Introduction

I wanted to look at Brady Corporation (NYSE:BRC), which has outperformed the broad market by a decent margin in the last year, to see if it would still be a good time to start a position. With somewhat unimpressive revenue growth, and margins that may come down in the long run, the company is a little too expensive to start a position right now, therefore, I am assigning a hold rating and will monitor how the company’s top-line and margins progress over the next while.

Brady Corporation is an international company that develops solutions to identify and protect people, products, and places, which helps improve security, productivity, and performance.

You can find the products used in various industries, including industrials, data centers and IT departments, laboratories, hospitals, and retail stores. Products like labels, signs lockout/tagout devices to identify equipment. Labels to identify cables in an IT setting and servers in data centers. Labels for conical tubes and vials in the hospital and other similar settings. They are found everywhere, and it has been around for over 100 years and cemented itself at the forefront of identification and protection solutions worldwide.

Financial Performance

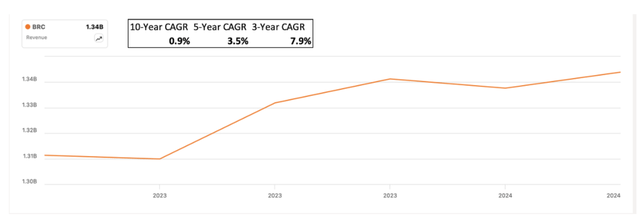

Over the last year, the company’s revenues saw a slight increase, however, it has been quite disappointing. In the last year, the company gained around 2% growth, with an average of less than a percent in the last 6 quarters. That is not going to attract very many investors who are looking for a more exciting company to invest in. In the last decade, the company saw a CAGR of 0.9%, with a slight acceleration in recent years, however, it seems to be slowing down once again.

Seeking Alpha, Author

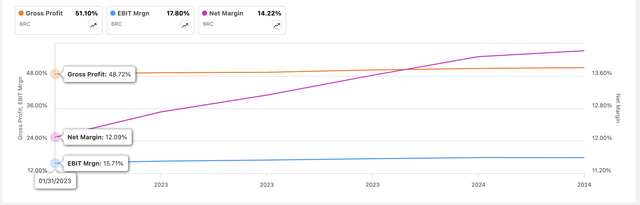

It is not all about the top-line growth, in my opinion. Sure, it helps a lot but, if the company can improve its efficiency and profitability, I think this is just as important if not more important than top-line growth. So, let’s see how the company’s margins progressed throughout the year.

Seeking Alpha

Here, we can see margins across the board improved by around 200bps in each, which is not bad considering this was not driven by top-line improvements. The company benefited from stabilizing input costs and higher sales coming from higher-margin products. The focus on higher-margin products is admirable and if the company continues down this path, I expect further margin improvements in the future, however, that remains to be seen.

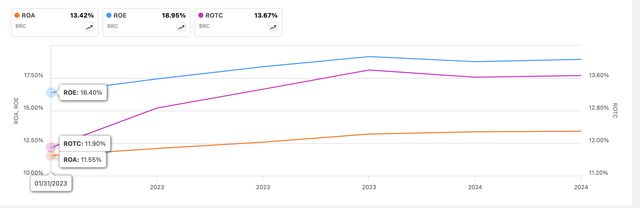

Continuing with efficiency and profitability, the company boasts some nice ROA and ROE percentages, which are well above my minimum of 5% ROA and 10% ROE, which means the management is doing a good job at utilizing the company’s assets and shareholder capital, thus creating value. Furthermore, I like to look at the company’s return on total capital, or ROTC, which measures how efficiently the management allocates all the resources to profitable projects. Here, I usually look for a company that can achieve at least 10% and BRC is well above that too, which tells me the company is enjoying some sort of competitive advantage and has a decent moat.

Seeking Alpha

Now, let’s look at the company’s overall financial health. As of Q3 ’24, which was filed on May 22nd ’24, BRC had around $160m in cash and equivalents, against around $64m in long-term debt. This is a good position to be in since the cash can easily cover any outstanding debt and operating income covers annual interest expenses on that debt over 80 times, so the company is at no risk of insolvency, and could utilize debt more to further the growth of the company if it wanted to. However, this may put off some more debt-averse people.

Overall, I am a bit disappointed in the lack of top-line growth, but with the improvements in margins, coupled with fantastic efficiency and profitability returns, and a solid balance sheet health, BRC could be a contender for a long-term position in my portfolio.

Comments on the Outlook

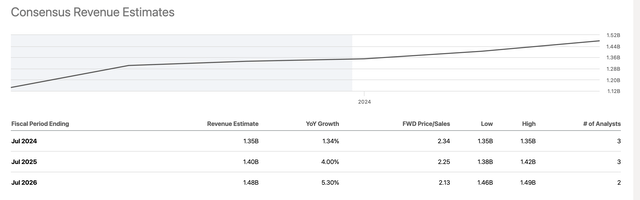

In the last couple of quarters, the company has experienced a decline in top-line growth due to divested businesses. In Q3, these divestitures accounted for -2.3% growth, while in Q2, this resulted in -3.5% growth. The top line was affected quite a bit because of it, even though the management is downplaying it as “not a significant growth vector”. With the business divested, which was called Personal Concepts, are we expecting a substantial improvement to the top-line growth going forward? Without the effects of the divested businesses, organic growth was around 4.5%, which as we know is still below the company’s 3-year CAGR. The company expects to grow at “low-single digits” for FY24, in line with Q3, so nothing that would point towards an improvement so far. Analysts are expecting the company to grow at around 1.3% for FY24, and accelerate to that low single-digit growth, which means that the divested businesses will finally stop weighing on the top-line going forward.

