Introduction and Background

I am a high-quality dividend growth investor first, but have a strong lean toward value, as anyone who has read my previous articles knows. For many months now, it has been difficult to find high-quality, dividend-growth stocks trading at a deep discount.

With that in mind, instead of my normal, high-quality trading near 52-week lows focus, I thought I’d dig a little deeper into the growth part of high-quality dividend growth to see if there are any obvious opportunities that might not be deep value plays, but that still offer strong investment potential longer-term. Maybe we’ll uncover some value along the way as well.

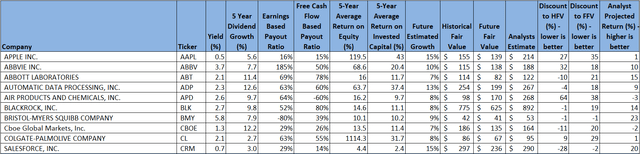

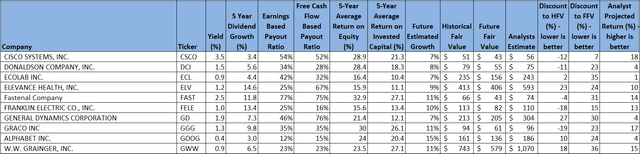

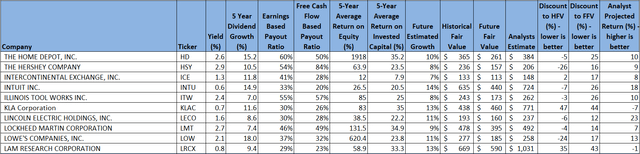

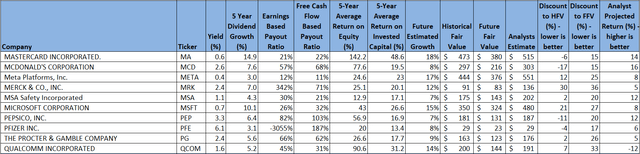

I regularly track around 100 high-quality dividend growth stocks. Let’s take a look at a subset of those where I’ve recently updated valuations:

FinBox, Seeking Alpha, Author’s Analysis FinBox, Seeking Alpha, Author’s Analysis FinBox, Seeking Alpha, Author’s Analysis FinBox, Seeking Alpha, Author’s Analysis FinBox, Seeking Alpha, Author’s Analysis

First, Fair Value Estimation

Though I promised I’d be focusing more on growth this time, I know you’ll be disappointed if we completely ignore valuation, and I know many of you like to see the standard valuation chart that I include in my articles.

For valuation, I like to calculate a fair value in two ways, using a Historical fair value estimation, and a Future fair value estimation. The Historical Fair Value is simply based on historical valuations. I compare the 5-year average: dividend yield, P/E ratio, Schiller P/E ratio, P/Book, and P/FCF to the current values and calculate a composite value based on the historical averages. This gives an estimate of the value assuming the stock continues to perform as it has historically. I also want to understand how the stock is likely to perform in the future so utilize the FinBox fair value calculated from their modeling, a Cap10 valuation model, an FCF Payback Time valuation model, and a 10-year earnings rate of return valuation model to determine a composite Future Fair Value estimate.

I also gather a composite target price from multiple analysts including Reuters, Morningstar, Value Line, FinBox, Morgan Stanley, and Argus. I like to see how the current price compares to analyst estimates as another data point, and as a sanity check to my own estimates.

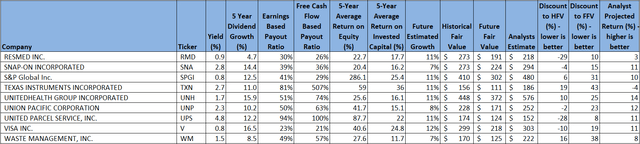

Plotting three variables on one plot is tricky but using a bubble plot allows us to visualize three variables by plotting the Historical fair value versus the Future Fair Value on a standard x-y chart, and then use bubbles to represent the size of discount relative to analyst estimates.

Author calculation of Historical and Future Fair Value, analyst estimates

This chart is insightful once you understand how to interpret it. What we are looking for are stocks that are trading at a discount to both the Historical Fair Value and the Future Fair Value. So, those stocks that are farther to the left, and farther to the bottom, are potentially the stocks trading at the largest discount to fair value. This would be the bottom left quadrant of the graph. Additionally, those stocks with the biggest bubbles are the stocks that are trading at the largest discount to analyst estimates, so in theory, stocks in the lower left quadrant that also have large bubbles should be decent candidates for investment.

