")

Written by Nick Ackerman, co-produced by Stanford Chemist.

Utilities have been starting to show a bit more life in the last month or so, but overall, utilities still look quite depressed. The utility sector has continued to face some pressure with the “higher for longer” interest rate environment we find ourselves in. Around the world, we are starting to see rate cuts, but at least those don’t seem necessary in the U.S. just yet. In the U.S. we continue to see inflation remaining sticky and the jobs market remaining strong, leading to a resilient economy overall.

That being said, it can continue to provide an opportunity for more patient investors to put some capital to work. It has been a while since we gave the Reaves Utility Income Trust (NYSE:UTG) a look. This is a solid closed-end fund in the utility space that has delivered a trend of rising distributions over its life. One of the boasts of this fund is being one of only a handful with inception prior to 2008 and never cutting its regular payout to investors.

Given the pressure on UTG’s share price and NAV over the last few years due to higher rates, the distribution rate has become more elevated. However, I believe it isn’t in any danger of needing to be cut and remains sustainable now that most of the damage is in. The next move is expected to be a rate cut still, even if we are staying at a higher overall rate environment for longer than may have been anticipated.

UTG Basics

- 1-Year Z-score: 0.29

- Discount/Premium: 0.81%

- Distribution Yield: 8.32%

- Expense Ratio: 0.94%

- Leverage: 19.81%

- Managed Assets: $2.624 billion

- Structure: Perpetual

UTG’s investment objective is “to provide a high level of after-tax total return, consisting primarily of tax-advantaged dividend income and capital appreciation.” To achieve this, the fund “intends to invest at least 80% of its total assets in dividend-paying common and preferred stocks and debt instruments of companies within the utility industry.”

The fund carries a modest amount of leverage, but it is always worth considering as it does add volatility and that means greater risk. With a higher rate environment, the fund’s leverage costs started to rise materially from where it was a few years ago. Those leverage costs resulted in the fund’s total expense ratio up to 2.32%, as of their last annual report, for the period ending October 31, 2023. If we look back at fiscal year-end 2022, the total expense ratio came in at 1.42% and for FY 2021, we saw a total expense ratio of 1.23%.

Performance – Sticky Premium

Since our last update, the fund has provided some solid total returns. However, we see that it has fallen short of what the S&P 500 Index itself has done during this period. That isn’t an appropriate benchmark, of course, but it can help to provide some context of what the overall market is doing. Given the S&P 500 Index has become primarily the tech-focused Super Six stocks and the complete lack of exposure to those names for UTG, I’m not the least bit disappointed. It isn’t a CEF that is designed to try to compete with the index.

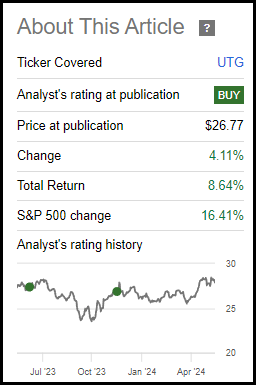

UTG Performance Since Prior Update (Seeking Alpha)

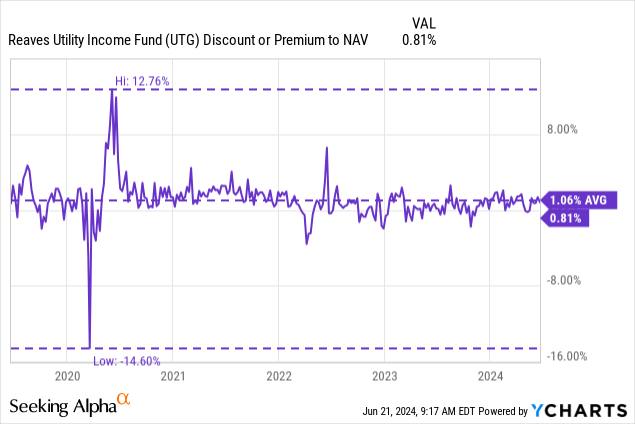

One of the ‘problems’ with this fund is it rarely has offered a huge buying opportunity in the last five years. This fund had in the past traded at some elevated discount levels to its net asset value per share previously, but it has since turned to trading regularly at a premium.

It is actually a closed-end fund that shows an unusually high efficiency in terms of correlating so closely with its NAV in these last five years. There was a bit of volatility through Covid, but otherwise, the share price and NAV have traded quite closely. This is highly unusual for a CEF to trade so closely to its NAV for such extended periods of time.

This creates a situation where it might not be a screaming buy today, being that it is only slightly below its longer-term average premium level. On the other hand, it also could suggest that it is a fair time to buy the fund, as there might not be much downside from discount expansion if even the smallest of dips gets bought up. Further, if one has a more optimistic outlook for utility investments going forward, then this fund can make even more sense.

