CPI came in cooler than I expected

This week, much of the focus was on the CPI data for April, which came in a bit lower than estimates. This was something seemingly forecasted by nearly everyone but me. Yes, this is my way of saying I was wrong. I won’t apologize for closing out positions in my trading account and holding mostly cash going into the CPI. I did have some minimal hedging but closing them out was fairly painless, that’s what insurance is for. I am still cautious and holding about 35% cash right now. I intend to maintain that level for the rest of May, which means that If I want to trade, I will have to close out a current trade to enter a new one. I will address that later in this article, I just wanted to get this down on paper because I try to be as real as possible, I called out the possibility that the CPI would be hotter, and it came in cooler. Now let’s push on.

We’ve had economic numbers that were cooler and stocks rallied, except for retail

The Commerce Department’s Census Bureau said on May 15 revealed unchanged reading in retail sales for April following a slightly downward revised 0.6% increase in March, Retail sales were previously reported to have risen 0.7% in March. This data caused a lot of consumer-discretionary stocks to sell off. Now that several days have passed, we can sift through different names and pick out some nice trades. Some stocks have been cast away that are doing quite well. So first I want stocks focused on services, preferably “asset-light” names. Let’s start with travel and entertainment stocks, middle-class consumers and higher are still traveling and going out.

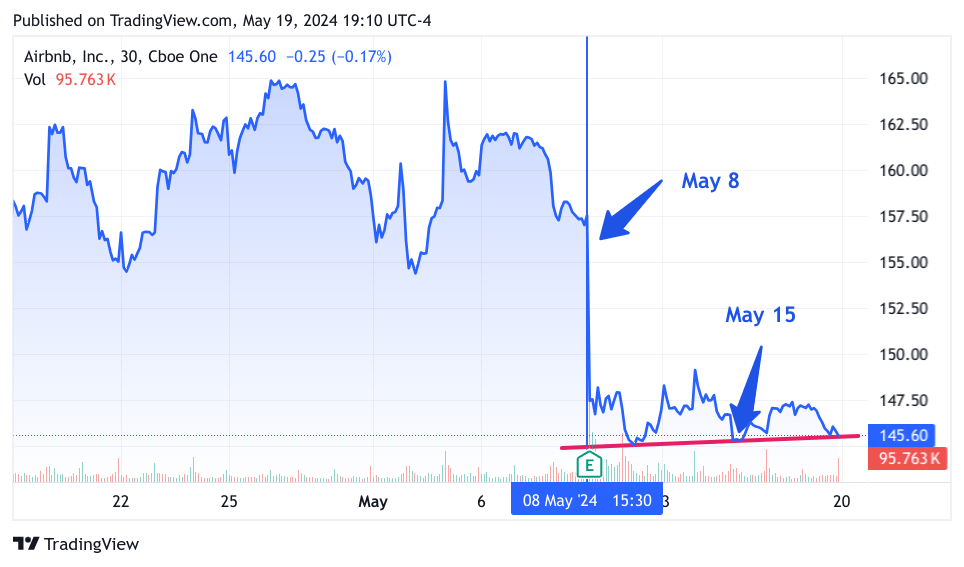

First, let’s re-examine Airbnb (ABNB)

So ABNB reported on May 8 that, by all accounts, they had a fantastic quarter. The stock sold off on weaker guidance for the second quarter. It is common for growth stocks to pull back on guidance so that they under-promise and then over-deliver. The same is happening here. Airbnb’s first-quarter revenue rose 18% year-over-year to $2.14 billion. The company forecast second-quarter revenue between $2.68 billion and $2.74 billion, and analysts’ average estimate was $2.74 billion, due in part to currency exchange rates and the timing of the Easter holiday. Is that as gloomy a forecast as was reported by the media? Earnings were 77% above analyst forecast as well. Let’s now look at the 1-month chart

TradingView

We see the steep decline on May 8 after the earnings report, then we see a bit of a recovery before May 15 when the retail sales numbers were revealed. Even so, we do see higher lows, as illustrated by the red line. I think I see an opportunity to get long ABNB and enjoy a recovery in the stock as market participants look back at the numbers and rethink their discarding of this great name.

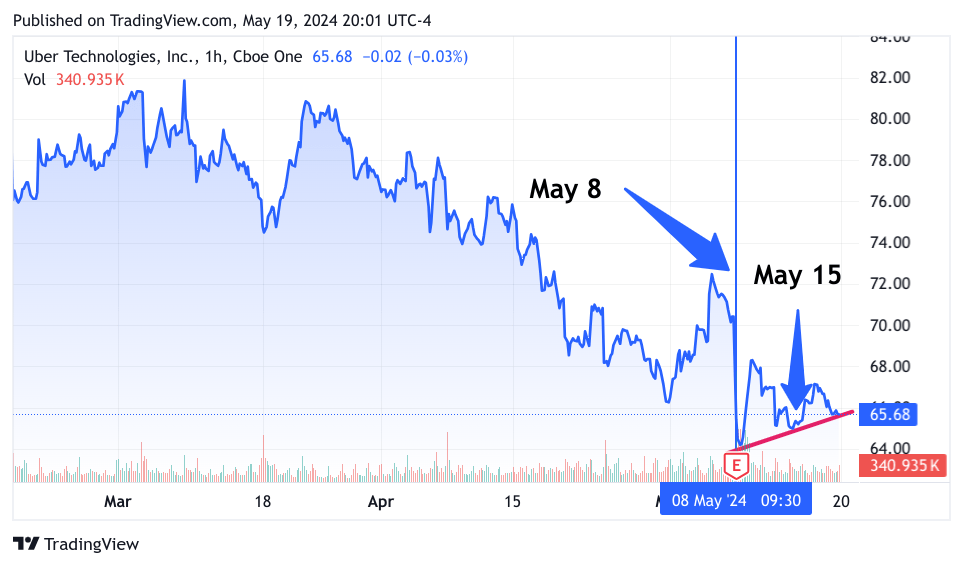

Next Is Uber Technologies (UBER)