The chart suggests that both Salesforce, Inc. (CRM) and Bristol Myers Squibb Company (BMY) appear to be very attractive from a Historical Fair Value and Future Fair Value perspective, as well as having potential based on analyst estimates.

I own both of these stocks. I recently initiated a starting position in Salesforce at $214 after the big earnings decline, and have continued to average down with Bristol Myers Squibb, feeling the pain of that dropping knife all the way down. I plan to add more under $40.

Additionally, since my last article, I also started a new position in McDonald’s Corporation (MCD) at $251 and added to my position in United Parcel Service, Inc. (UPS) at $134.

Now, how about that Growth?

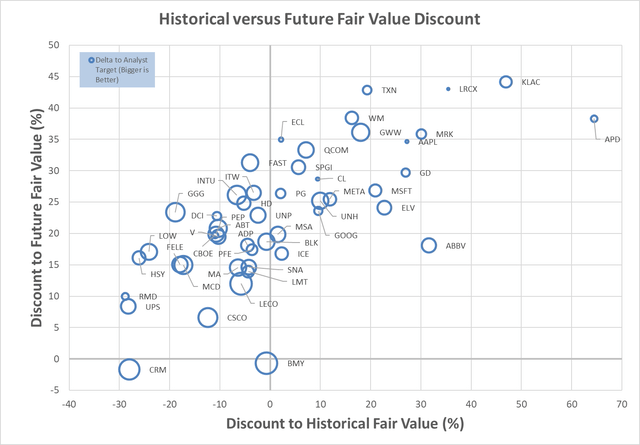

So now that we’ve spent some time looking at valuations, as promised, let’s take a look at growth. Another way I really like to look at my watchlist is by plotting the past 5-year dividend growth versus my projected forward growth, while also considering yield.

I’ll be the first to admit that growth is the hardest part for me to predict in investing. I use a combination of factors and models to derive a composite growth estimate, both past and future looking. This includes past EBITDA growth and forecasts, past dividend growth, recent changes in shares outstanding, several long-term earnings growth forecasts, a forward rate of return model, and Return on Invested Capital compared to the Weighted Average Cost of Capital.

This is what the plot looks like:

Author calculation of Projected Growth, FinBox

With this chart, we want to see those stocks with the biggest bubbles that are farthest to the top and right.

Now we’re having some fun. We can obviously look for just those that are top and right, like Mastercard Incorporated (MA), Intuit Inc. (INTU), and Visa Inc. (V). We can obviously also look at those with the biggest bubbles, like Pfizer Inc. (PFE), and Bristol Myers Squibb Company (BMY). Looking for the combination of all three is where the real potential could exist – high growth, which supports further high dividend growth, all wrapped up nicely in a decent current yield. Companies like United Parcel Service, Inc. (UPS), The Home Depot, Inc. (HD), and Automatic Data Processing, Inc. (ADP) are examples that could fall into this camp.

So to have some fun, and just mix things up a little compared to my normal articles, let’s take a company that is potentially attractively valued, that also appears to score well in this growth view, and compare it to a company that doesn’t appear to be as attractively valued, but still looks attractive in this growth view to see if we can make any conclusions regarding where to invest. I will be comparing United Parcel Service to Home Depot.

I own both of these and plan to continue investing in both. They are both very high-quality companies. The question I want to consider is am I paying too much attention to valuation? Should I just put my money to work in the highest quality, highest growth companies, and quit paying so much attention, and investing so much time into valuation?

Preliminary Analysis

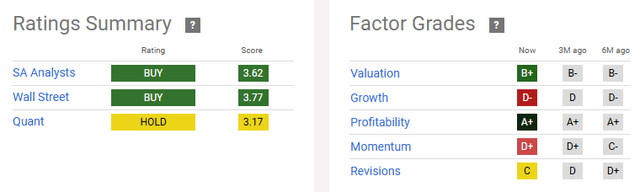

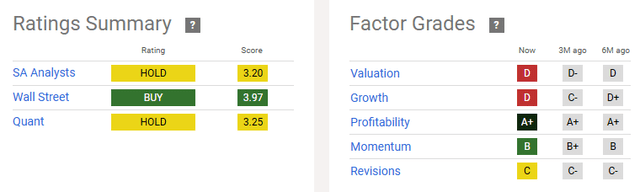

Seeking Alpha makes available a summary of ratings, as well as factor grades. These make for another nice, first-pass filter for investment timing.

