…")

Wall of Worry

On Tuesday I put out a summary of Bank of America’s May Global Fund Manager Survey:

Here were the key points that suggest continued upside for the markets in coming months:

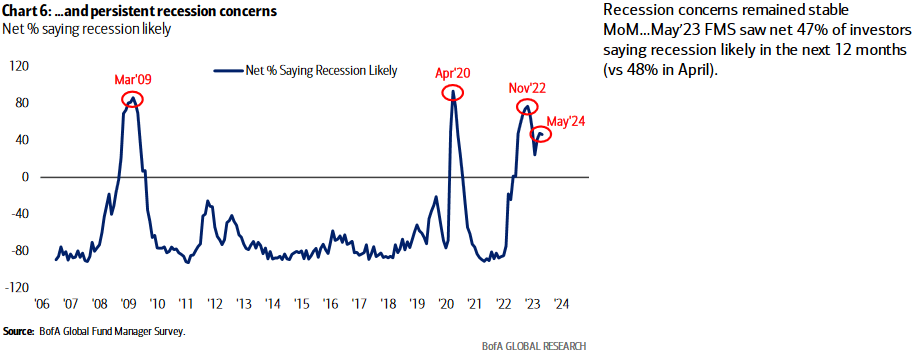

1) By the time “recession concerns” have started rolling over, the bottom in equity markets is well in the rear view mirror:

BofA Global Fund Manager Survey

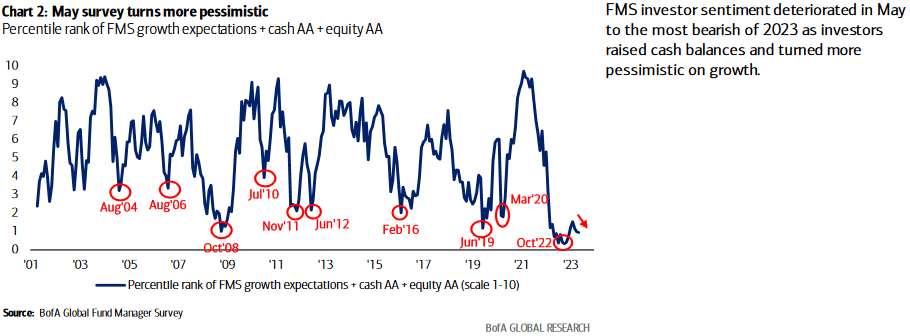

2) The bottom in pessimism is in and resembles the mini “check back” in 1Q 2009 and 2016 when the market had already bottomed:

BofA Global Fund Manager Survey

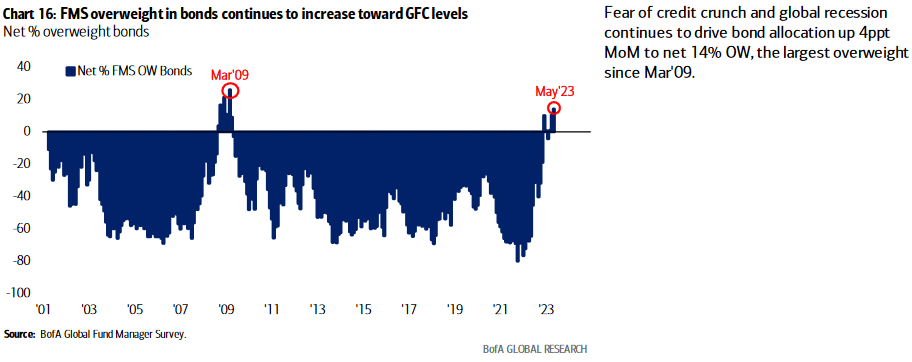

3) Managers are the most overweight bonds relative to stacks since the GFC lows in March 2009. BAD TIME TO BE OUT OF EQUITIES.

