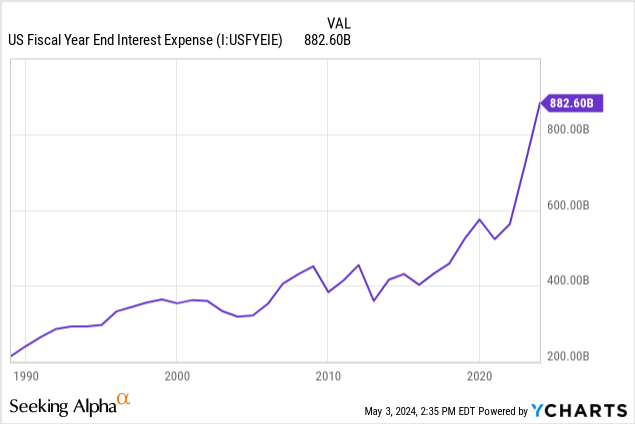

I’ve made several fundamental arguments for precious metals through the years. Those have generally included but not been limited to fiat currency debasement and the BRICS nations challenging dollar hegemony. Admittedly, the latter has not played out in a meaningful way to this point. Regardless, there is still a totally justifiable case for metals due to the predicament the US fiscal/monetary system is currently in.

Interest payments on US debt are rising and if the Federal Reserve keeps rates higher for longer, that debt is only going to continue to get more expensive. Recent history tells us that this debt will be monetized by the central bank since raising taxes is politically impossible, particularly in an election year. Just as Gold (XAUUSD:CUR) and Silver rallied in response to COVID stimulus, they will likely rally again with what I expect to be more debt monetization. And this is just taking the view that XAG serves as monetary debasement insurance and nothing more.

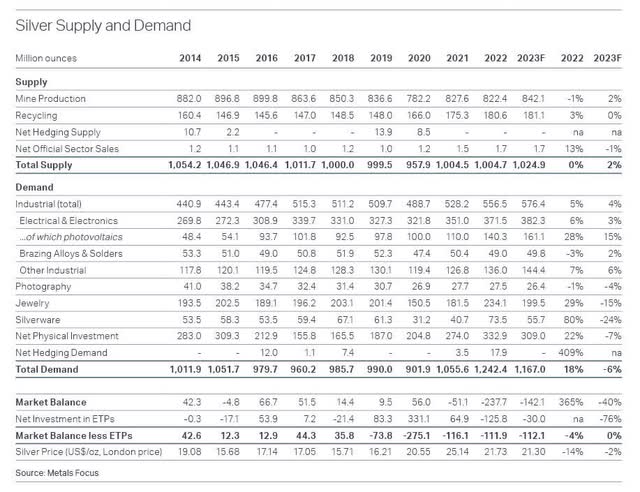

Supply/Demand Balance (Silver Institute)

To a larger degree than Gold, Silver is used as an industrial commodity. And what we can see in the table above is 3 consecutive years of imbalance between supply and demand. Adjusting those metrics for ETP products and the imbalance is actually 5 years running. The point is, the world needs more silver and there isn’t enough being mined or recycled at current levels. Even without the currency debasement argument, the price of Silver will rerate higher if this supply/demand dynamic continues.

Risks And Additional Considerations

In my personal opinion, there is no substitute for holding the metal in your own hand. Whether that be through rounds, bars, coinage, or jewelry, I do think it’s wise to own at least some physical metal. Longing PSLV in a retirement account is certainly not the same thing as holding the physical metal in your hand. But buying Silver through PSLV allows an investor three distinct advantages over holding the metal directly.

- Security: buying vaulted Silver is theoretically safer than trying to store a large amount of physical silver yourself.

- Liquidity: Since the fund shares are traded via the trust wrapper, buying and selling PSLV is fast, easy, and cheap as there are no shipping or handling costs associated with physical bullion delivery.

- NAV Rate: buying the metal via PSLV today is buying metal at a discount rather than a premium.

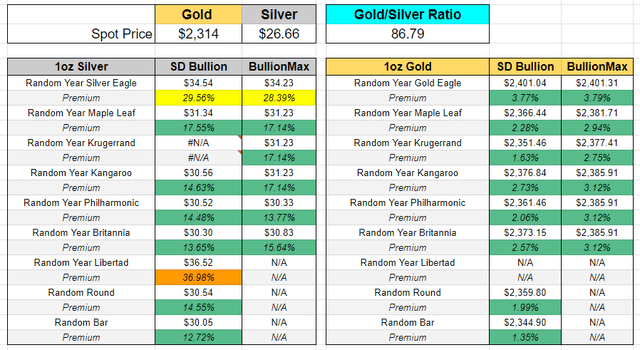

When I covered PSLV in February 2023, the fund was trading at a fairly large 6% discount. That NAV rate is now closer to 4% but it’s still much cheaper to buy Silver through PSLV than to buy it through a physical bullion dealer. Even if we adjust for the fund’s 0.6% expense ratio, the 3% net discount is far superior to the 13-15% premium one will pay when buying random bars or rounds through popular bullion sites:

Bullion premiums as of 5/3/24 (Author’s Calculations)

Naturally, there are tradeoffs. And when one is purchasing metal through trust shares like PSLV they don’t actually have control of the Silver being purchased. Additionally, there are embedded trust assumptions that come with intermediaries including but not limited to asset managers, vault owners, and brokerage account providers.

Closing Thoughts

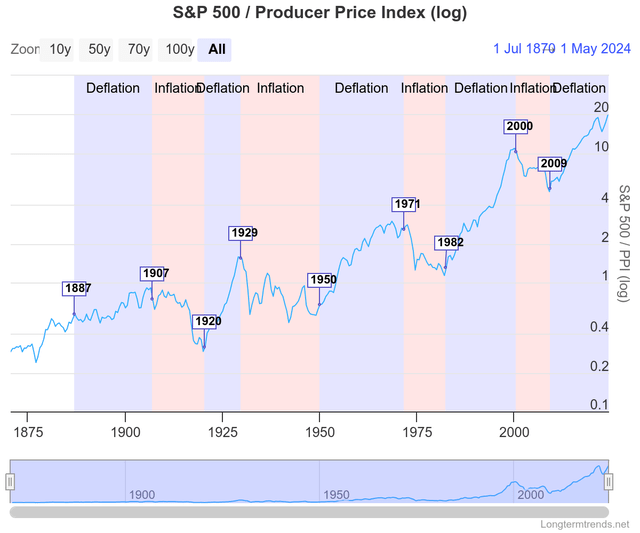

Stocks to Commodities Ratio (Longtermtrends.net)

For an investor who doesn’t want to speculate on equities with a Buffett Indicator at 181% in April and a stocks to commodities ratio at 20, there may only be a few viable options for capital appreciation. I’m certainly not opposed to taking some chances on decentralized currencies or hard assets. I suspect precious metals are going to play a large part in portfolio allocations for the next several years. If one takes the view that commodities are undervalued to stocks and that Silver is undervalued to Gold, PSLV figures to be a nice place to park capital while financial markets experience some mean reversion.

Read the full article here