")

West Fraser Timber Co. Ltd. (NYSE:WFG) is a wood products and lumber play focused on the US and Canadian markets, but also a small business in Europe. The story here is that they are quite scaled. They bought a company called Norbord some years ago, and their inorganic growth strategy has been pretty successful and their business’ run-rate performances are improving on average compared to previous downcycles. They are pushing more, not less, lumber onto the US market despite the low levels of profitability, pressuring regional peers, and their OSB business is managing sequential improvement as their Allendale facility scales and average costs fall.

While lumber is more commodified and a bit less supported by non-discretionary and secular forces, OSB (oriented strand board) is more valuable. It can command positive EBITDA margins in a downcycle, although the performance has been under more pressure than we thought in our previous coverage.

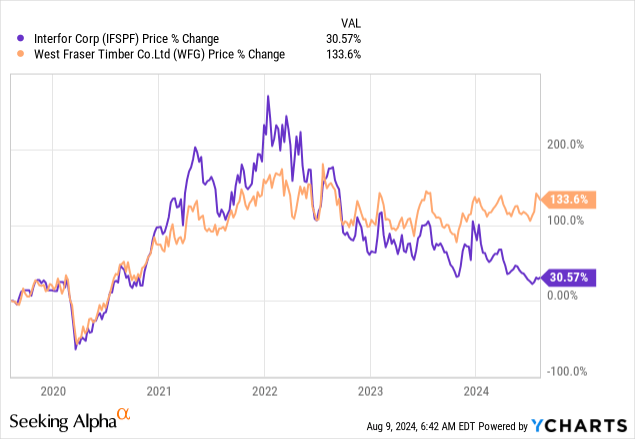

We tend to draw comparisons between WFG and Interfor (OTCPK:IFSPF) which is a lumber pure play and does not have OSB facilities. WFG is a more resilient stock, and the relative underperformance of Interfor signals that lumber is clearly in the downcycle. The issue is that lumber is still not rationalizing. With WFG margins having worsened in lumber, they probably will with Interfor as well when it reports. Although both have more similar cost assets now after some mill closures that Interfor did. While Interfor is a play for the upcycle in lumber, we think resilience and WFG are a better pick for the moment as macroeconomic risks seem to be developing.

Latest Earnings

The situation in lumber markets has been difficult. Most players are operating in negative profitability and the levels of supply into the market are unsustainable. Marginal mills are being closed by the major players, and they are trying to run more shifts at the profitable mills to improve the profitability situation.

WFG might be the outlier here, as they are actually seeing sequential growth in lumber shipments despite a constant price environment. Operating losses in that business are growing, although they are still doing some rationalization of shifts at less profitable mills, primarily in Canada. They are likely using their OSB business to subsidize the losses from their lumber business to put more marginal mills at competitors. Furthermore, they are likely ramping up previous industrial investments in lumber and bringing them to fruition. In industrial businesses like this, the cost of production is the most important competitive moat, and you want to see marginal supply shaken permanently out of the market if possible, if you can afford to do that.

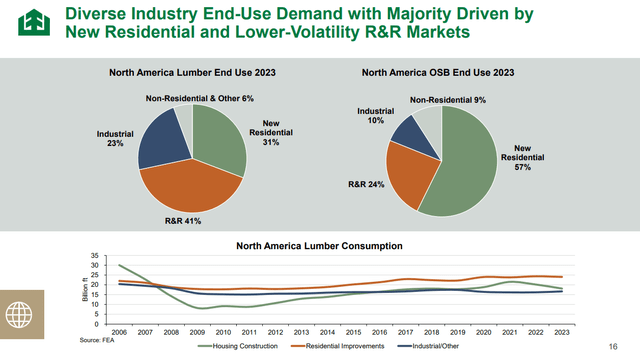

End Markets (Q2 Pres)

Lumber is very dependent on renovation, repair and remodeling markets. These tend to be more discretionary than new residential building, which has more force behind it from the housing shortage in the US. Even though the new residential markets are pressured by the higher mortgage rates and financing rates for development, so housing starts are still struggling. R&R markets have not been benefiting from a typically strong spring season, which spells trouble for the whole rest of the year. The bigger seasonal windfall did not come in the spring. Destocking has also been an issue, where less readily available lumber some years ago meant buying patterns demonstrated more urgency.

