ACM Research (NASDAQ:ACMR) is a niche WFE (Wafer Fab Equipment) manufacturer with a focus on the Chinese WFE markets. ACMR has established itself as the domestic leader in single wafer and batch wet cleaning equipment while rapidly expanding into the electro-chemical plating (ECP), ALD furnace, PECVD, and Track equipment markets. ACMR is in a prime position to ride the wave of China’s semiconductor drive for self-sufficiency. Furthermore, ACMR is trading at a mere fraction of its publicly-traded, 82%-owned subsidiary, ACM Shanghai. I believe the company is significantly undervalued and therefore, give ACMR a “strong buy” rating.

ACMR’s history

ACMR was founded in California in 1998 by its founder David Wang. Dr. Wang is both an entrepreneur and a scientist. ACMR’s official website states that “he is the inventor of stress-free Cu polishing technology, and he holds more than 100 patents in semiconductor equipment and process technology”.

Wang’s background is perfect for a WFE company. China’s Pudong Talent International Hub’s website has a detailed introduction of Wang’s story. First of all, he is a graduate of the most prestigious Tsinghua University in China with a bachelor’s degree in Precision Instruments. So he has a solid academic and theoretic foundation for a career in the semiconductor industry. Secondly, Wang was among the first group of Chinese talents to study overseas. In 1984, he obtained a scholarship from the Ministry of Education to study in Japan’s Osaka University as part of Tsinghua University’s exchange program. At Osaka University, Wang received a Master and PhD of Engineering in Precision Engineering. He was mentored by Osaka University’s renowned professor, Mori Yuzo. And his research focused on semiconductor precision processing and semiconductor equipment. After getting his PhD in Japan, Wang then went to the U.S. and joined the Nanoelectronics Laboratory of the Department of Electrical Engineering at the University of Cincinnati for postdoctoral research. After his post-doc position, he joined Quester Technology and quickly became manager of the R&D department.

Wang founded ACM Research in California in 1998. In 2005, Jiang Shangzhou, a legendary figure in China’s semiconductor industry who was key to the founding of Semiconductor Manufacturing International Corporation (SMIC), persuaded Wang to establish ACM Shanghai. ACM Shanghai’s goal was to break through with single-wafer cleaning equipment, which had a large market size and was dominated by Japanese companies such as DNS and TEL.

In 2008, ACMR successfully developed SAPS technology. In 2011, ACMR received the first order of single-wafer cleaning equipment from SK Hynix for its products using the SAPS technology. In 2015, ACMR successfully developed the TEBO technology. The company’s products were later qualified by China’s leading domestic logic and memory fabs such as Yangtze Memory Technologies, SMIC and Hua Hong Group. ACMR then started to take off. During the past five years, ACMR has grown its revenue and net income at a CAGR of almost 50%.

SeekingAlpha

ACMR is in a perfect position to benefit from China’s drive for semiconductor self-sufficiency

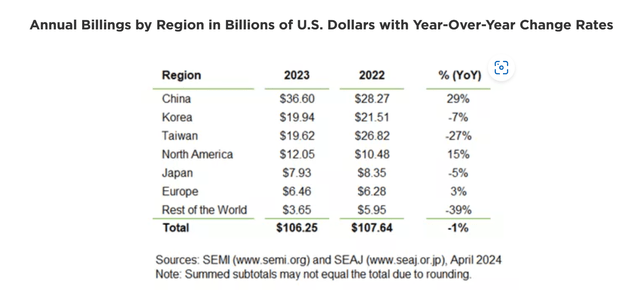

According to SEMI, worldwide sales of semiconductor manufacturing equipment were $106.3 billion in 2023. China is the largest market, with $36.6 billion of sales. China was also the fastest growing market in 2023, with growth of 29% year-over-year, compared to a decline of 1.3% across the globe. Needless to say, China’s one of the most important, if not the most important market for WFE.

SEMI

According to ACMR’s investor presentation, of China’s $36.6 billion of WFE sales, ACMR’s products portfolio has a Serviceable Available Market (“SAM”) of approximately $2.4 billion.

ACMR

ACMR’s current revenue in China mostly comes from chemical cleaning equipment. The demand for cleaning equipment in China has been surging due to wafer fab expansions and technological advancements. ACMR’s portfolio of cleaning products with TEBO, and Tahoe technologies cover approximately 90-95% of all the cleaning steps required for wafer manufacturing. ACMR has also developed IPA and supercritical CO2 drying technologies to enhance its competitive edge.

In China, ACMR competes against global giants such as DNS, TEL, LAM Research (LAM), and SEMES. After years taking shares from foreign competitors. According to the annual report of ACMR’s subsidiary ACM Shanghai, ACMR’s current market share in China’s cleaning equipment market is 23%. In the long term, the company aims for 55% of market share, replacing DNS as the dominant player.

