A few weeks ago, I published an article titled “Banking Crisis: The next domino is falling” and while it seemed in the last few weeks like a potential banking crisis was contained, the collapse of First Republic Bank probably led to some doubts again.

And while I don’t know if we are on our way towards the next severe banking crisis, I am quite confident we are on our way towards a recession. In the following article, I will provide an update where we are – in my opinion – in the cycle and what might happen in the next few months.

Buffett And Munger

The previous weekend, Berkshire Hathaway (BRK.B) held its Annual General Meeting and Charlie Munger and Warren Buffett provided valuable insights once again. Not very surprisingly, both are expecting that the majority of Berkshire’s businesses will make less money in 2023 (compared to 2022). Two other statements were much more interesting (video version here). On the one hand, Charlie Munger told investors to get used to making less money and Warren Buffett told investors that an “incredible period” for the U.S. economy has come to an end.

And both statements can be interpreted as just looking at the coming quarters. As the business cycle is coming to an end, earnings will decline, and investors will make less money – that is just a typical pattern. However, a more likely interpretation is the following: Buffett and Munger and not just talking about the current business cycle and the coming quarters but are looking at much longer timeframes and are commenting on a decade-long huge debt cycle coming to an end. And that would be quite a statement from the investor that told us never to bet against the United States of America and was most of the time optimistic about the long-term prospects.

Early Warning Indicators

But let’s rewind a bit and look at the last few months, in which I (and many others) warned quite often that several early warning indicators are signaling a recession. Let me provide just a quick recap.

One of the best early warning indicators for a recession is the stock market itself, for example the S&P 500 (SPY). And in late 2021, the S&P 500 marked its all-time high around 4,800 and that top might have been a first early warning sign. However, the problem is that we know only in hindsight when the stock market marked its top (even now in May 2023 we can’t be completely sure if we won’t see higher stock prices again before a recession and/or a huge decline). But in hindsight, it seems like the stock market was warning us starting in early 2022 that the bull market was over and more difficult times were ahead.

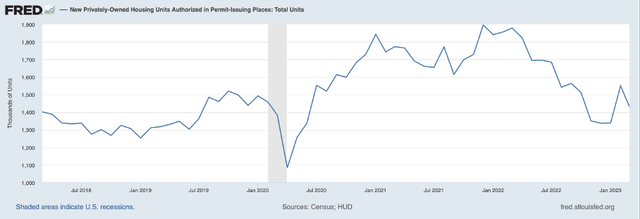

Additionally, we are seeing housing permits declining for several months in a row now (only interrupted by an increase in February 2023). Huge investments – and buying or building a house is for most people the biggest investment they will make during their lifetime – are often postponed when economic conditions are challenging, and this is reflected in lower housing permits. And this is probably the best indicator as the permit for a house is one of the first steps (ahead of actually building a house).

FRED

Other numbers to look at would be the employees in construction as well as total construction spendings – and while these two numbers have difficulties to grow, we don’t see a decline yet.

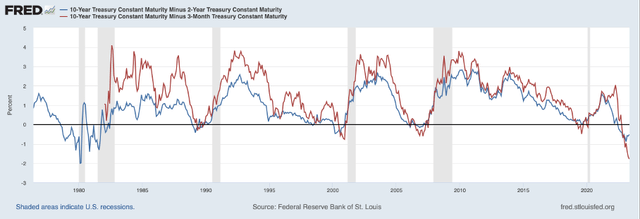

And a third warning indicator – in my opinion, the best one – is the inverted yield curve. In an article explaining several early warning indicators, I wrote:

The yield curve is a line that connects bonds (in our case U.S. treasury bonds) that have equal credit quality but different maturity dates. Usually that line is an upward sloping curve (as bonds with a later maturity date should have a higher interest rate) but when the line is inverted it is indicating trouble for the economy.

And to make it simpler we are looking at two metrics — the 10-year treasury yield minus the 2-year treasury yield as well as the 10-year treasury yield minus the 3-months treasury yield. We simply can watch out for the two metrics falling below zero. And especially the 10-year minus 3-months was an extremely reliable indicator with hardly any false signals since the 1970s.

FRED

And these two are sending (or sent a few months ago) such clear warning signal, it is hard to argue against.

