Over the last month, ANSYS (NASDAQ:ANSS) stock saw a massive jump of around 25% after The Wall Street Journal reported that Synopsys (SNPS) is in talks to merge with the company. Since then, Synopsys stock dropped by over 10%. Cadence Design Systems (CDNS) was also cited as a potential suitor for the company. Sources said, “the offers ANSYS attracted value it well over $400 per share”. ANSYS is currently trading at about $350 a share. The question is, is the market overreacting to this potential merger, or is it still a good time to enter?

A Little About the Industry

ANSYS specializes in developing engineering simulation software that is widely used around the world. Its simulation is used in a variety of industries from aerospace to healthcare to 5G to chip design. These simulations are valuable to engineers for increasing performance, reducing design cycle time, and reducing R&D costs.

ANSYS

The simulation software market size is expected to increase at a fast pace of 13.1% CAGR from 2023-2028. Simulation is a needed feature in many industries, in fact, the report finds that one of the biggest constraints to the growth of market size is the number of experts familiar with the software readily available. Most importantly, ANSYS works with a subscription model, which will generate a lot of revenue just from the recurring customers.

On the other hand, Synopsys is an industry leader in electronic design for the semiconductor and electronics industry. It specializes in providing semiconductor design solutions and IP integration, which basically means to integrate pre-designed modules onto a SoC (System on a chip).

Cadence also very much competes in the same market as Synopsys, specializing in PCB designs. Its market capitalization in this industry is only second to Synopsys, with a value of $70 billion, compared to Synopsys’ $75 billion.

The EDA (Electronic Design Automation) market is expected to climb at a CAGR of 9.1% from 2023 to 2030. A key factor to watch is the integration of AI and ML into the design software, as it can massively increase the efficiency of the designing process.

