")

The Manitowoc Company, Inc. (NYSE:MTW) is a leading provider of cranes and boom trucks which are used for construction, maintenance, deconstruction, salvage, and other applications. This company sells cranes under a variety of brands including Manitowoc, Potain, National Crane, Grove, and Shuttlelift. These cranes are used by many different industries and this company is one of the largest crane providers in the world. With this stock down by about 35% from the highs in February, I wanted to take a closer look.

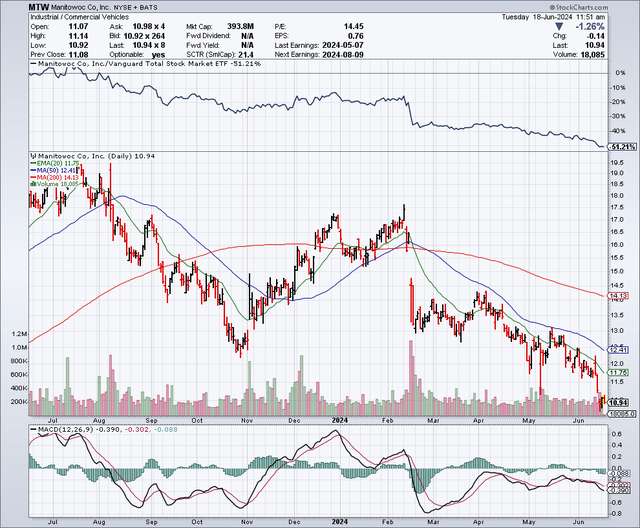

The Chart

As shown below, Manitowoc shares were trading for more than $17 in February, but have since declined significantly to around $11. The stock is now trading well below the 50-day moving average of $12.46 as well as the 200-day moving average which is $14.16. I don’t see a company-specific reason that would justify a pullback of this size, so I think much of it is due to concerns about a slowing economy. Even with these concerns which I share, this stock looks undervalued and the recent pullback does not appear to be justified to me, unless we are going into a recession.

StockCharts.com

Earnings Estimates And The Balance Sheet

Analysts expect Manitowoc to earn $1.18 per share in 2024, $1.39 per share in 2025 (which represents about a 17% increase in earnings), and $1.52 per share in 2026 (which represents a nearly 10% increase in earnings). This represents a solid growth rate and what impresses me is that the stock is trading for just around 9x estimates for 2024, and only 7x earnings estimate for 2026. That represents significant value, especially in a market that is trading for well over 20x earnings.

Manitowoc is expected to report Q2 2024 earnings on Tuesday, August 6. The consensus estimate calls for a profit of $0.56 per share, on revenues of about $610 million.

As for the balance sheet, I am not as impressed, since the company has nearly $462 million in debt and around $31.5 million in cash. I generally prefer to invest in companies with strong balance sheets, but I can also see some benefits and upside potential when the use of leverage is done properly. This company has carried a higher debt load than I would typically like to see, however, it has shown it can manage this and the stock has traded at much higher levels in the past in spite of the debt. Because of this, I am less negative about the balance sheet than I would be otherwise. Another factor that makes me more positive about the balance sheet is the fact that some insiders have a meaningful stake in this company.

Here Are The Upside Catalysts I See For Manitowoc

Recent insider buying and strong insider ownership appear to support a bullish upside scenario. Insiders (especially the CEO and CFO) tend to know a company and the industry it operates in better than most of us. For this reason, I always view recent insider buying as a strong positive, as well as when I see insiders owning a meaningful stake in the company they work for.

On June 4, 2024, Aaron Ravenscroft (the CEO) purchased 1,000 shares at $11.96 per share. He also purchased 1,000 shares in May 2024, at an even higher price. While these purchases do not represent a large amount of money, I still view this as a positive (and certainly better than seeing insider selling). There are other reasons that make me view these relatively small purchases in a positive way and one of them is because there are other insider buyers who have also been taking advantage of the stock decline. Brian Regan (the CFO), bought 1,000 shares in May and he now holds around 108,286 shares, which is worth well over $1 million. The other bullish factor is due to the amount the CEO owns, since his stake is now almost 495,000 shares which even at the very low share price still represents around $5.5 million.

Secondly, in the Q1 2024 earnings call transcript, there are some very positive factors to consider. One is that this company (as of the end of the first quarter), has a backlog which totals about $971 million. That’s a very significant number, especially since it represents an amount that is equivalent to nearly half a year’s worth of revenues. Management also stated that in the U.S., crane activity throughout the country remains strong. I also saw some more encouraging bits of information which suggested that the boom in data centers, chip manufacturing plants, and other infrastructure projects were helping to create demand for cranes, and are therefore likely to be a long-term growth driver. In the transcript, CEO Aaron Ravenscroft stated:

“With this in perspective, I recently spent a day with the owner of a large crane rental house who’s been in the business for more than 50 years, and he told me that he’s seeing more work coming than he’s ever seen. Of course, we all see the announcements around the semiconductor projects, but this fellow indicated that data-storage centers, rail, and power generation were driving his regional market.

It will be interesting to see how this plays into decision-making over the next couple of quarters, but I view the medium and long-term outlook in the US favorably.”

A third possible catalyst comes from the European Central Bank or “ECB” recently cutting rates for the first time in years and this could be the start of a rate cutting cycle. This could spur new home construction and industrial development in Europe. The Federal Reserve is also expected to cut rates later this year, and the Fed has projected these cuts could continue into 2026. This could drive more economic activity in the coming years which would benefit Manitowoc.

Lastly, the U.S. and many other parts of the world need to rebuild infrastructure. Many bridges, rail stations, airports, and power stations, are in need of rebuilding and this is a growth driver for Manitowoc.

What I Don’t Like About Manitowoc (Potential Downside Risks)

In that same earnings call transcript, the CEO said the tower crane market in Europe remains “very challenging”. However, the Committee for European Construction Equipment recently released their annual report which suggested that the European construction market will stabilize in 2024 and start to recover next year, thanks to investments in renewable energy and infrastructure.

Of course, there are macro concerns that could be a potential downside risk for this stock. This includes a stock market correction, but I would say especially if that correction is caused by a recession. A U.S. or global recession would likely impact a crane company in a significant way. I believe this stock would go down further, if we even just had a “growth scare” rather than a full-blown recession. This is an economically sensitive stock and I know from past experiences that these types of stock can be hit hard, even more than what is sensible. So, along with the fact that I am concerned the Federal Reserve has already waited too long to cut rates, I have to temper my enthusiasm. I recently wrote an article detailing my concerns about Fed rate cuts and a potential recession, so even though I am putting a buy rating on this stock, I would only buy a small position for now.

In Summary

I see a number of positives including a very low price-to-earnings ratio. It is great to see recent insider buying and a meaningful stake being owned by management. The backlog of $971 million is another big positive. It appears that this company will benefit from the boom in AI data centers, semiconductor facilities and infrastructure as well. Because of the balance sheet, and because I believe the risks of a recession are quite high now, I won’t buy a lot of this stock. I just bought a small position as a way to keep a closer eye on it. If there is a recession, the opportunity to buy will likely be much greater, so I am holding back for now, but I do see significant long-term upside potential once we get past a possible growth scare or recession.

No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.

Read the full article here