United Parcel Service:

Seeking Alpha

Home Depot:

Seeking Alpha

Well, I think we know what the lean of most analysts is – valuation. The comparison highlights that UPS is likely attractive based on valuation and analyst consensus. HD on the other hand, is not as attractively valued, and analysts don’t appear to be as excited.

Since we’re focusing on growth for this article, it’s interesting to see that the factor grades show both poor growth factors.

Comparative Growth Analysis

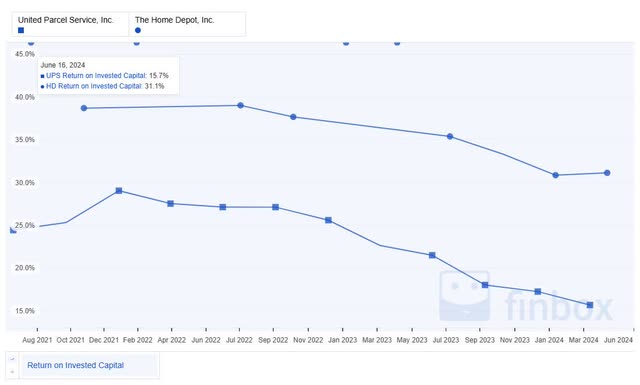

One of my favorite metrics to start with is Return on Invested Capital. I like to look at companies that have high ROICs since this should help feed continued growth.

FinBox

Both UPS and HD have high ROICs, with a strong history of those high ROICs. Both companies have experienced some erosion in their ROICs. HD looks more attractive in this regard and shows more margin to sustain ROIC above the Weighted Average Cost of Capital. The delta between ROIC and WACC is one of the indicators that I look at from a growth perspective, the idea being that excess returns above WACC can be used to fund growth or to sustain the dividend.

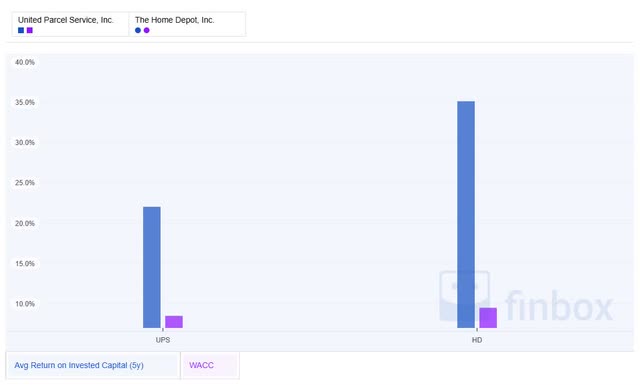

FinBox

Based on a comparison of the 5-year average ROIC to the current WACC, both companies appear favorable, with HD being more attractive.

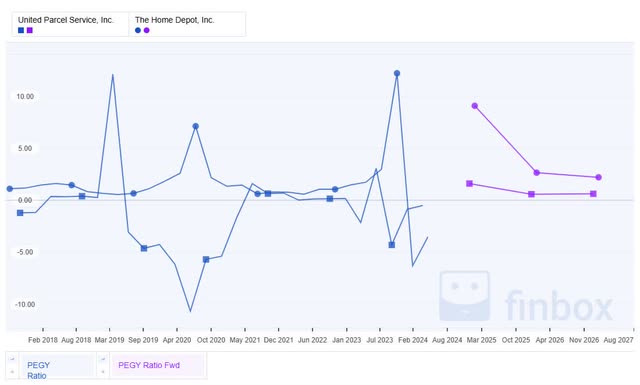

Though we’re focusing more on growth than valuation for this exercise, I still like to consider the price you’re paying for that potential growth. To do this, let’s look at the past and projected PEGY ratios. For those less familiar, PEGY is a version of the well-known Price-to-Earnings Growth ratio, with yield added into the mix, essentially including yield in the total return calculus.

FinBox

Both stocks have negative current PEGY ratios based on recent negative earnings growth. Looking to the future though, based on current valuations, UPS is projected to trade at a lower PEGY ratio, giving UPS an advantage in this comparison.

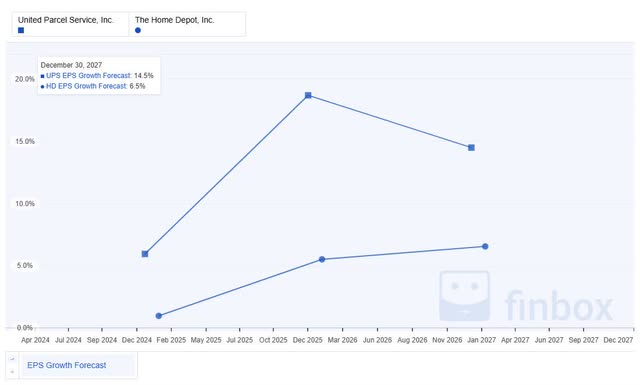

Let’s look at what that future earnings growth might look like. To do this, we’ll start with a history of analyst estimates for this growth – I like to see how different the history is to the future.