ANSYS Financial Health and Evaluation

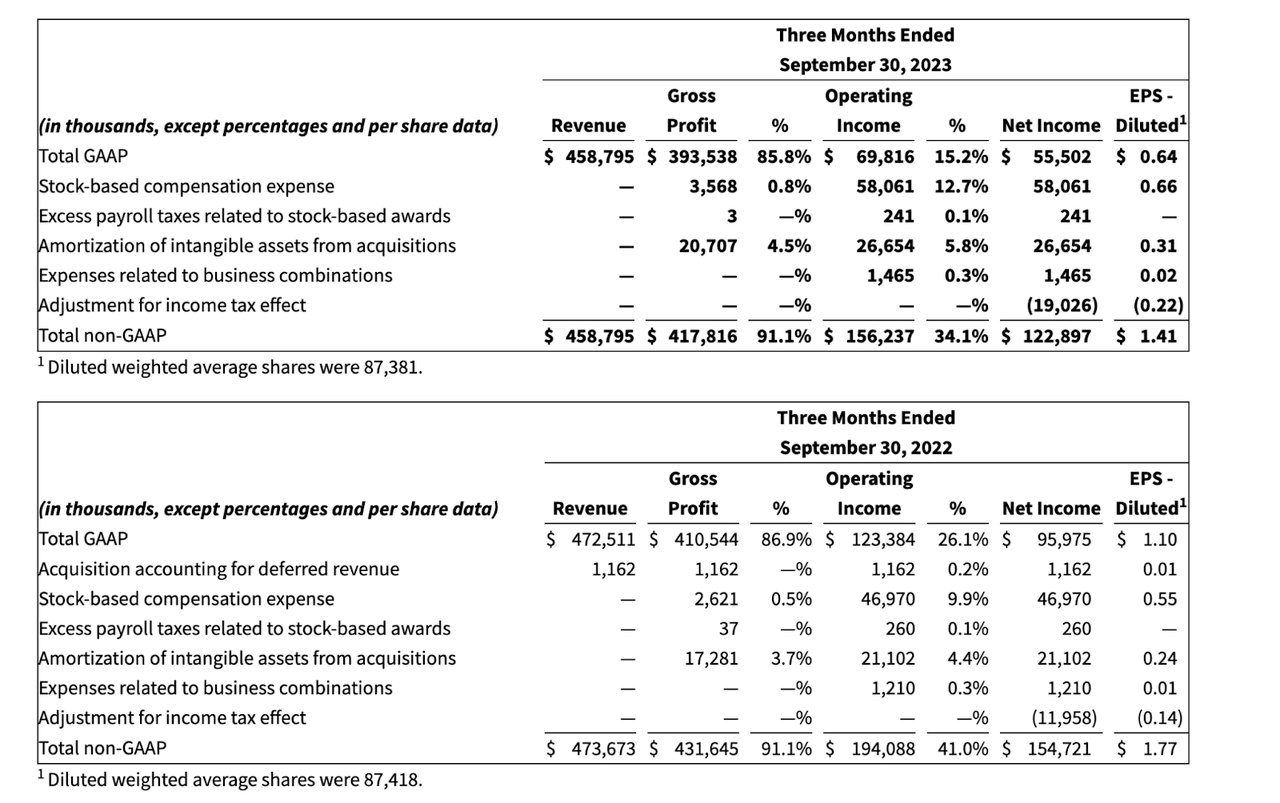

Now, let’s ignore the merger talk and seek a fair valuation for ANSYS. Over a year ago, I evaluated ANSYS at $255, but the market and the economy have changed since then. In the most recent Q3 2023 earnings report, ANSYS’ GAAP and non-GAAP revenue for Q3 2023 was $458.8 million, which is a 3% decrease in reported currency or a 4% decrease in constant currency compared to Q3 2022. ANSYS’ GAAP and non-GAAP diluted earnings per share for Q3 2023 were $0.64 and $1.41, respectively, compared to $1.10 and $1.77 for Q3 2022. However, ANSYS’ annual contract value (ACV) for Q3 2023 saw a growth of 12% in reported currency. ANSYS’ Q3 2023 results were negatively impacted by incremental approval processes and export restrictions, including additional restrictions on sales to certain Chinese entities, which created a $20 million headwind to ACV and revenue that was not contemplated in the third quarter guidance provided in August. For its balance sheet, the company’s cash and short-term investment saw an increase YoY from $614.5 million to $639.5 million. At the same time, its long-term debt saw a minor increase from $753.5 million to $753.8 million YoY.

ANSYS

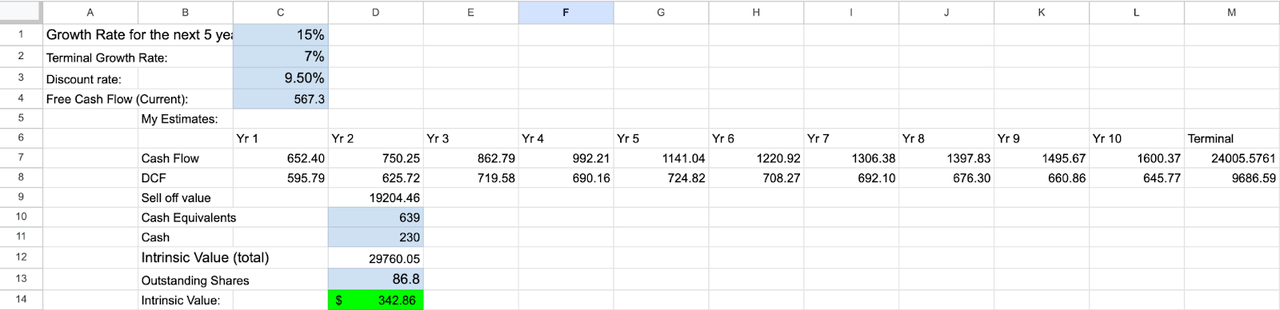

This was quite good news for the company, as its revenue and earnings stayed relatively stable even amidst a rough political climate. In fact, its earnings still beat Wall Street estimates by 11%. The strong growth in ACV demonstrates that the company has a strong and loyal customer base, and can greatly help improve profitability and reduce customer acquisition costs. The company is clearly heading in the right direction and its cash flow reflects it. Comparing Q3 for 2023 and 2022, ANSYS saw an operating cash flow increase from $127.2 million to $160.8 million. The company’s cash flow is growing at a faster pace than I used for my previous DCF evaluation, so my new evaluation is going to take this new knowledge into account.

Author’s own Calculations (Sheets)

Once again, when using an assumed 12x terminal value like I did last time, I also increased the growth rate to be slightly higher than the expected CAGR for the market. And an interesting conclusion is reached – the company has grown into its intrinsic value. Quite curiously, I believe ANSYS is now properly valued.

Plausibility of a merger and why I think it won’t happen

So an ANSYS merger is in the talk, who will come on top? I think no one. First of all, between Cadence Design Systems and Synopsys, it is Synopsys who is much more likely to merge with ANSYS. In addition to its greater market capitalization, ANSYS and Synopsys have already been collaborating for years up to this point. While the two companies don’t directly compete in the same market, I believe many of ANSYS’ simulations and physics can greatly enhance the calculations used in Synopsys’s software. At the same time, Cadence is a direct competitor to Synopsys, so there is little chance it will merge with ANSYS.

For Synopsys, merging with ANSYS would mean not only enhancing its simulation proficiency, but also reaching into completely new markets that ANSYS is a part of.

While this all sounds great, ANSYS currently already has a market cap of $30 billion, so the price of the merger could possibly go up to $40 billion. Synopsys is only worth $70 billion. So using the stock-for-stock merger method, I believe the company stock could be expected to fall a lot. When a merger happens, the market cap just doesn’t simply add together. It would not be surprising if the market cap barely changed and the only thing that changed was the number of outstanding shares. Issuing and distributing over half the number of its existing shares is just not a smart move for any company and would be really bad for its investors in my opinion. We’re talking about potential financial troubles for the company that may take over a decade to recover. In addition, this deal would not easily be done as 2 competing companies are in the potential merger talk. Even if one company gets the merger deal, the other company would likely not let it come out unscathed in my view. In the end, I think both parties will realize a merger would not make much financial sense.

Conclusion

In my opinion, while the public is overreacting to the merger rumors, ANSYS stock has actually grown to its intrinsic value. I do not think either Cadence or Synopsys will merge with ANSYS. Thus, ANSYS stock, at the current moment, is a hold.

Read the full article here