BofA Global Fund Manager Survey

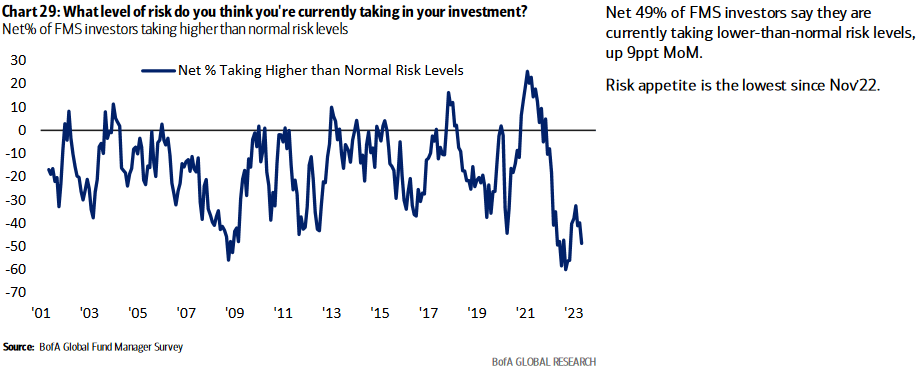

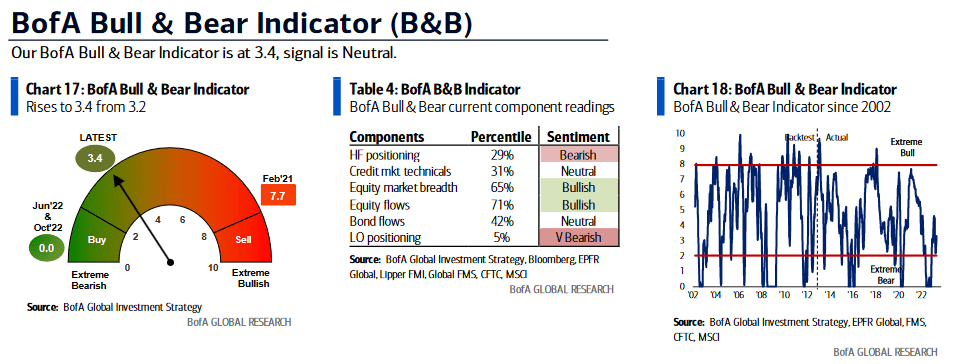

4) Managers are as scared to take risk today as they were at the March 2009 GFC lows:

BofA Global Fund Manager Survey

OTHER INDICATIONS:

BofA Global Research

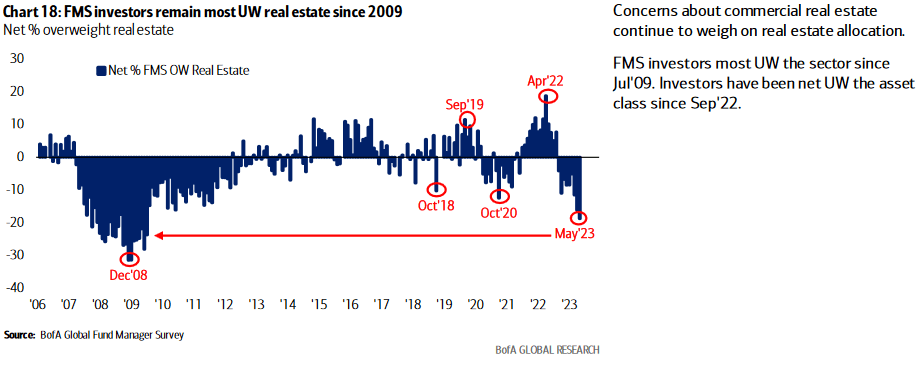

Selling in REITS should be nearing an end:

BofA Global Investment Strategy

BofA Global Fund Manager Survey

As we’ve repeatedly said, “the last shall be first.” Expect REITS (which was the worst performer last year) to work its way back up to the top in the next 12-24 months as the Fed is finished hiking:

BofA Global Investment Strategy

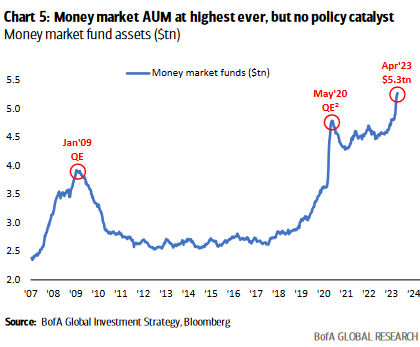

Markets don’t top when everyone is in cash:

BofA Global Investment Strategy

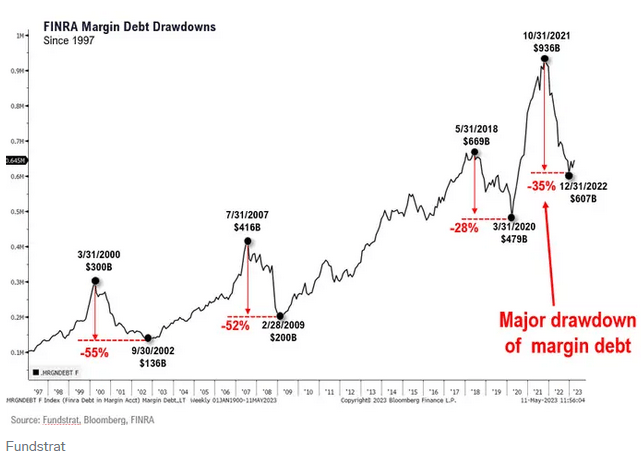

Markets top when everyone is overweight stocks on margin. We are nowhere close to that point:

Fundstrat

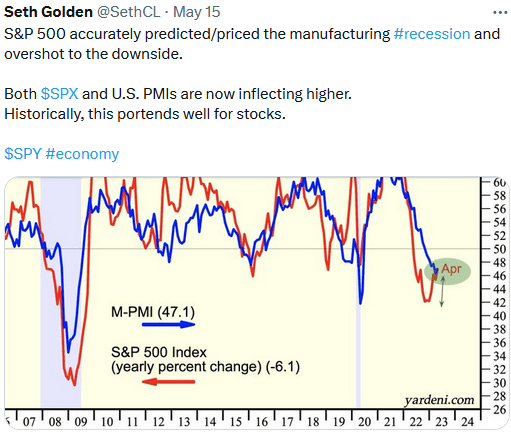

Seth Golden

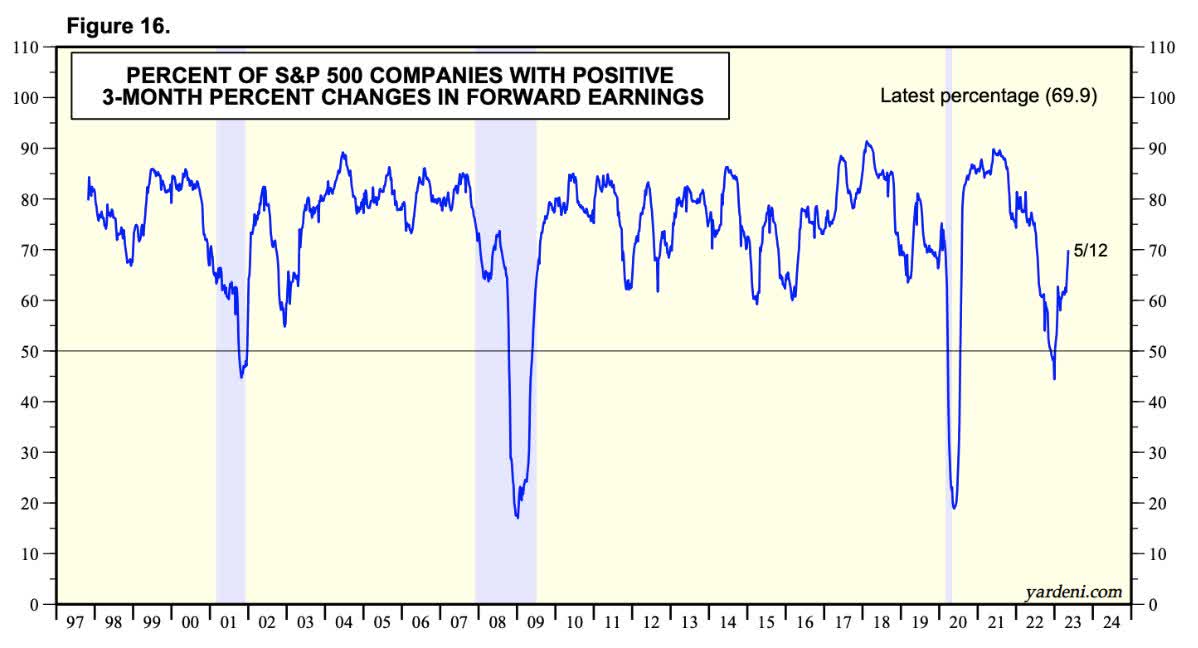

More Positive Earnings Guidance

Yardeni

Cooper Standard

While the stock is up almost 100% since our initial purchases last May, there is a lot more room to run.

