")

Free cash flow stocks were all the rage last year and coming into 2023. Firms that were able to produce profits without accounting gimmicks were gems in a world of quickly rising interest rates. The start of 2023 has been a different story, however. Growth names – not the value style – have performed the best. Energy, Financials, and Industrials equities have suffered on a relative basis to, say, the Nasdaq 100 ETF.

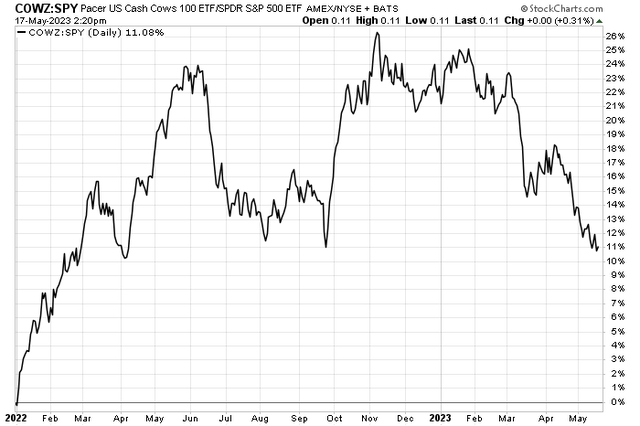

The Pacer US Cash Cows 100 ETF (COWZ) sported impressive alpha last year, but its free-cash-flow focused ETF hovers near 52-week lows versus the S&P 500. One of its largest holdings is an embattled Health Care-sector company.

Pfizer (NYSE:PFE) trades at an attractive 13 times this year’s FCF and the vaccine-maker’s dividend yield is sharply above its 5-year average. Still, poor price action and an uncertain second half lead me to issue a hold recommendation. But I do offer technical guidance on where PFE stock would be a buy.

Free Cash Flow ETF Falls Vs SPX YTD

Stockcharts.com

According to Bank of America Global Research, PFE is a global biopharmaceutical company with a diversified portfolio of products and pipeline candidates. The firm is focused on advancing–discovering, developing, licensing, marketing–drugs for oncology, rare diseases, infection and immunology, infectious diseases, hospital settings, and other indications.

The New York-based $209 billion market cap Pharmaceuticals industry company within the Health Care sector trades at a low 7.3 trailing 12-month GAAP price-to-earnings ratio and pays a high 4.4% dividend yield, according to The Wall Street Journal.

Shares have been under pressure for a host of reasons, but recent news that the firm would have to float a large $31 billion debt amount to finance the acquisition of Seagen (SGEN) is not seen as favorable to its balance sheet considering today’s higher interest rates versus past years. While the M&A move aims at inorganic growth opportunities, the concern is that it is not all that shareholder friendly.

Its organic growth prospects remain murky and bearish sentiment is high. Even after reporting better-than-expecting Q1 earnings estimates with a strong COVID franchise, investors quickly look past the waning pandemic and forward to uncertainty. While its Paxlovid sales were very strong, that could perhaps be attributed to China COVID cases that spike last quarter.

In the second half, Prevnar and RSV will be a pair of major launches to monitor. A longer-term problem for PFE is that its pipeline may have holes since patent loss of exclusivities (LOEs) begin to mount in 2025, potentially leading to billions of lost sales.

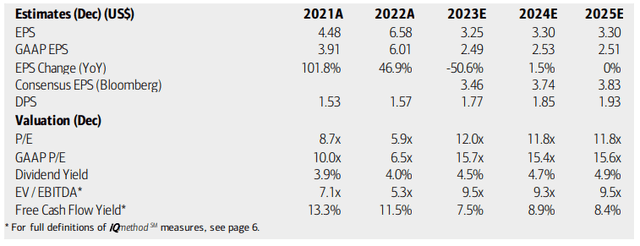

On valuation, analysts at BofA see earnings falling sharply from 2022’s abnormally high per-share profit total. Nero-zero percent annual bottom-line growth is expected over the coming quarters as EPS normalizes. The Bloomberg consensus forecast is a bit more sanguine, though. Dividends, meanwhile, are seen as rising steadily amid ample free cash flow despite soft profit growth.

