Lululemon (NASDAQ:LULU) has been among the worst-performing stocks in the S&P 500 so far this year. The athleisure retailer has struggled amid shifting consumer preferences and new competition in what’s often a somewhat low-margin business. What’s more, there are growing signs that many consumer cohorts are coming under pressure amid a rising unemployment rate and cooling wage gains.

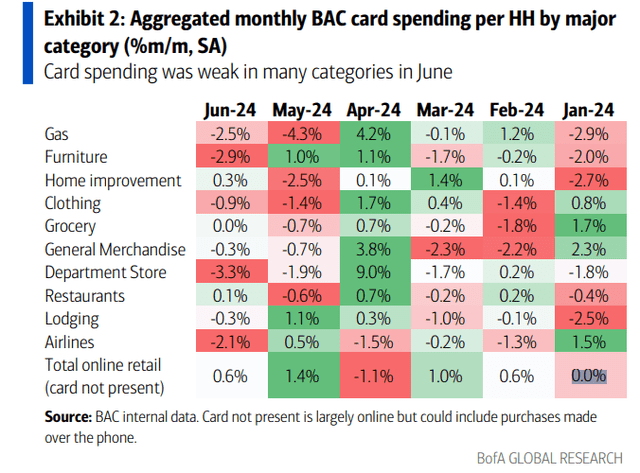

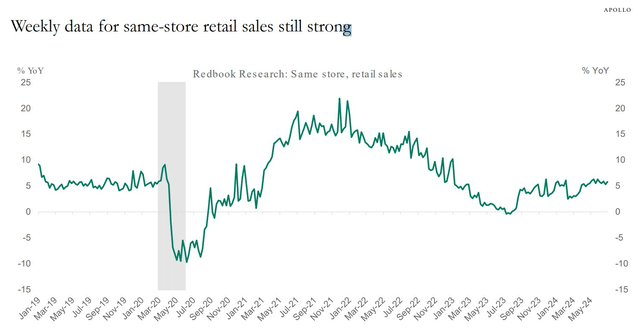

We’ll get a fresh read on that front on Tuesday morning this week with the June Retail Sales report put out by the US Census Bureau. While Johnson Redbook sales have continued to show solid 5%+ YoY retail sales growth, total card data from Bank of America suggests that Tuesday’s key report could be a disappointment. We’ll see how it plays out, but it’s clear that some air has been let out of the consumer bubble, so to speak. Nike’s (NKE) recent quarter was yet another sign of discretionary weakness, though that may have been more of a firm-specific issue.

I am upgrading shares of LULU from a hold to a buy. I see today’s valuation as compelling while its technical situation, which I noted was particularly precarious earlier this year, now offers investors a favorable risk/reward entry with the company’s Q2 report due out next month.

BofA: Another month of soft retail spending, Retail sales probably declined in June

BofA Global Research

Johnson Redbook Retail Sales Holding Up Well YoY

Apollo Global

Back in May, LULU reported a decent set of quarterly results, but it was the $36 billion market cap company’s Q2 guidance that offered a boost. Q1 GAAP EPS of $2.54 topped the Wall Street consensus estimate of $2.42 while revenue of $2.21 billion, up 10.5% from year-ago levels, was a modest beat. Comp-store sales jumped 6%, but there was a one-percentage point hit from adverse currency moves.

Moreover, LULU’s gross margin actually improved by 20 basis points to 57.7%, though its operating margin dipped by half a percentage point. Strong international sales helped drive profits, up 40%, compared to just a 2% YoY rise in domestic sales. The higher gross margin was buttressed by better interest income.

Its men’s business was impressive in its growth, with sales increasing by 15% due to new products and expansions within existing lines. But concerns remain surrounding its women’s business – sales were light; however, LULU sees a better second half there.

Now, here’s where things turned a bit more hopeful for the Canadian Apparel, Accessories, and Luxury Goods company. For the quarter about to wrap up, the management team stated in April that it sees net revenue to be in the range of $2.4 billion to $2.42 billion, slightly below the $2.45 billion consensus. Diluted EPS for Q2 was seen in the $2.92 to $2.97 range, also underestimates, which were $3.03 at the time. FY 2024 top and bottom-line numbers were also solid, though, helping shares to rally 4.8% in the following session.