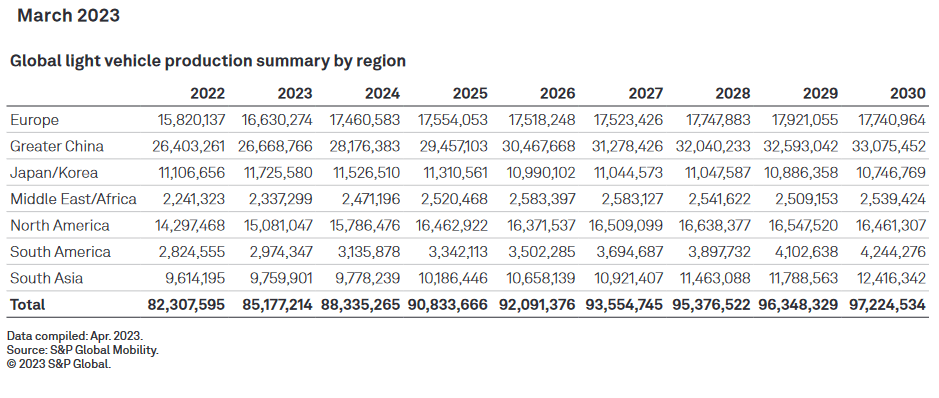

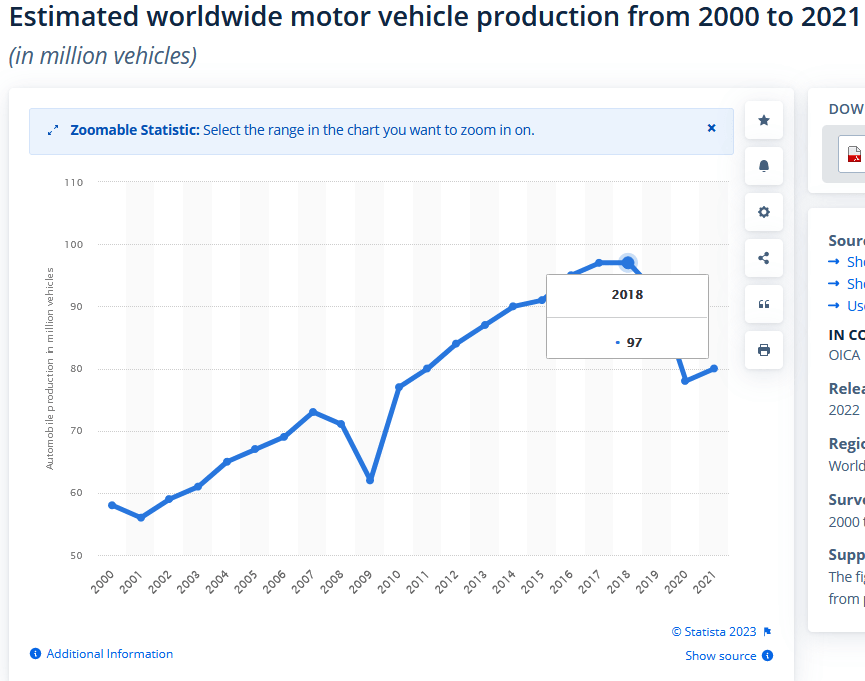

The pandemic aberration is over. In 2017 Global Light Vehicle Production was 97MM. Cooper Standard earned over $7 per share and traded at $140 (~20x). Remember when despondency turns back to euphoria you get multiple expansion. According to S&P (below) we won’t hit 97M, but we don’t have to. North America is already tracking higher than this estimate for 2023. At 90M the company can earn >$7/share again because costs have been gutted and margins are higher on EV which is becoming an increasing share of mix. Haircut it and we’re out around $60-$120/share blended (some lower, some higher). (opinion, not advice – see terms).