PFE’s P/Es are attractive at a high level, but with uncertainty regarding activities in the second half and over the long haul, paying 16x GAAP EPS is not all that cheap. Still, income investors can point to a yield that is more than 20% above Pfizer’s 5-year average of 3.6%. A free cash flow cow, the valuation is not entirely poor, though.

Pfizer: Earnings, Valuation, Dividend Yield, Free Cash Flow Forecasts

BofA Global Research

Based on the low growth outlook, I would value shares no more than 10x operating earnings. Assuming normalized EPS of $3.50 over the coming 12 months, that would make it a $35 stock – just slightly above where it trades today.

PFE: Weak Growth Ahead Challenges Strong Valuation Measures

Seeking Alpha

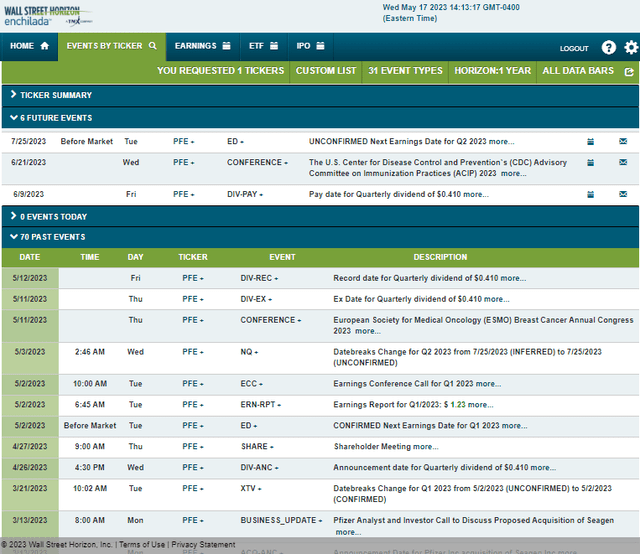

Looking ahead, corporate event data provided by Wall Street Horizon show an upcoming conference speaking engagement on June 21-22 at The U.S. Center for Disease Control and Prevention’s (CDC) Advisory Committee on Immunization Practices (ACIP) 2023. The following volatility catalysts come on July 25 when the Health Care firm has its unconfirmed Q2 2023 earnings date.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

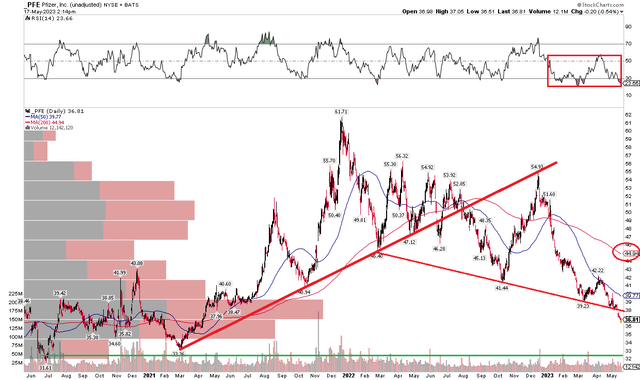

PFE has been an utter disaster ever since the breakout of the COVID omicron variant in late 2021. Over the last 15 months, shares are in a stunning 40% drawdown. Lately, the stock has taken an accelerated downside move. Notice in the chart below that PFE is sliding toward its old 2020-early 2021 range where we find an ample amount of volume by price. What’s more, the $32 to $33 range should offer some support – those were the range lows where buyers stepped to the plate many quarters ago. Buying there with a stop under $30 is a favorable risk/reward play.

Also take a look at other bearish near-term indicators. First, the RSI momentum reading at the top of the chart shows a classic negative picture. The 20 to 60 zone is often where downtrends see RSI range within. Moreover, the 200-day moving average is sloping downward while the short-term 50-day is under the longer-term trend indicator. Following the uptrend break during the middle of last year and with a move under a support line just this month, I see more downside ahead. But we are nearing a buy point technically.

PFE: Bearish Downtrend, Support Seen In the Low $30s

Stockcharts.com

The Bottom Line

I am a hold on PFE. Shares are near fair value in my estimation while the chart is more bearish with support not far below the current stock price.

Read the full article here