Investors should monitor LULU’s margins in next month’s Q2 report, as well as how its women’s business performs. Additionally, while strength internationally is helpful, we need to see US sales hang in there. As it stands, the options market has priced in a small 4.9% earnings-related stock price swing when analyzing the at-the-money straddle, expiring soonest after the August report. Analysts expect GAAP EPS to come in at $2.96 on sales of $2.43 billion.

Key risks include poor execution of new store openings and product launches that don’t match emerging consumer preferences. Higher interest rates and overall weaker retail sales would hurt the firm’s top line, while increased labor costs would be a threat to the bottom line.

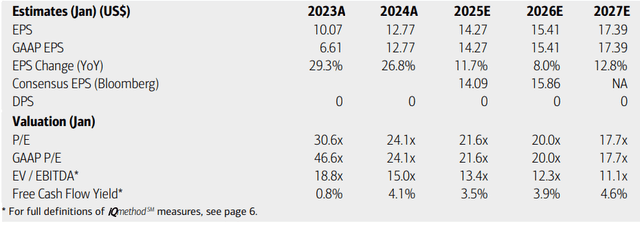

On earnings, analysts at BofA see operating GAAP EPS rising by more than 25% this year, with an earnings growth slowdown over the next two years. Per-share profits could top $17 by 2027, though. The current Seeking Alpha consensus numbers are quite close to what BofA sees.

That results in a historically low price-to-earnings ratio and an EV/EBITDA ratio that is now below that of the S&P 500 – something rarely seen in LULU’s history. Its free cash flow yield is nearly 5%, which is a healthy number for a high-growth company. No dividends are expected to be paid, however.

Lululemon: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

If we assume a forward PEG ratio of 2, below its long-term average of 2.4, and assume a long-term EPS growth rate of 12%, then LULU’s P/E should be 24x. With EPS of $15 over the next 12 months expected, a fair value for the stock is $360.

I have reduced my PEG ratio estimate due to the emerging concerns with the consumer and obvious signs that the athleisure category is not as strong as it was just last year. But the valuation case is compelling even with that discount.

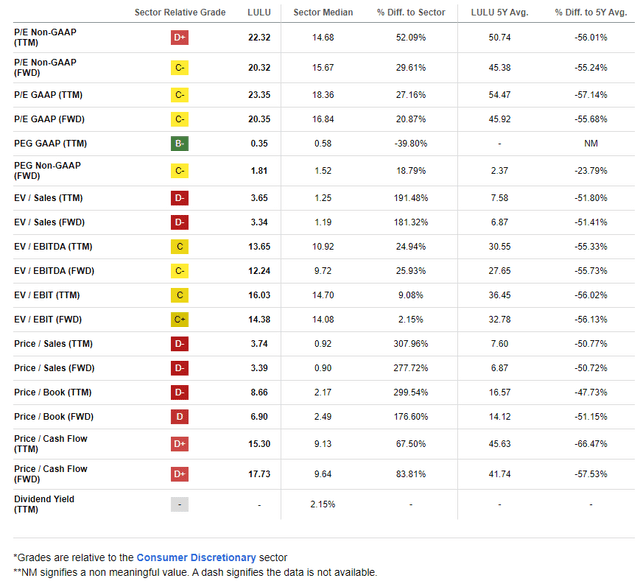

LULU: Shares Now Historically Cheap Across Metrics

Seeking Alpha

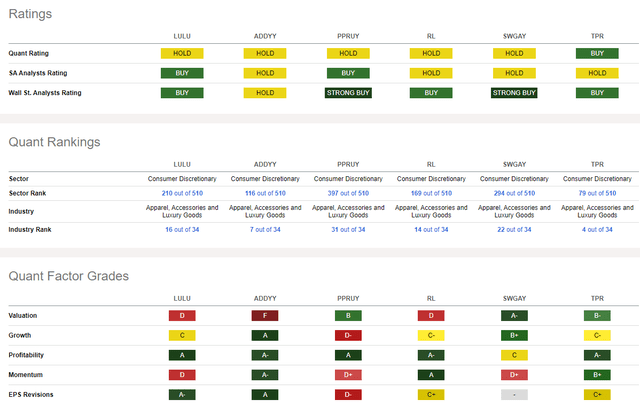

Compared to its peers, LULU features a soft valuation grade, but if you step back and assess some of the metrics pictured above, the stock trades at a major discount to its 5-year average multiples.