FinBox

Maybe not a big surprise, given current valuations, but HD has higher recent growth expectations than UPS, showing recent estimates to be about 2 percentage points higher than UPS. Historically, the companies have been in similar ranges of growth, suggesting the comparison between them is not completely ridiculous.

What about future estimates?

FinBox

Looking to the future, HD looks more attractive than UPS from an earnings growth perspective. The reason I like to look at historical estimates for growth, as part of the look to the future, is to look for discontinuities. HD’s future estimates are more in line with historical estimates, whereas, UPS looks like the forward growth is well below where it has historically been estimated to be. Sometimes this is an indicator of company decline. Other times, this can just be an indicator that a company is out of favor, which could be a good time to buy.

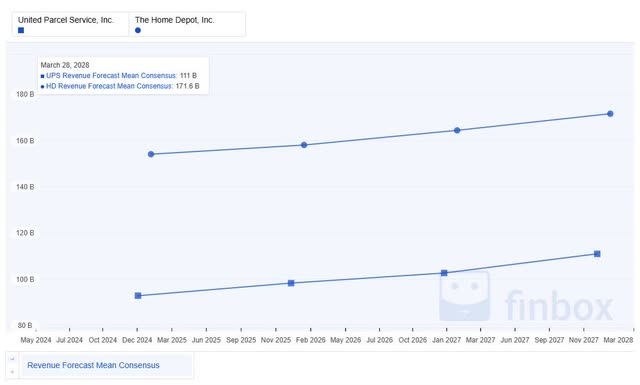

From a revenue projections perspective, both companies show solid signs of continued growth, so the key question that remains to be seen is can that growth in revenue to turn into profit, which would therefore suggest that the lower earnings growth is likely just an issue with short-term favor.

FinBox

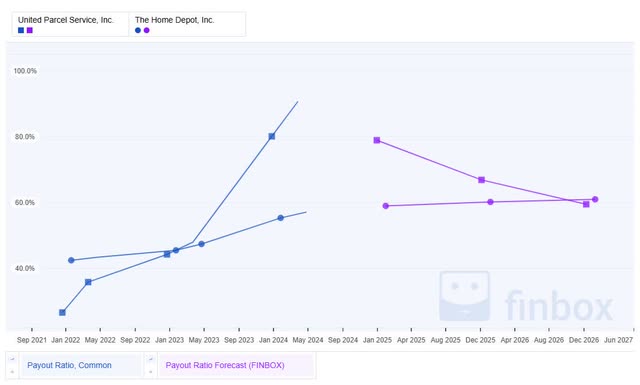

In talking about growth, as a dividend growth investor, one of the most important growth components I’m concerned with is the ability of the company to continue to grow over time. Payout ratios are an important indicator of this growth potential.

FinBox

HD looks more attractive from a past and future payout ratio perspective than UPS. As a matter of fact, the most recent payout ratio for UPS is concerning, approaching 100% of earnings. This obviously does not lend itself to high, sustainable future dividend growth. Looking forward though, the payout ratios do come down significantly for UPS. It’s also worth noting that HD generally has nice stable payout ratios over time, which is a good attribute for a dividend-paying stock. If the projections for UPS are true, this could be a nice time to buy.

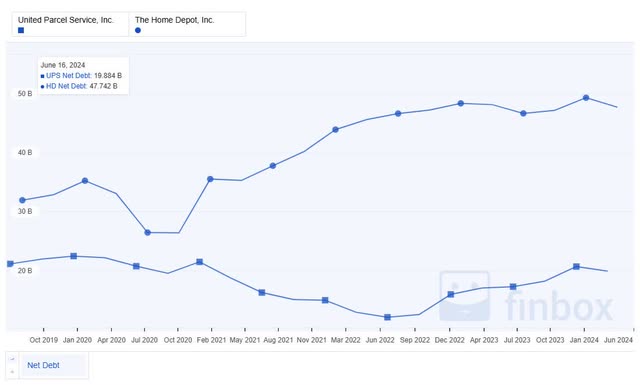

Looking at future sustainability, especially with the high payout ratios that UPS currently has, I also like to look at the net debt position. These aren’t directly comparable, since the companies are different sizes. What we’re more looking for here is the stability over time, and evidence that management may be increasing debt to sustain the company, or to sustain the dividend.