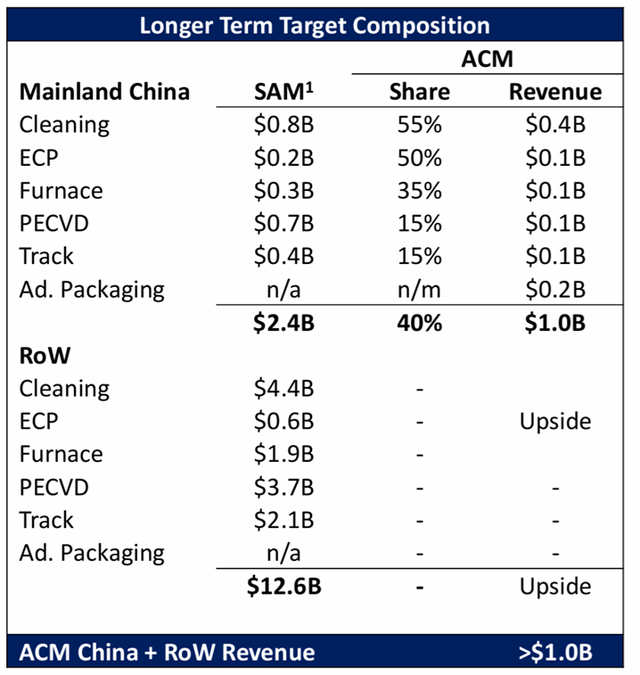

Besides cleaning equipment, the company has expanded its products offering to electro-chemical plating (ECP), advanced packaging, vertical furnace, Track and PECVD. ACMR’s portfolio now covers both front-end wafer manufacturing and back-end advanced packaging. In the above chart, ACMR has laid out the addressable market and ACMR’s long term goals.

I think ACMR is extremely smart in terms of choosing which market to enter. ACMR has avoided competing against the best domestic players such as Naura and AMEC in etching and deposition. Instead, the company focuses on a niche market with limited competition. For instance, the ECP market has only one major player, namely Lam Research. ACMR decided to enter the ECP market because its Founder David Wang has actually systematically studied precision copper plating and electrical polishing at Osaka University and ACMR’s very first product was an ECP product. The product failed because it was too advanced back then. However, Wang is clearly one of the top experts in ECP. This is probably why ACMR is confident that it can take 50% of market share in China’s ECP market.

Similarly, ACMR faces very limited competition in Track. The Track market is dominated by TEL globally. There’s only one domestic competitor, KINGSEMI. KINGSEMI’s main advantage is that it has been the indisputable leader in the Track market since it was spun-out of the Shenyang Institute of Automation, Chinese Academy of Sciences. However, KINGSEMI is a semi-SOE and its operation is not very efficient. ACMR is much more flexible and market-driven than KINGSEMI. Therefore, ACMR is very likely to gain some share from KINGSEMI in the Track market.

Overall, I think ACMR will continue to take share from DNS and TEL in the cleaning equipment market, and with an ever-expanding portfolio of products, ACMR will have no problem achieving its $1 billion revenue goal in the next few years.

Financial projections and valuation

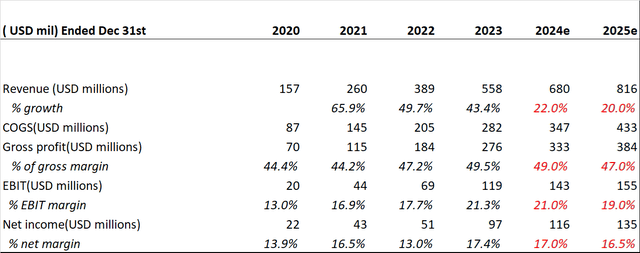

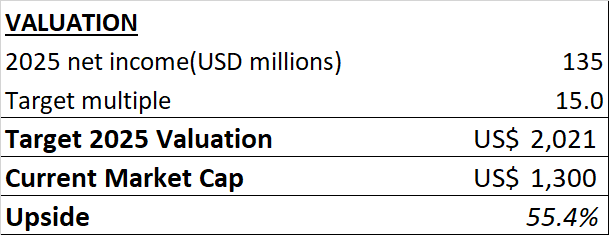

In my model, I assumed that the ACMR’s revenue will continue to grow at 20% a year, which is consistent with management’s guidance. I also assume that ACMR’s margin will peak out and gradually decline to a normal level in FY2024 and FY2025. Combining these assumptions, I arrive at my own estimate of ACMR’s 2025 net income of $135 million.

author’s estimate

On the valuation side, I applied a 15 times TTM P/E multiple, which is roughly a 50% discount to the sector average. The discount mainly reflects the China risk.

author’s estimate

Based on my assumptions, ACMR appears to be undervalued at this price.

From another perspective, ACMR’s 82% owned subsidiary ACM Shanghai has a market cap of $5.2 billion, or roughly 4 times the market cap of ACMR. At the current price, ACMR’s stake in ACM Shanghai is worth more than $4 billion. The Chinese investors are willing to pay 4 times the price of the same company. This says a lot about geopolitical tension.

Risks to consider

The biggest risk to ACMR is that both the Chinese government and U.S. government can hurt ACMR as geopolitical tensions rise. For instance, ACMR’s founder is a Chinese-born U.S. citizen. The U.S. government has banned U.S. citizens from providing support to Chinese semiconductor manufacturers. So far, Wang has not been affected by the ban. However, at some point, Wang will likely face some restrictions on his ability to lead a major Chinese WFE company as a U.S. citizen. This may pose some risk to ACMR’s operation.

Secondly, ACMR is subject to export license requirements by the U.S. government in terms of acquiring certain parts and software for the production of ACMR’s equipment. The introduction of additional export controls by U.S., Japan or the Netherlands could further adversely impact ACM Shanghai’s supply chain and make it harder for ACMR to expand in China.

Lastly, ACMR’s stock is extremely volatile given it is likely considered a Chinese stock even though it’s different from Chinese ADRs because it is headquartered in the U.S.

Conclusion

ACMR has a strong presence in China’s vast WFE market and will likely continue to grow rapidly due to wafer fab expansions and the ongoing trend of domestic substitution in China. Even though the geopolitical risk is high, I believe ACMR is significantly undervalued given its growth potential. Therefore, I am giving ACMR a “strong buy” rating.

Read the full article here