UBER also reported on May 8, they had a more complicated earnings picture. I am not surprised that UBER sold off, they wrote off some international investments, along with higher legal fees and gross bookings came in slightly lower. Revenue did grow year-on-year by 15% to $10.10B, though no one wants to see an unexpectedly large loss of $654M, However, UBER is not sitting still, its Uber Eats bought the Taiwanese food delivery business – FoodPanda for $950M, Uber Eats signed up with Costco to deliver product for them. Uber also just announced a new shuttle service to Airports, Concerts, and Stadiums. Also announced that Instacart (CART) will be using Uber Eats to handle restaurant delivery. So I think this is a one-time thing, and in my opinion, UBER can be bought for a trade, expecting a very nice recovery. Let’s look at the 1-month chart.

TradingView

We see a very similar pattern, a sharp sell-off on May 8, and a bounce back before May 15. The red line marks out higher lows, as the stock resumes its recovery. I see this as a nice entry point for investment as well as for a trade.

Last, we have Affirm (AFRM)

AFRM reported a revenue jump of 51% year over year, while AFRM posted a quarterly loss of 41 cents, which represents a positive earnings surprise of 38.57%. Yet AFRM sold off hard and many analysts are pointing to the lower guidance of Shopify (SHOP) and that AFRM sold off in sympathy. SHOP represents only 10% of its GMV – Gross Merchandise Value, so it shouldn’t have a large effect on AFRM’s share price. Charge-offs fell to just 2% in 2024 so far, so the notion that AFRM is having large credit losses is incorrect. Finally, AFRM raised guidance for the current quarter. Let’s look at a 3-month chart.

TradingView

Just like ABNB, and UBER, AFRM also reported on May 8, and just like the prior 2, AFRM took a further dip starting May 15, however, through the week AFRM improved. Perhaps market participants are rethinking their negative picture of AFRM already.

I am already a long-term investor in AFRM and UBER and have some trades on UBER as well. I am going to think about getting back in AFRM for a trade and initiating a position in ABNB for investment.

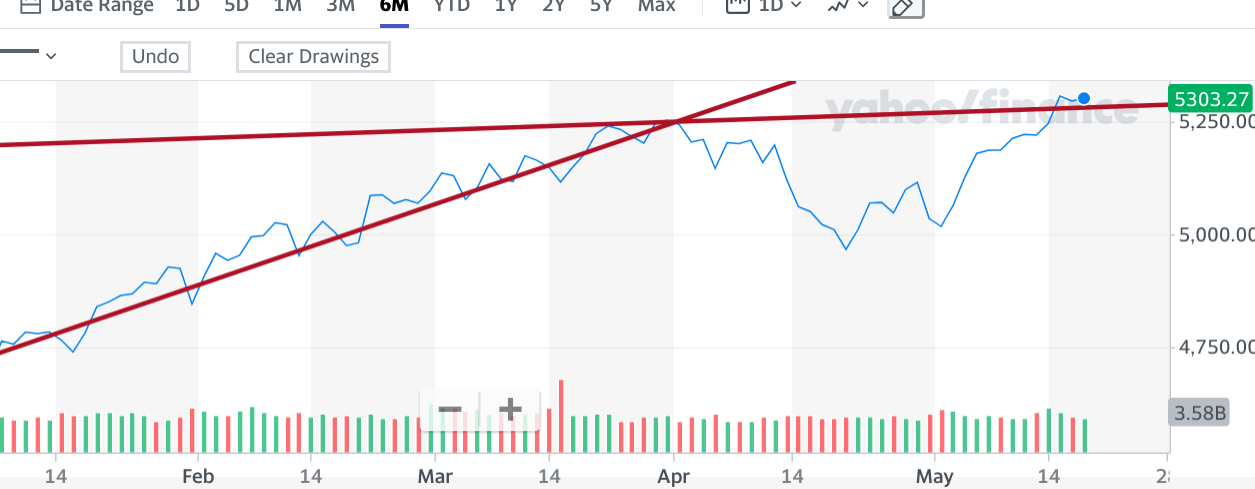

Why am I still cautious?

Now about why I am still cautious about the market, look at this chart that I shared with my investment group. This is a 6-month chart of the SPX index – the S&P 500. I just wanted to illustrate to them how it is trading. This chart comes courtesy of Yahoo Finance.

Yahoo Finance

TradingView

This is a very simple chart. The steepest diagonal is the rally at a very strong upward movement. The second almost flat line shows that the prior peak leading to the current one is barely moving upward. I am concerned that this could be a false breakout. It’s that simple, so for the time being I will hold a chunk of cash in reserve and see if we get another dip.

And with that hopeful conclusion, I wish you all the best of luck.

Read the full article here