FinBox

If anything, HD is the one that has increased net debt over time, as the business has grown. UPS has had a fairly stable net debt position, and at least at this point, does not appear to be increasing debt at the expense of the business sustainability.

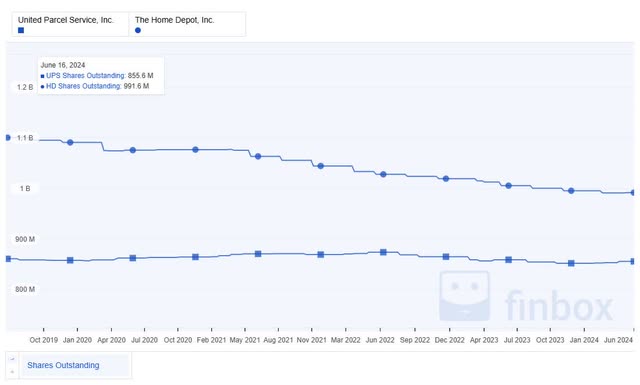

In addition to debt, equity is another consideration for a shareholder. A company can obviously finance its operations and shareholder returns using many strategies. Ensuring that a company is not increasing shares outstanding by issuing equity is another attribute I look for.

FinBox

In this case, HD has had a strong history of decreasing shares outstanding. UPS, on the other hand, has more or less held shares consistently. Obviously, decreasing shares helps to improve the sustainability of future dividend growth, but at least we don’t see UPS using equity to support the business short term.

Risks

Let’s just touch on a couple of components of risk for these companies. These are both very strong, high-quality companies, with what look like reasonable growth prospects, and perhaps most importantly to me, the potential to sustain their dividends, and even grow them going forward.

They are both companies that face a lot of competition and that have interest rate and inflation sensitivity. Both companies regularly face the threat of disruption to their businesses to some degree.

UPS is A rated by S&P, A2 by Moody’s, and A+ rated by Value Line. HD is A rated by S&P, A2 by Moody’s, and A++ by Value line.

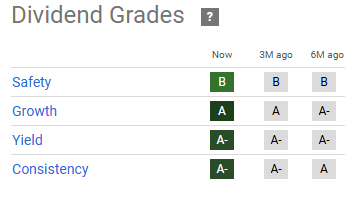

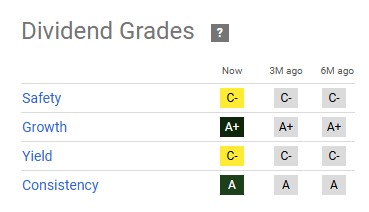

Looking at the Seeking Alpha Dividend Grades:

UPS:

Seeking Alpha

Home Depot:

Seeking Alpha

Both companies have favorable dividend grades, with UPS having potentially a slightly higher level of safety, which is interesting given what we saw with the payout ratios.

Summary

I decided to take a little different approach to my normal article this time. Instead of a pure focus on valuation, I wanted to see if more focus on growth would perhaps highlight opportunities that I wasn’t seeing. Admittedly, the fact that one of the three valuations that I use, the Future Fair Value, contains a lot of future-looking growth, means I don’t ignore growth as part of my valuation, but nonetheless, I find it helpful at times to think about investing from different perspectives, and using different approaches.

So, after all of that, what do I think? I believe that United Parcel Service and Home Depot both continue to be excellent investment candidates. For me personally, I will likely continue to rely heavily on valuation as part of my approach, while including growth as part of the valuation process.

With that, I believe UPS is attractively valued currently, and, as I said, has recently added to the position that I’ve held since 2018. I also believe that HD has excellent continued sustainable growth characteristics but will likely wait for the valuation to come closer to fair value before I add to my holdings.

Based on the initial analysis in the article, I also believe that both Salesforce and Bristol Myers Squibb appear to be very attractive from a Historical Fair Value and Future Fair Value perspective, as well as having potential based on analyst estimates.

As a bonus question, many of you might have noticed that I had Salesforce, Alphabet, and Meta at the bottom of my growth chart, showing a 5-year average of 3% for dividend growth. Obviously, since they just started paying dividends, there is no such thing as a 5-year average. For now, I’ve put in an arbitrary 3%. What do you do? Do you use an arbitrary estimate, or do you have a better approach? I’ve thought about just using my generic estimated growth rate as a surrogate but am still thinking about it. Also, what about the average historical yield, for companies without a yield history, any ideas?

Read the full article here