Furthermore, EPS growth is still seen in the 11% to 13% range. LULU sports strong profitability metrics compared to its competitors, while its EPS revision trend is actually quite positive following the relief Q2 report. Still, share-price momentum has been dreadful since late last year, but I will note key price points that should offer hope to the bulls.

Competitor Analysis

Seeking Alpha

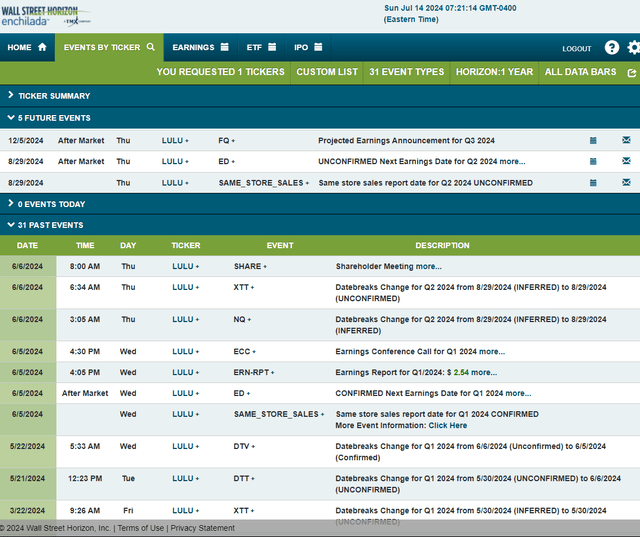

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q2 2024 earnings date of Thursday, August 29 AMC. The retailer also reports same-store sales within the quarterly update next month. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

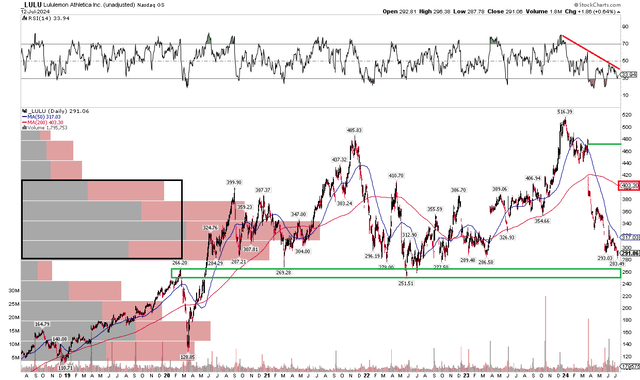

Earlier this year, I voiced significant concerns with LULU’s technicals. Notice in the chart below that shares indeed dropped from near $390 at the time to under $300 today. Now with a falling long-term 200-day moving average, the bears clearly have control of the primary trend.

But take a look at the graph below. It doesn’t take a CMT to spot where critical support comes into play. The $251 to $269 zone has been an area of historical importance. It’s where LULU met initial selling pressure pre-COVID, and where the stock found support on several occasions from early 2021 through early 2023.

Long here with a stop under $240 appears as a favorable risk/reward strategy, in my view. Of course, after such a large drop, there is now a large amount of volume by price up to about $400 while the RSI momentum oscillator at the top of the chart remains in a bearish trend. Bulls can look up to a price gap way up in the high $400s for a potential fill, but that is a long way off.

LULU: Shares Approach Important Support

Stockcharts.com

The Bottom Line

I have a buy rating on LULU. Shares are inexpensive given EPS growth trends, despite concerns about the consumer and competition. The stock’s technical situation appears more attractive today, with a solid risk/reward opportunity ahead of earnings next month.

Read the full article here