Distribution – A Strong ~8% Payout

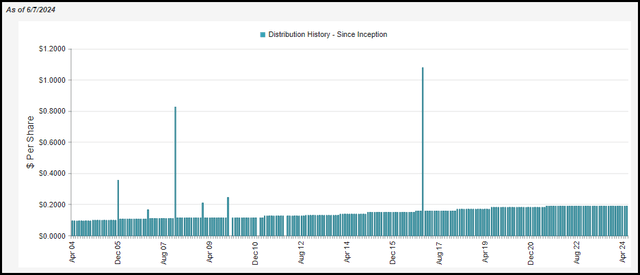

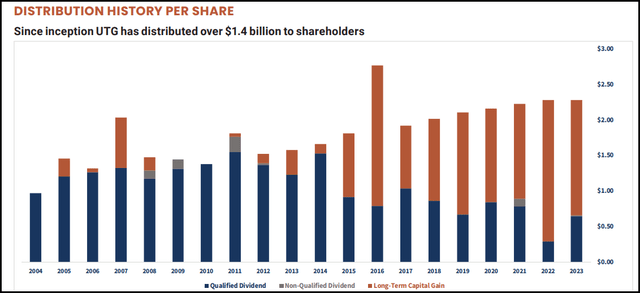

As mentioned, this fund has a long history of paying a stable or growing distribution to investors. There has been a more extended period in the last few years without an increase, but that’s prudent for the current environment. Based on the latest monthly distribution, the fund’s current payout works out to an 8.32% distribution. Given the small premium, the fund does actually have to earn a touch higher rate of 8.38%. This is comfortably below the red flag zone for me, which would kick in closer to 10% or higher.

UTG Distribution History (CEFConnect)

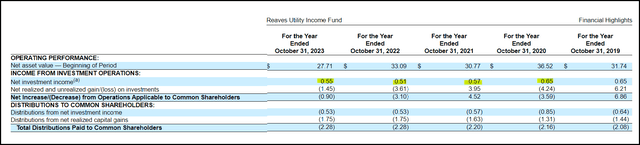

Given that the fund has seen its borrowing rate increase-it’s based on a one-month secured overnight financing rate (“SOFR”) plus 0.65% – the fund’s net investment income has declined in the last several years.

UTG Financial Metrics (Reaves Asset Management)

That has created a situation where the fund will rely on more capital gains to fund the distribution. After all, it is primarily an equity closed-end fund, and that isn’t that unusual. One thing that the fund has now been including is a file that provides a list of dividend changes for its underlying holdings. As dividends get lifted in the underlying portfolio, that should increase UTG’s NII, all else being equal.

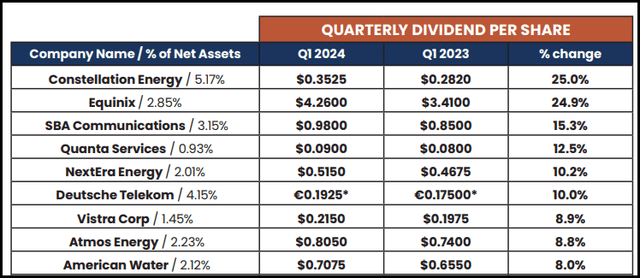

Some of the largest increases seen with the latest Q1 2024 file came from Constellation Energy (CEG) and Equinix (EQIX). CEG is UTG’s largest holding, so that one is particularly nice to see for investors in UTG. I’m sure the investors in CEG itself were also happy to see such an increase.

UTG Holding’s Top Dividend Changes (Reaves Asset Management)

There were three other holdings that they listed as initiating dividends, which will also now start providing regular cash flow to UTG and support its own distribution. Overall, the weighted average dividend increase in its underlying holdings in Q1 2024 came to 7.7%. They also noted that their portfolio of holdings saw no dividend cuts.

These dividend increases, and whenever the Fed does start cutting their target rates, should start to see the fund’s NII increase. The fund’s distribution being covered with capital gains has become a larger and larger part of the distribution. So, seeing that reverse could bring more confidence in the fund and its payout. Some investors feel more comfortable in terms of distribution coverage as it is a more regular and predictable form of cash flow.

UTG Distribution Classification History (Reaves Asset Management)

UTG’s Portfolio

Talking about dividend increases in the fund’s underlying holdings is important, but at the end of the day, this is an actively managed fund. They can trade in and out of positions regularly. For example, they noted having 57 positions being held in the fund as of the end of March 31, 2024, but in our prior update, they listed 51.

The fund’s portfolio turnover rate came in at 32% in FY 2023, so it is a fairly active management team. Not the most active we’ve seen, but there could still be some material changes in each update.

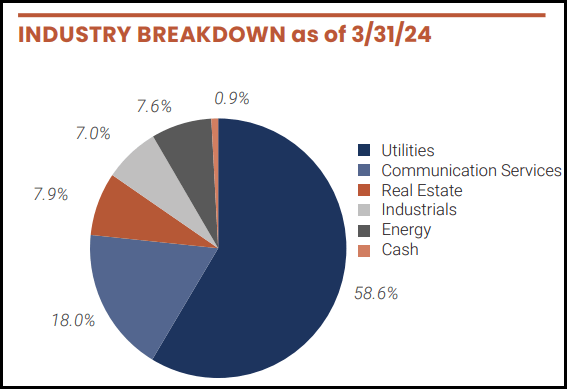

That being said, the utility sleeve still comprises the largest allocation to the fund – as it was in our prior update, as well when it was listed at a weighting of 58.1%. This isn’t uncommon for UTG, but it also isn’t uncommon to see other material sectors exposed to, areas like the communication services and real estate sleeve either.

