| Seeking Alpha")

Written by Nick Ackerman, co-produced by Stanford Chemist.

Since our prior coverage, Adams Diversified Equity Fund (NYSE:ADX) has performed incredibly well.

ADX Performance Since Prior Update (Seeking Alpha)

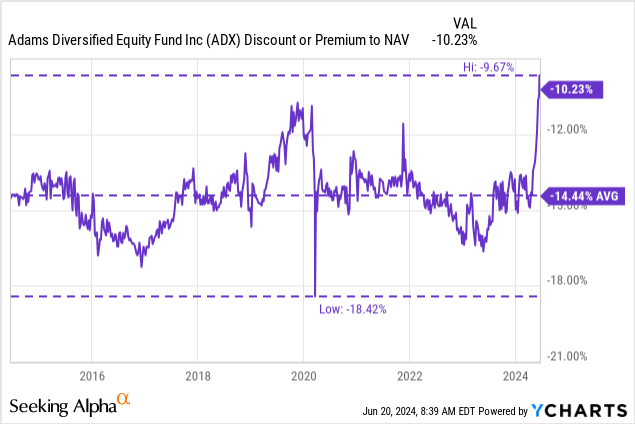

Partially responsible is that the fund has seen its discount narrow, but the fund still offers a sizeable discount. In particular, the catalyst to push that discount to narrow was likely a result of the activist group Saba Capital Management’s direct or indirect influence.

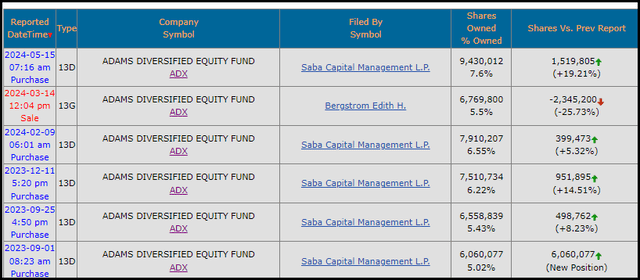

Saba Capital was building a position in the fund slowly through 2023 and took a more sizeable position recently.

ADX Saba Buying (SecForm4)

With that, the fund recently announced an increase in the managed distribution policy, as well as how the fund will meet this new policy. The fund also announced a tender offer that should begin in early July. Upon this announcement, the fund’s discount narrowed materially, but there is still an opportunity here.

ADX Basics

- 1-Year Z-score: 3.25

- Discount/Premium: -10.23%

- Distribution Yield: 8% NAV (new managed minimum distribution policy)

- Expense Ratio: 0.61%

- Leverage: N/A

- Managed Assets: $2.8 billion

- Structure: Perpetual

ADX’s investment objective is simply; “long-term capital appreciation.” The investment policy is quite straightforward as well. They intend to meet this objective by “investing primarily in large U.S. companies.” They also add that they “seek to deliver superior returns over time by investing in a broadly diversified equity portfolio. The Fund invests in a blend of high-quality, large-cap companies.”

ADX New Distribution Policy

The last time we covered ADX, I had a ‘Hold’ rating based on the fund’s discount being quite wide, but that hasn’t been unusual historically. In fact, based on history, it was even trading above its longer-term average discount that it had traded at for the prior decade. The fund also carried a 1-year z-score of 2.02 at the time, meaning on that basis, the fund was also looking expensive over the shorter-term time frame.

So, how can a fund with a 1-year z-score of 3.25 and trading meaningfully above its decade-long average discount – in fact, the fund recently touched the narrowest discount the fund has ever seen in the last decade – now look cheap? Because things have changed.

Their new distribution policy should make them a more appealing fund for income-seeking investors. The tender offer also offers an obvious chance at almost guaranteed alpha, but we will touch on that more specifically below.

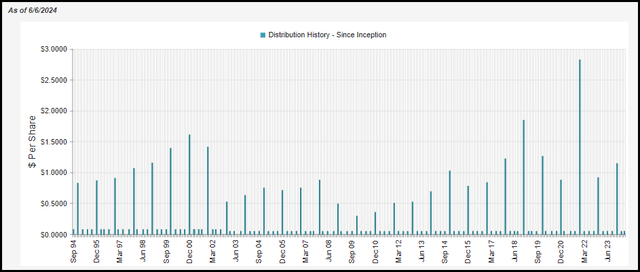

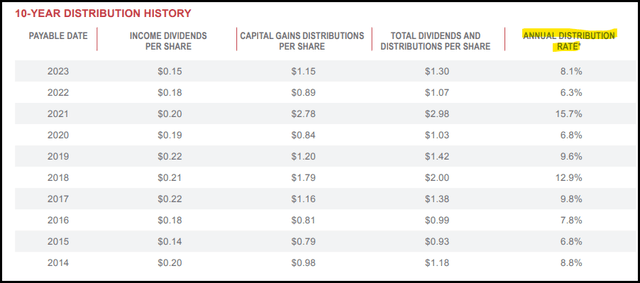

The fund’s previous distribution policy was to pay a low quarterly distribution throughout the first three quarters and then pay a ‘top-off’ distribution at year-end. That top-off distribution would meet the fund’s minimum 6% managed distribution that they were targeting. That was the fund’s distribution policy for decades.