Labor Market

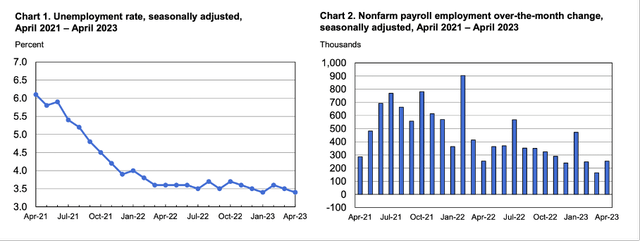

After these early warning indicators have signaled a recession already several months ago, we can move on to numbers reacting with some time delay. The labor market with its many different metrics would belong to that category of time-delayed warning indicators. In fact, many people are often pointing towards the robust labor market to argue against a potential recession. And when looking at the unemployment rate of only 3.4% it is extremely difficult to argue for trouble and a recession ahead.

U.S. Bureau of Labor Statistics

But in case of the labor market, we must look at the right metrics – and the unemployment rate is not the right one as it doesn’t start to take off before the economy is already in a recession (see here for past data). Instead, we can look at the nonfarm payroll employment month-over-month change – and when looking at the data over the past two years we see that the economy is constantly adding a lower number of jobs – but we are still at healthy levels. Additional 100k jobs per months are often seen as the threshold for a healthy economy and we are still above that number.

When looking at the last few recessions, the economy usually was not able to add jobs anymore from the time the recession began. It was not always the same month, but the time when the U.S. economy entered a recession and the time when it was not able to add jobs anymore were in most cases only one or two months apart. Of course, there are exceptions to that rule (1973/74 for example) and with the U.S economy still adding 253k jobs in April the recession could still be several months away (I excluded the COVID-19 recession as the extreme numbers completely messed up the chart).

FRED

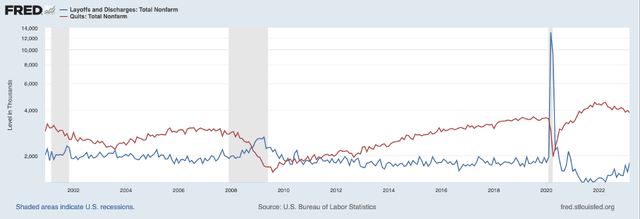

We can look at the nonfarm numbers in more detail – especially at the split between the people quitting and those getting laid off. In a healthy labor market, people are usually quitting their jobs while people start quitting less when the economic situation gets more dire and instead companies start to lay people off.

FRED

When looking at the numbers we already see a trend reversal with layoffs increasing and the number of people quitting getting lower. However, it could also be only a reversion to the mean as both numbers have reached extremes after the COVID-19 crisis.

FRED

And finally, we can look at the initial claims for unemployment insurance. We can see the number constantly increasing over the last few months, which could also be a sign for the labor market turning, but we must be very cautious when interpreting these numbers as the increase is not really dramatic and certainly not enough to make definite statements about a potential recession.

However, if I am right and the United States will enter a recession in 2023, we should see initial claims rising and total nonfarm numbers declining over the next few months. And at some point, the unemployment rate will also start to rise.

FED Pivot

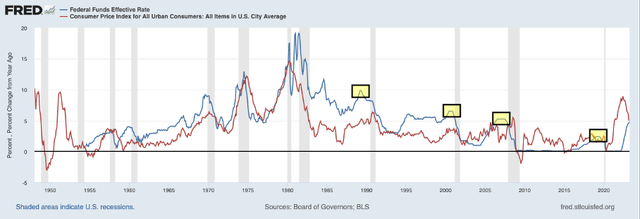

Aside from a labor market getting worse, the FED pivot is a next “necessary” step towards the recession. Of course, it is not necessary but usually happened before the economy enters a recession and usually the FED pivot is not a single turning point, but interest rates are rather plateauing at a high level for several quarters before the FED is starting to lower rates again. Keeping that in mind it might take several more quarters before the United States will enter a recession.

FRED

But here we can make the case that “it might be different this time”. We are at one of the few times in history when inflation was for several years above the federal funds rate and with inflation shooting up in 2021 and 2022, the FED had to fight inflation. And now the FED is caught between bringing inflation down by high interest rates and not crashing the economy by too high interest rates.

The chances are rather high that the FED pivot is actually a pivot point – similar to other times with high inflation and the FED might start cutting rates quickly once they are convinced inflation is more or less under control. Hence, one of the next steps to look for is the FED stopping to raise rates and instead start cutting again.

Purchasing Manager Index

Another indicator that is signaling a recession with a high probability is the U.S. purchasing manager index – especially the non-manufacturing (or service) PMI. The number already dipped below 50 in December 2022 but was above 50 in the following months again. Maybe that single month was a false signal, but usually a non-manufacturing PMI is signaling a recession and for the coming months we should expect that number to decline below 50 again.