Sequential Volumes (Q2 Pres)

Sequential EBITDA (Q2 Pres)

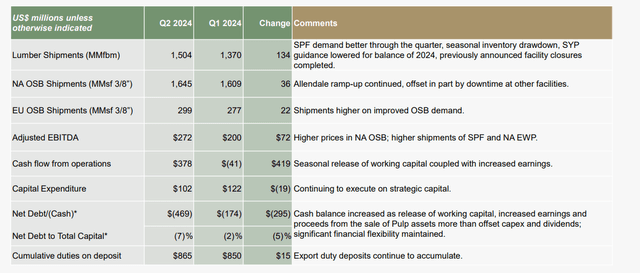

OSB shipments are growing a little sequentially. There is some downtime at facilities, but that decline is being offset with growth at a newer facility in Allendale, which is reducing average costs as its margin profile is better than that of WFG’s existing assets. Other capital projects have also come to fruition, driving adjusted EBITDA improvements sequentially.

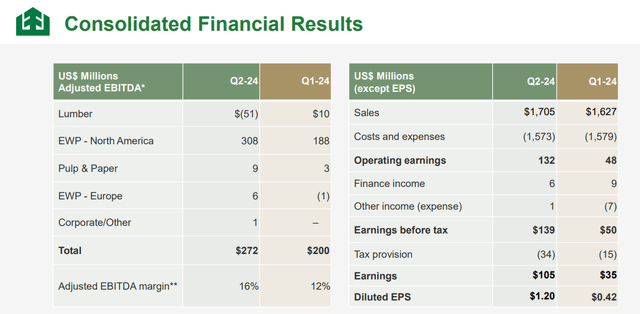

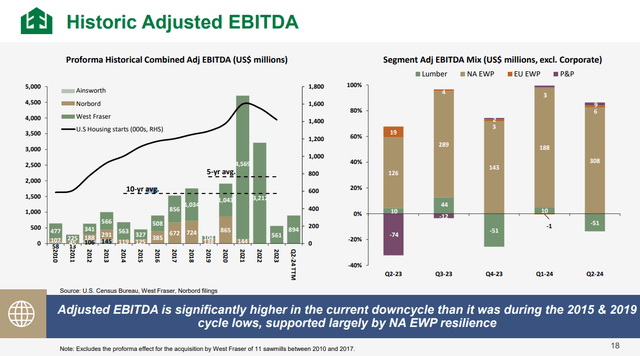

One of the comments from management is that the integration and synergies that have come from the Norbord acquisition have improved EBITDA in the current downcycle by about $650 million. Their profit situation is pretty resilient, and it will help them outlast the downcycles without too much capitulation. This was normalized before Norbord was consolidated into WFG.

Historic EBITDA (Q2 Pres)

Bottom Line

The forecasts for volume this year show declines incoming towards the end of the year, but the company is stating that this is mostly to do with seasonal effects and planned downtime in facilities. WFG is pushing hard to maintain its volumes since it can afford to.

Housing starts are still quite weak, and macro in general is a concern. Consider that while rates may start to fall, it will probably come with larger deltas in unemployment, which is a critical measure for mortgage market health and also for property values, which are all leveraged assets. R&R is already under pressure and having a weak year in the current economic setup. A soft landing is a narrow window and an unlikely bet in our view, but might be the only basis to make this investment.

West Fraser Timber Co. Ltd. is a pass, although more resilient than Interfor, which would be the more aggressive cycle play and also with a strong management record in pivoting assets and in inorganic and accretive growth. We want to get out of the way of playing with risks like WFG’s.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here