S&P Global Mobility

Satista

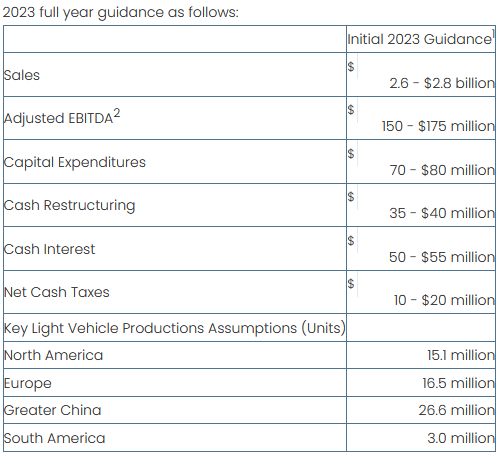

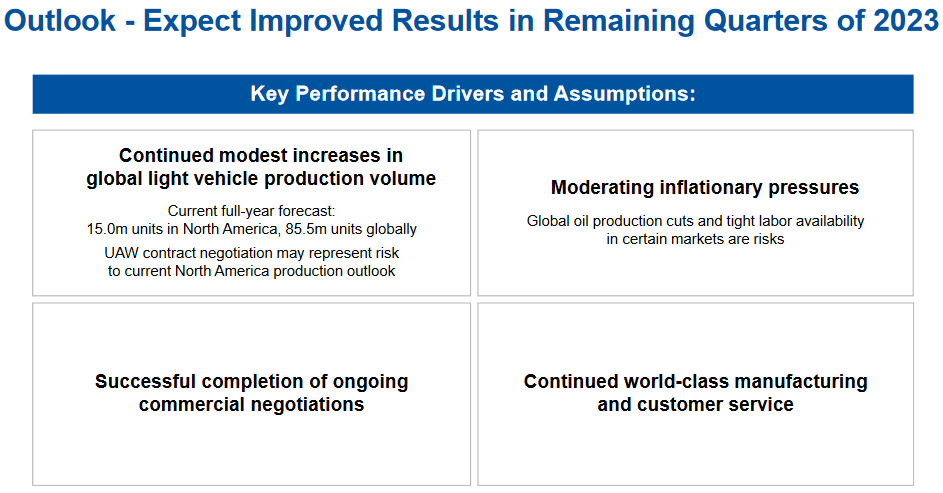

2023 Guidance still tracking:

Cooper Standard IR

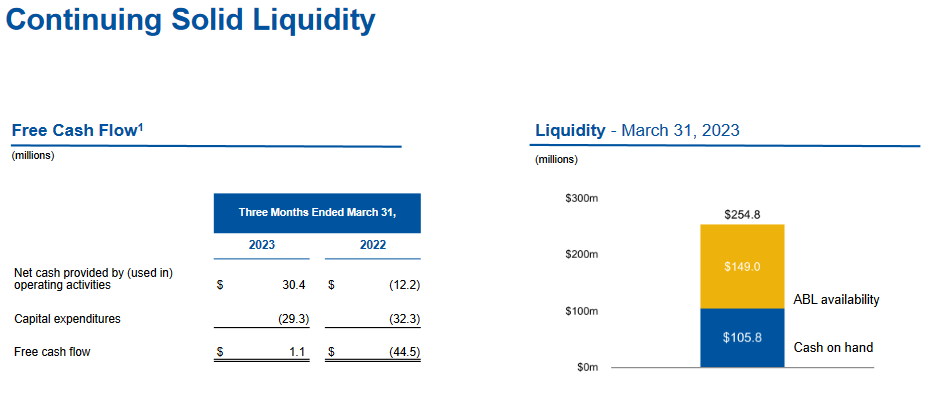

Cooper Standard IR

Cooper Standard IR

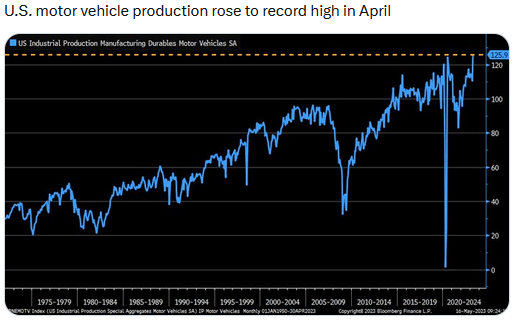

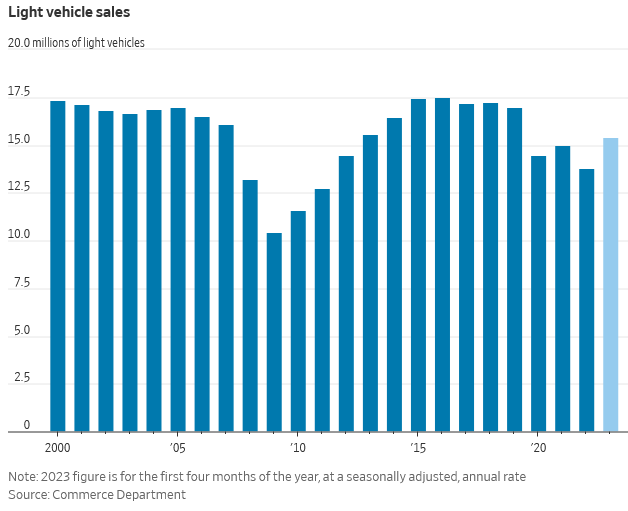

Updated Data Since earnings:

Bloomberg Finance L.P.