Seeking Alpha

I would like to see the company using its cash position more aggressively and would like to see a rejuvenation in the top line over the next year or so.

In terms of margins, the company in a Q3 earnings call increased its FY24 guidance on a GAAP and non-GAAP basis: “We are increasing our full year fiscal 2024 EPS guidance range of $3.80 to $3.95 on a GAAP basis and $3.95 to $4.10 on a non-GAAP basis, to $3.93 to $4 on a GAAP basis and to $4.08 to $4.15 on a non-GAAP basis.”

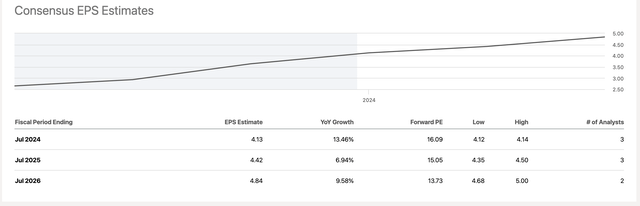

This shows me that the company is confident in its ability to keep improving its margins going forward, which is a very positive sign for an investor. Even if the company doesn’t grow its top line at more than a few percentages, streamlining the business but cutting out certain revenues that did not fit the portfolio, should help it become much more efficient, even though ironically, the divested Personal Concepts business was a high-margin business. Nevertheless, the consensus estimates, see decent EPS growth over the next couple of years, which are bound to change over time, but as it stands right now, I like what I see here.

Seeking Alpha

In my opinion, the company’s margins are already very healthy, and if it can continue to improve even by just a little more over the next couple of quarters, I don’t see how the company’s valuation will not continue to go up even more. However, during the Q3 call, the management did say that the high gross margin of 51%+ is a bit above what they expect the company to achieve in the long term, which means they don’t expect such margins to be sustained going forward and expect these to fall to around 50% in the long-run.

Valuation

As usual, I will approach my valuation model with a conservative mindset. I don’t like being too optimistic about revenue and margin potential, that way I am getting a built-in margin of safety.

So, for revenue growth, I went with around 1% growth in FY24, which still has a lot of divested business negativity. After that, the company will match its organic growth of around 5%, which will taper off to around 1% by FY33. I chose these rates mainly because the company needs to prove to me that it can grow at a much higher pace than low single-digits, and so far, there is nothing on the horizon. Additionally, I also modeled two more cases to give myself a range of possible outcomes.

Author

For margins, I went with the improved numbers for the next few years, and then I will echo the management’s words and bring down gross margins to that 50% mark in the long run. I would like to see how long the company will enjoy such margins before coming down, but in my model, it’s got around 5 years or so, which may be more than what the management is thinking.

Author

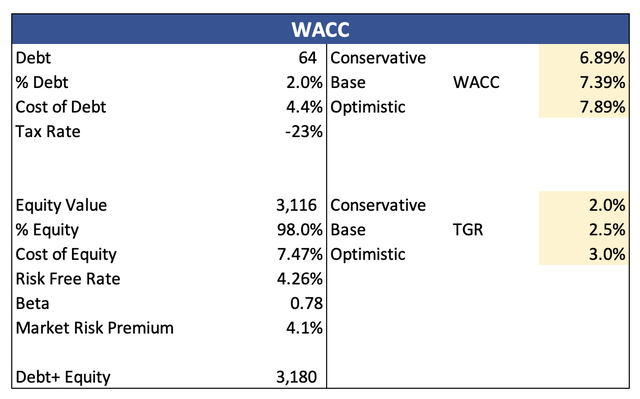

For the DCF model, I went with the company’s WACC of around 7.4% as my discount rate and 2.5% terminal growth rate because I want it to at least match the US long-term inflation goal.

Author

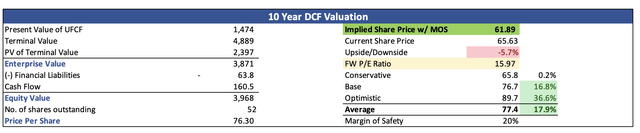

Furthermore, in case my margin assumptions are a bit too optimistic, I decided to discount the final intrinsic value by 20%, to give myself some room for error in my estimates. With that said, BRC’s intrinsic value is around $62 a share, which means it is currently not a very attractive investment.

Author

Closing Comments

I would like to see how the company’s sales progress over the next few quarters and whether it manages to grow at a better rate than “low single-digits” as that is not very appealing to me either. Furthermore, I would like to see what the company has in store for further efficiencies. With the transportation costs coming down further, we may see some further improvements there, but marginal, I would guess. I don’t expect margins to see any substantial improvements going forward, just like the management mentioned in the previous call. Therefore, I am assigning the company a hold rating and would like to see the share price come down slightly before considering starting a position.

It has the potential to be in my portfolio because of its healthy balance sheet, solid margins, and efficiency and profitability metrics, however, the market may not value its low sales growth, which may in the end bring it down to a more acceptable price, and a better entry point. I’ll monitor the situation on the sidelines for now.

Read the full article here