ADX Distribution History (CEFConnect)

Worth noting is that the fund regularly far exceeded the 6% minimum.

ADX Annualized Distribution Rate (Adams Funds)

With the fund’s new distribution policy being ramped up to 8%, one might not even expect too much of a change based on them exceeding that rather regularly anyway. However, with the new 8% minimum, the fund is also changing its payout schedule in that it will be 2% of the average NAV paid out each quarter.

Under the new Policy, the Fund commits to distribute a minimum 8% annual rate of the Fund’s average net asset value (“NAV”) to shareholders beginning with the third quarter distribution expected to be paid at the end of August 2024. The Fund expects to distribute 2% of average NAV for each quarterly distribution, with the fourth quarter distribution expected to be the greater of 2% of average NAV or the amount needed to satisfy minimum distribution requirements of the Internal Revenue Code for regulated investment companies. Average NAV will be based on the average of the previous four quarter-end NAVs per share prior to each declaration date.

With that policy, we should see higher distributions throughout the year and not get a particularly large year-end distribution as the fund had been paying previously. While I know many CEF income investors enjoy monthly distributions, a more smoothed-out distribution throughout the year could still likely attract new income-seeking investors.

ADX Tender Offer – Opportunity For Alpha

The fund also announced they would be conducting a tender offer as well with this new distribution policy. This creates a situation where there is still alpha to be gained based on the fund still trading with a hefty discount. We only have a short paragraph with the announcement, but it really gives us mostly all we need to know.

In addition, the Fund will conduct a tender offer for 10% of its outstanding shares at a price of 98% of NAV per share. A tender offer provides liquidity at a predetermined price to shareholders seeking to rebalance their portfolios, without having to sell their shares on the open market. The tender offer period is expected to commence on July 5, 2024 and expire on August 2, 2024. Specific terms and conditions of the tender offer will be forthcoming in offering materials to be distributed to the Fund’s shareholders.

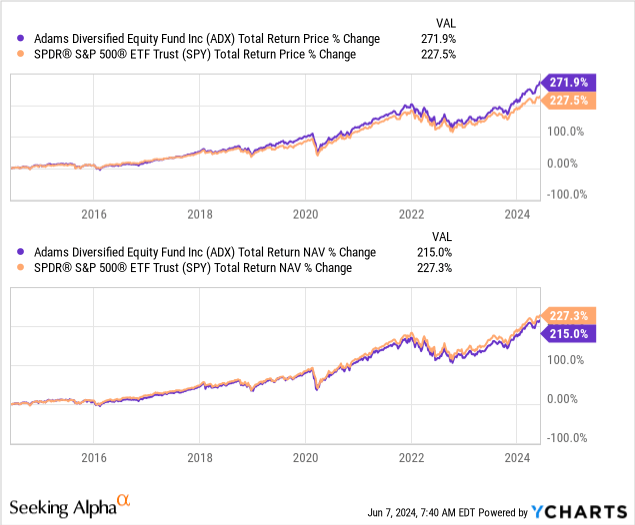

The fact is, this fund mostly correlates with the S&P 500 Index and that leads to some quite similar results on a total NAV return basis. Against the SPDR S&P 500 ETF (SPY), ADX carries a higher expense ratio, so that can explain some of the minor underperformance. Of course, the total share price returns can be more volatile due to discounts/premiums at play for ADX.

YCharts

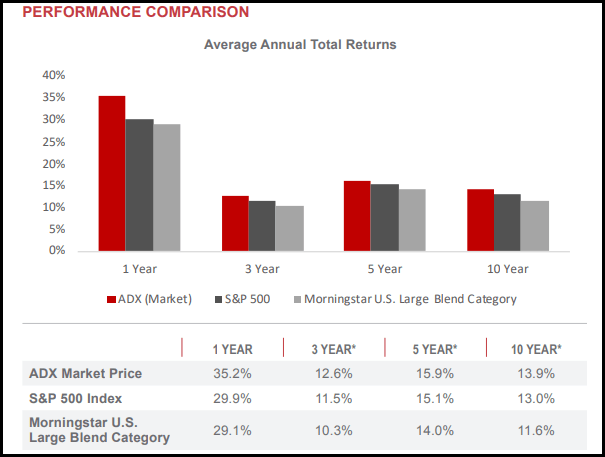

Over shorter periods of time, the expense ratio is going to play less of a role in terms of the divergence between performance. The performance comparison below is for data as of March 31, 2024. Alongside the S&P 500 Index, they also include the Morningstar U.S. Large Blend Category, which it has beaten quite handily.