Commerce Department

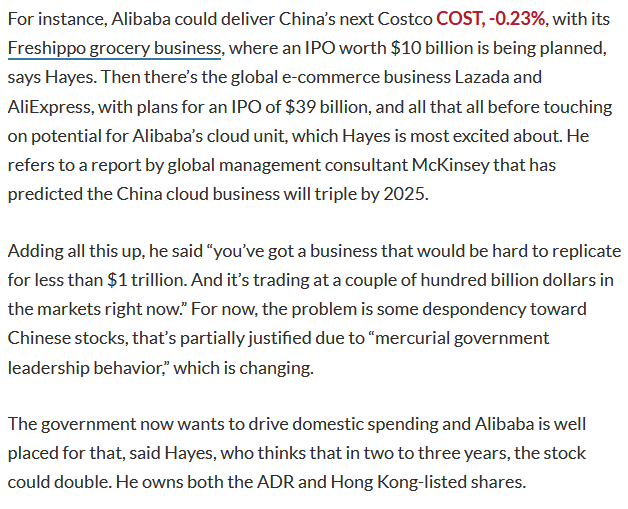

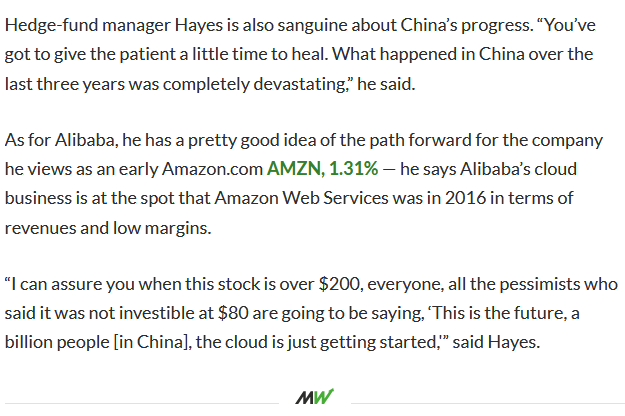

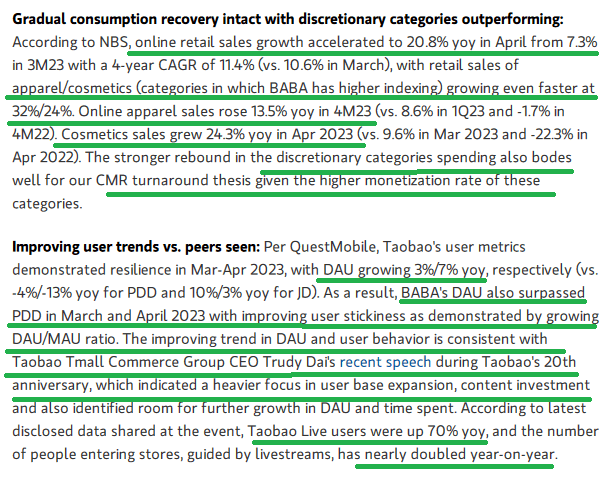

Alibaba

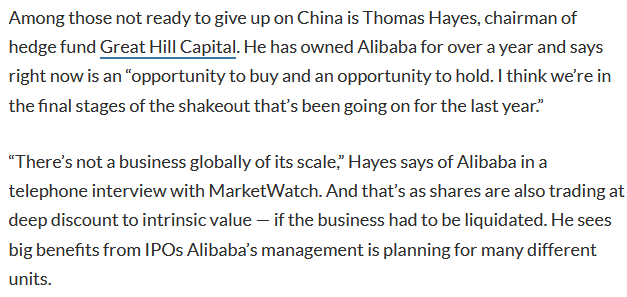

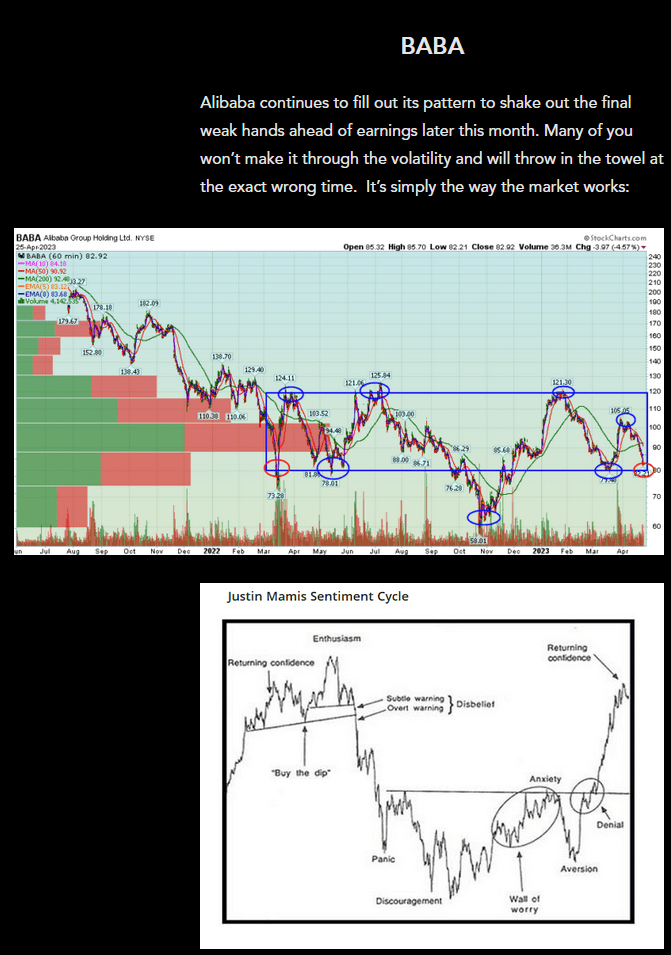

We presented our “sum of the parts” analysis in last week’s note. We laid out how the pieces can add up to ~$300/share (and more) over time. Yesterday, Barbara Kollmeyer interviewed me for her MarketWatch article. Here were my key points:

MarketWatch

MarketWatch

MarketWatch

The article above may prove to be as important as the last major feature I had on MarketWatch on March 19, 2020 when we called the pandemic stock market bottom (to the day).

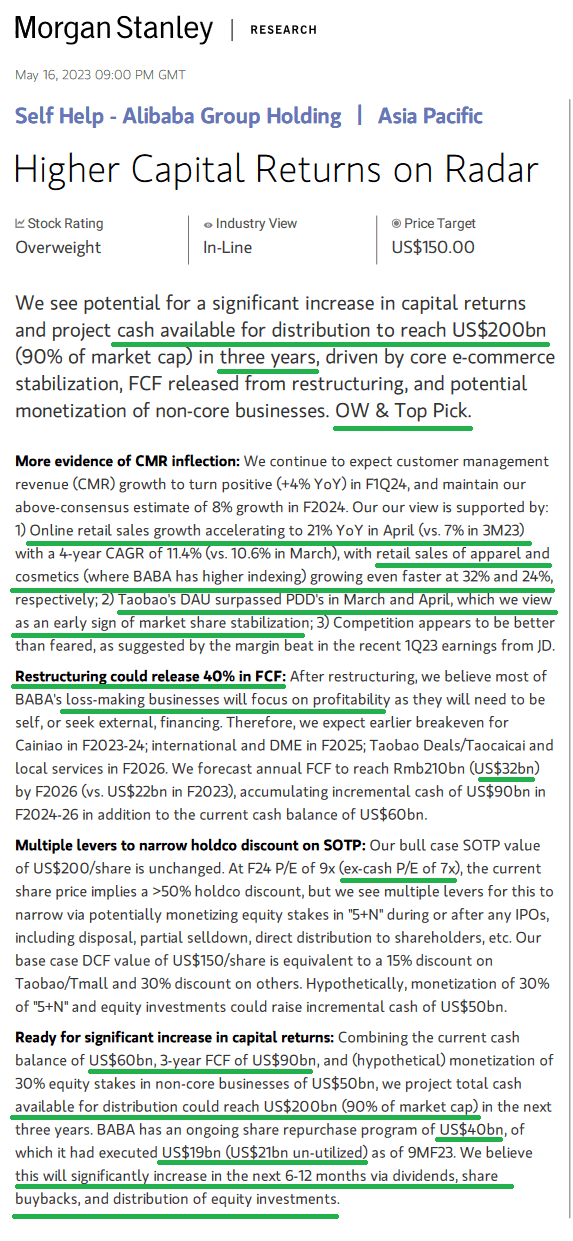

It seems Morgan Stanley agrees as the cash BABA has on hand, plus the free cashflow they can generate over the next 3-4 years is sufficient to buy back 100% of the shares over that period!