Stock Market Crashing

And while the stock market is signaling a recession quite early – by the market usually topping months before the economy enters a recession – it often takes a long time before we see the stock market crash we often remember in hindsight. In case of the Great Financial Crisis, the market made its top in October 2007 but it took until September/October 2008 before panic set in and the stock market sell-off accelerated.

Hence, one of the next signs we must look out for is severe panic among investors. Right now, it is still possible to ignore the risk of a recession (and of course, I might be wrong and there is nothing to ignore). Investors can still point towards a strong labor market, point towards the FED still raising rates or the service PMI still being above 50. But as the bad news will pile up and more and more metrics pointing towards a recession, panic will set in at some point. And at some point, it will become a vicious cycle – that often leads to extreme overreaction (meaning that pessimism will become so extreme that many stocks will trade for prices below the intrinsic value).

So, at some point in the coming months, we should see the stock market crashing. And by crashing, I mean a panic sell-off (like we saw in September and October 2008) with the S&P 500 losing 20% or 30% within a few short weeks.

Banking: Ripple Effects

And although the failure of banks – or even worse: a banking crisis – is not going hand-in hand with every recession, I expect ripple effects in the coming months and in my opinion, we will see more banks failures – however, it remains to be seen if we will experience a similar banking crisis as in 2008 and 2009.

But after a first initial shock in March 2023 (after Signature Bank and Silicon Valley Bank collapsed), the S&P 500 performed quite well in the last few weeks and slowly crawled higher. It seems like confidence returned and many people were positive that the banking crisis was not really a banking crisis, but the banks failures were just a few isolated events (and not a systemic problem).

Howard Marks – who I admire for his detailed and great analysis – argued in a similar way in his last memo “Lessons from Silicon Valley Bank”. After listing some of the reasons why SBV collapsed (mostly huge amounts of cash due to wealthy clients in California and a low demand in loans which made SBV management to purchase bonds at the completely wrong time), he concluded:

The sum of the above rendered SVB particularly vulnerable to a bank run if adverse circumstances developed – and they did. However, many of the above factors were peculiar to SVB. Thus, I don’t think SVB’s failure suggests problems are widespread in the U.S. banking system.

And further down the line, Marks writes:

Looking at the current situation, I can’t think of anything that’s highly analogous to the subprime mortgages at the heart of the GFC. There are things here or there that have been over-hyped or are short on substance – some people will point to SPACs or cryptocurrencies – but they’re not as massive in scale, perhaps not as lacking in substance, and certainly not held on the balance sheets of America’s key financial institutions in amounts sufficient to endanger our financial system. Indeed, I think it’s safe to say the most glaring market excesses were corrected in 2022 and aren’t hanging over us now.

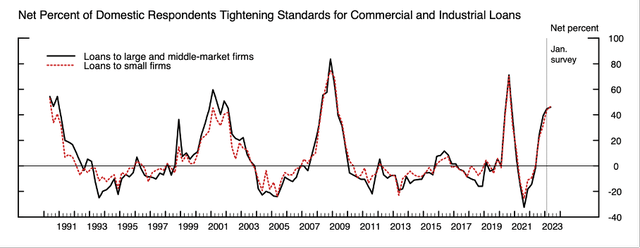

Although I think Mark’s analysis is often spot-on, I think he might be a bit too optimistic here. And despite confidence among investors, we are definitely seeing banks getting much more cautious – for example by tightening lending standards. About 50% of domestic respondents are tightening standards for commercial and industrial loans. And this is a typical pattern we are seeing prior to every recession – at least since the early 1990s (no older data available).

Senior Loan Officer Opinion Survey

And although we don’t have to see failing banks, we will most likely see rising delinquencies in the coming quarters and bank profits will certainly be lower. If more banks will be brought to their knees remains to be seen (but I would not bet on banks being safe).

Conclusion

I am already reading articles, that the bear market will be over soon as it obviously began in December 2021 (or January 2022) and is now lasting almost for 1.5 years, and the average bear market doesn’t last much longer. When talking about bear markets, our mind is often looking at the most recent data we remember – the COVID-19 crash and the Great Financial Crisis. And especially the COVID-19 crash was over after a few weeks. But we must be prepared for a long and painful bear market with the market moving lower over several years.

I personally expect a much steeper decline than the one we have seen so far, but it is also possible that the market will just stagnate at the same level for a long time until earnings and fundamentals are catching up – like it was the case in the 1970s. And looking at average numbers will give us important information, but we also must be prepared for the extremes – and survive these extremes. It is like one of Howard Mark’s favorite sayings:

Never forget the six-foot-tall person who drowned crossing the stream that was five feet deep on average.

Read the full article here