UTG Industry Allocation (Reaves Asset Management)

EQIX, which we touched on above, is an example of their real estate exposure. However, that isn’t the only REIT this fund is holding; it actually isn’t the only data center REIT either, as the fund also holds Digital Realty Trust (DLR). The fund also holds all three of the publicly traded tower REITs, American Tower (AMT), Crown Castle (CCI) and SBA Communications (SBAC). The fund is primarily focused on being a utility fund, but these are types of holdings that are often considered part of the broader infrastructure space overall.

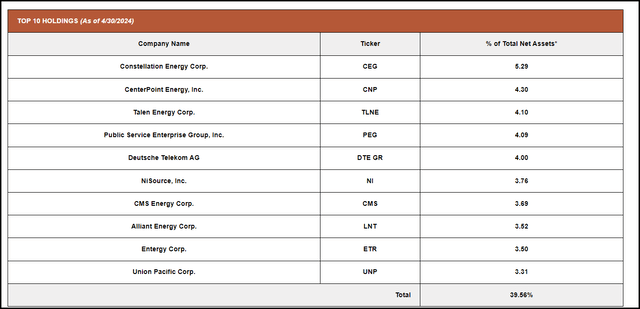

Being a fund with 57 holdings means that it is relatively more concentrated than we typically see in other CEFs. That isn’t necessarily a bad thing, but it is worth noting the more concentrated portfolio, and being a more sector-specific fund also limits diversification further, of course. With that being said, the fund’s top ten holdings comprise nearly 40% of the fund overall. That was down from the 43.17% weight the fund’s top ten had accounted for previously.

UTG Top Ten Holdings (Reaves Asset Management)

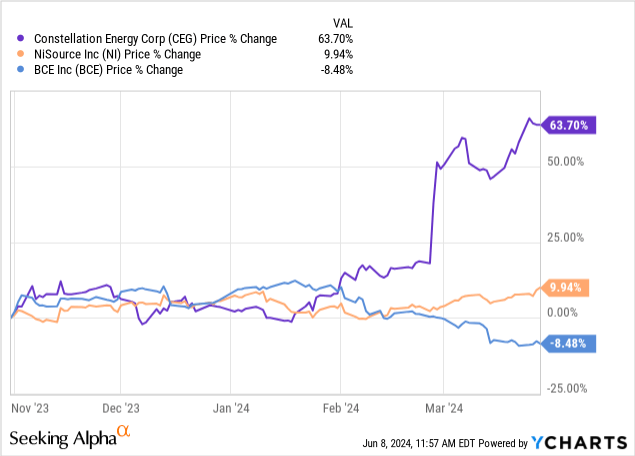

Seeing CEG as the fund’s largest holding is also a change. Previously, the fund was holding NiSource (NI) as its largest position. NI is still a relevant position, but it has slipped from its 4.96% weight. Interestingly, CEG wasn’t even a top ten holding the last time we took a look at the fund.

Another name that was previously a larger holding for the fund was BCE (BCE), the Canadian telecom giant. That fund was the ninth largest and accounted for a 3.85% weight in the fund. Taking a look at the full holding list has seen that the weight dropped to 2.16%.

A driving factor for this was simply the price performance of these three holdings to see these types of shifts. CEG has been absolutely surging during this period while NI performed respectably, it was easily eclipsed.

YCharts

BCE, on the other hand, performed poorly, and I believe for good reason. The company is facing headwinds that are causing its earnings and free cash flow to remain depressed. BCE increased its dividend as usual earlier this year, but coverage isn’t great, and if they can’t turn things around, it could eventually be cut.

For what it’s worth, they do expect FCF to rise once again as CapEx comes down. Ultimately, BCE is in a situation that its American counterparts, Verizon (VZ) and AT&T (T), found themselves in as well not long ago. Those telecom companies also lacked FCF to cover their dividends but are now sitting in a much better place as CapEx began to come down. T did also cut its dividend, but VZ was able to navigate through.

Conclusion

My position is that rate cuts will come, and I don’t mind being patient for that to happen. In my opinion, UTG is not in a dire situation where the fund needs rate cuts. As long as rates have stabilized around these levels, then I believe UTG has stabilized as well. A rate cut would definitely help provide the fund with more breathing room. In a rate cutting environment, it could even put the fund in a situation where it could lift the distribution once again. It has been quite a while since the last increase, I’m sure that some investors would appreciate that. For me, the ~8% distribution is more than enough to make me continue to view this fund as appealing without needing a boosted distribution. For these reasons, while I don’t view it as a screaming buy, I’m still comfortable giving it a ‘Buy’ rating for long-term investors.

Read the full article here