We may be the last shareholder standing with a business generating >$30B/year in free cash-flow after all of the float is bought in!!!

Morgan Stanley

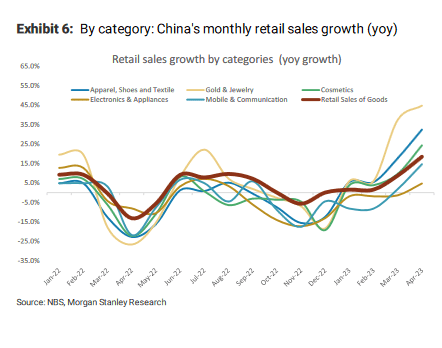

NBS, Morgan Stanley Research

Morgan Stanley

Remember this from our article 2 weeks ago:

HedgeFundTips

Biotech

We’ve covered all of the valuation catalysts and fundamental catalysts for the biotech sector in previous articles and podcast|videocasts.

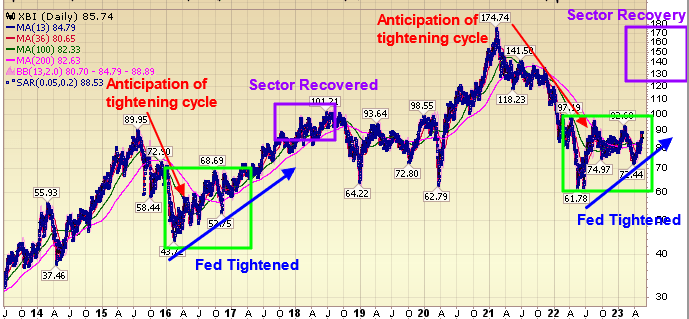

Ultimately, Biotech is just a Fed trade like 2016 – 2018. Sector crashed anticipating tightening cycle; Fed tightened; basket went up; end of story. Same will happen (is happening) this time:

Tom Hayes via Stockcharts

Now onto the shorter term view for the General Market

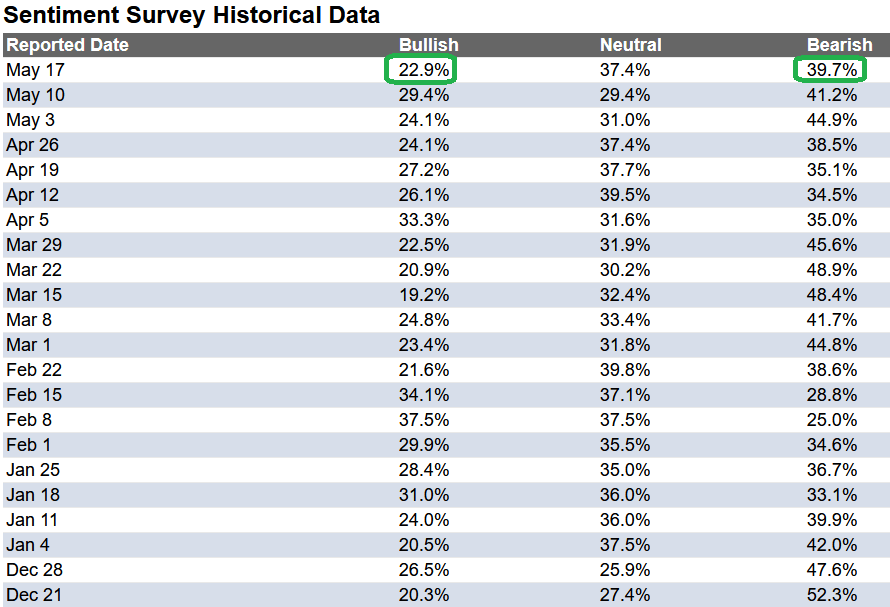

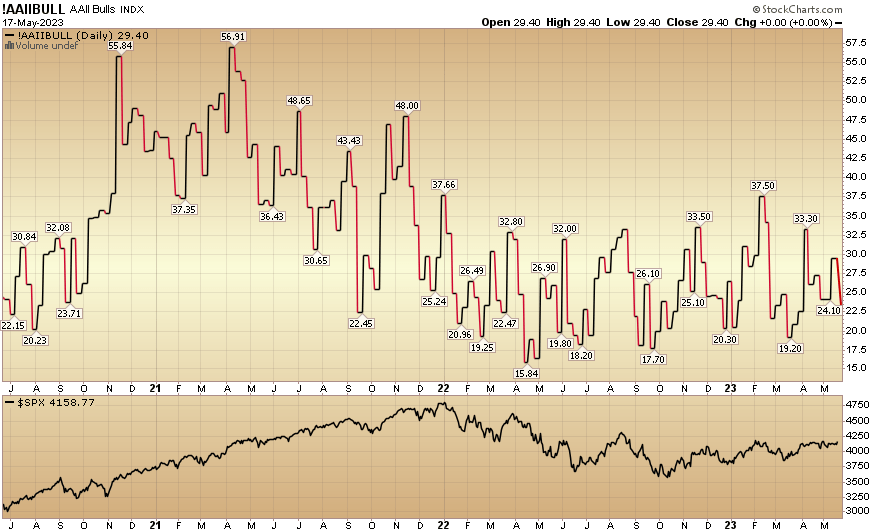

In this week’s AAII Sentiment Survey result, Bullish Percent dropped to 22.9% from 29.4% the previous week. Bearish Percent moderated to 39.7% from 41.2%. The retail investor is extremely fearful.

AAII.com

Stockcharts

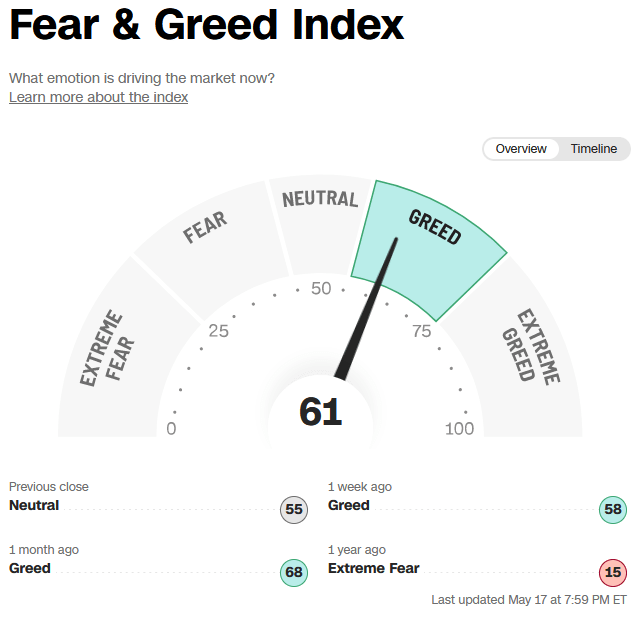

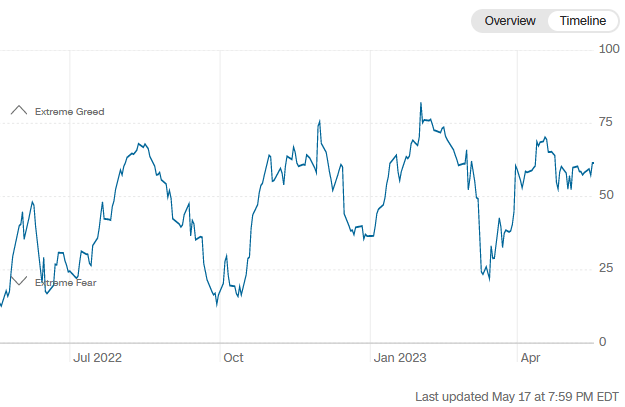

The CNN “Fear and Greed” ticked up from 60 last week to 61 this week. Sentiment is moving up.

CNN

CNN

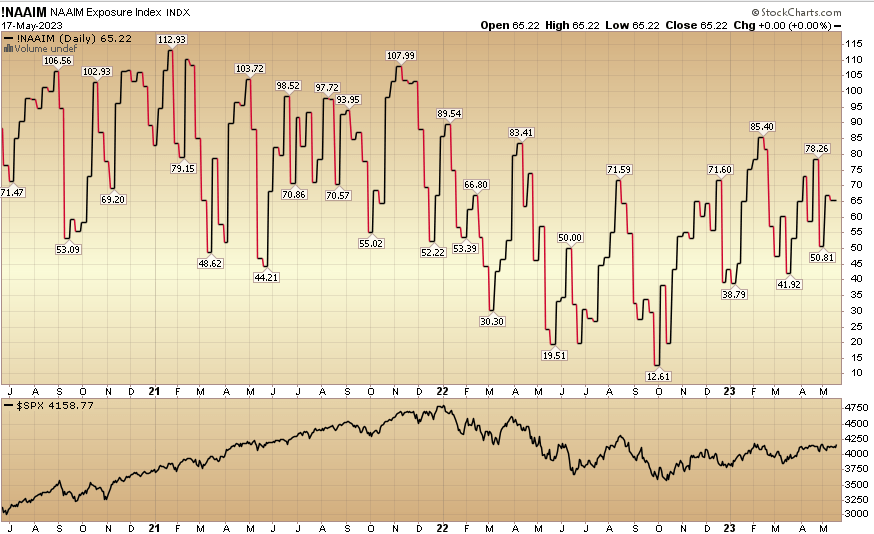

And finally, the NAAIM (National Association of Active Investment Managers Index) ticked down to 65.22% this week from 67.01% equity exposure last week.

Stockcharts

*Opinion, not advice. See “terms” at hedgefundtips.com.

Read the full article here