ADX Annualized Performance (Adams Funds)

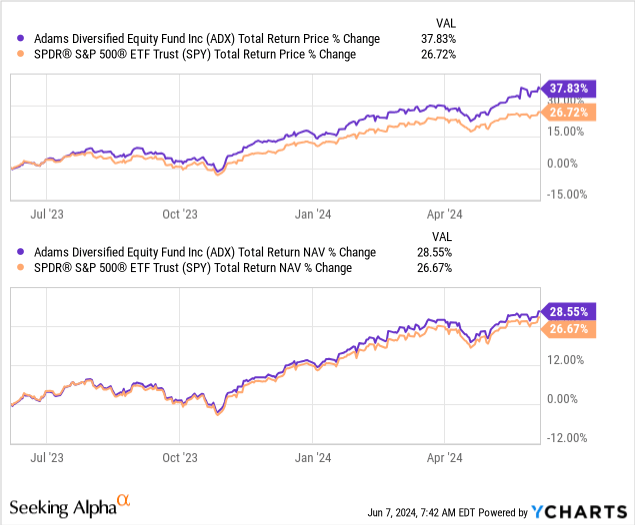

Perhaps even more interesting, we can see that ADX has outperformed SPY over the last year.

YCharts

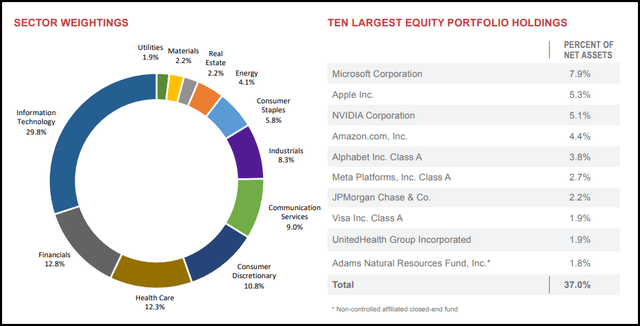

After all, it isn’t the same exact portfolio being carried, but we see many common names.

ADX Sector Weighting (Adams Funds)

That said, that sort of tight correlation with the S&P 500 is where alpha can be made with the tender offer.

The offer is for 98% of NAV; while we don’t know what the NAV will be at the time of expiration of this offer, as it’s in the future, here is an example of how one can profit based on the latest closing data. Shares closed at $20.67 and NAV was $23.23.

Let’s say one can buy 100 shares today for a total of $2067 and participate in the tender offer for 10% of their outstanding shares. That could see a minimum of 10 shares repurchased by the fund at 98% of NAV, or what works out to $22.77 per share.

Note: Not all investors participate in tender offers, whether they aren’t paying attention or just don’t feel like participating. That means that there is a high likelihood that more than 10% of one’s shares will actually be accepted for tender. For the sake of simplicity, we are using the minimum in our example.

That would result in the investor being paid $227.654 for the 10 shares tendered. The investor would still have 90 shares worth $1860.30. When combined with the cash balance after tendering those 10 shares, the balance would come to $2087.954 or roughly $20 in profit.

At that point, there is generally a post-tender slump where the discount will widen back out. At that time, one could consider buying back the shares they had originally tendered and walk away with a bit of cash or buy even more shares with the additional cash they’ll have.

$20 might not be too much, but we only highlighted this as a simple example for only 100 shares. One could easily translate that 1000 shares could be roughly $200, or 10,000 shares could translate into around $2000. Every investor is different, so a lot for some is little for others.

The main point is that it could provide nearly guaranteed alpha relative to investing simply in SPY at this moment, assuming the fund doesn’t start to significantly underperform.

ADX Risks – High Likelihood Of Alpha, But No Guarantee of Profits

Underperforming SPY is one of the key risks that could wipe away any alpha potential.

Market risk, in general, is another huge key risk for investors to consider. If the market has a pullback or drops even further into correction or bear territory over the next couple of months, then that could result in a loss. There could still be potential for alpha to be generated against something like SPY, but there is no guarantee that it will be profitable.

For example, one could buy 100 shares today at $20.67, again for a total cost basis coming in at $2067. However, let’s say NAV drops 10% between now and when the offer expires. That would bring NAV per share down to $20.907, and 98% of that would be $20.49. Thus, no profit would have been made, but there would have been an actual small loss.

The post-tender slump is also something to consider, as it is quite common after a tender offer is conducted that a fund’s discount will simply widen back out. In the case of ADX also announcing a now higher distribution policy that should be paid more regularly throughout the year, that might be enough to minimize that usual slump.

Conclusion

ADX provides investors exposure to an S&P 500-esque portfolio while providing a now higher and more regular distribution policy throughout the year. The change in policy can be helpful for income-seeking investors who want a more smoothed-out distribution throughout the year. The fund is also conducting a tender offer that should result in a high likelihood of generating some alpha against the S&P 500 for investors. Though, not without its own risks to consider.

Read the full article here