")

Shares of Ardelyx (NASDAQ:ARDX) took a hit last week after the company said it will not apply to include Xphozah in the Centers for Medicare & Medicaid Services (‘CMS’) End-Stage Renal Disease (‘ESRD’) Prospective Payment System (‘PPS’) Transitional Drug Add-On Payment Adjustment (‘TDAPA’), in an effort to preserve patient access to the drug. This effectively means CMS will not cover Xphozah in 2025, and the drug’s future is highly uncertain.

After last week’s decision not to file for TDAPA, Xphozah’s coverage and commercial success now largely depend on legislative efforts – there is a bipartisan bill that can provide a lifeline for the drug, but it will effectively be kicking the can down the road and I am doubtful a product with only two years of guaranteed coverage and high uncertainty thereafter will get the recognition it might otherwise deserve.

This puts more pressure on Ibsrela, which has the same active ingredient (tenapanor), but is approved for the treatment of irritable bowel syndrome with constipation (‘IBS-C’).

Difficult position for Xphozah with Ardelyx leaning on legislation to gain favorable coverage

There is always some drama around Xphozah. It was approved for the treatment of hyperphosphatemia in adults with chronic kidney disease only after a third attempt in October 2023 and more than three years after the first NDA submission in June 2020. Its label limits the use to patients who have “inadequate response to phosphate binders or who are intolerant of any dose of phosphate binder therapy.”

And just as Xphozah received FDA approval and generated decent demand in the first two quarters on the market, there was another setback last week as Ardelyx decided not to file for TDAPA for 2025. The company analyzed the situation and concluded that Medicare coverage from 2025 would have too many restrictions that will “effectively eliminate access to all patients” and management said that not filing for TDAPA would enable them to explore other options to enable better access to Xphozah.

TDAPA refers to payments from CMS after a new drug is added to the dialysis bundle, and means that each dialysis treatment gets a fixed payment regardless of services provided and drugs used during that treatment. Ardelyx believes that Xphozah’s inclusion in the bundle does not provide adequate economics and that it is unlikely to be profitable for the company.

The company did not say how adverse the effects would be in 2025, but this does not sound good, and my baseline assumption would be that sales would materially decline if the situation stays as is since 55-60% of Xphozah’s sales came from Medicare in the first quarter of 2024. Management also said that applying for TDAPA would adversely impact all coverage of Xphozah, not just Medicare.

However, all is not lost. Ardelyx is now relying on legislative efforts that would extend Xphozah’s coverage outside of the bundle. The good news is that the legislative effort is bipartisan – Managed Healthcare Executive reported that the Kidney PATIENT Act passed 41-1 in the Ways and Means Committee in March 2024, and it would allow Xphozah’s coverage outside the bundle until 2027. This is not a long-term solution, but would provide two more years of decent to significant Xphozah revenues, and the time for the company to try and find a permanent solution. Managed Healthcare Executive also says that there is another version of the bill that would extend coverage through 2033 and this is the blue-sky scenario for Xphozah.

The legislative effort looks genuine, but there are no guarantees and I believe a long-term solution is required for Ardelyx to get proper credit for Xphozah.

The launch to date looks good. Xphozah generated $2.5 million in net sales in the last two months of 2023, and $15.2 million in the first quarter of 2024. The early signs of demand are solid and there appears to be more demand than was initially expected. Given expectations for Ibsrela for 2024 to generate $140-150 million in net sales, it appears analysts are expecting approximately $90-100 million in Xphozah net sales this year since the Street consensus is $242 million. Based on the Q1 numbers, I believe this is achievable, but it will not mean much if there is no proper coverage in 2025 and beyond.

Ibsrela – a more reliable growth driver and anchor of investment thesis amid Xphozah’s uncertain outlook

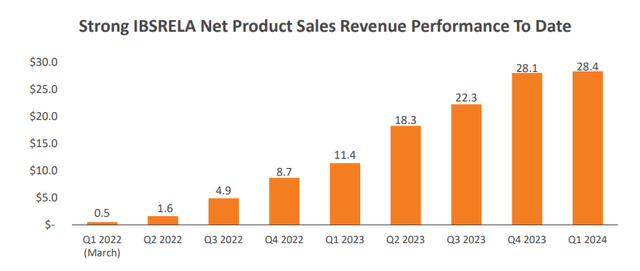

Xphozah’s uncertain outlook puts more pressure on Ibsrela to perform. And at current levels, Ardelyx looks like a decent long based on Ibsrela’s potential in IBS-C. The launch is off to a strong start and management guided for 2024 net sales in the $140-150 million range.

Sales in the first quarter of the year were flat sequentially at $28.4 million, but this reflects the usual seasonal headwinds at the start of the year that create some demand disruption (insurance resets and plan changes, holidays), and the associated lower net price compared to the other three quarters of the year – the gross to net discount was 33.5% in the first quarter compared to 21% in the fourth quarter of 2023. I expect a strong sequential recovery in the second quarter and good momentum in the second half of the year.

Ardelyx investor presentation

There is also potential for growth acceleration driven by the sales force expansion. The company recently expanded the number of covered territories from 64 to 124. Management sounded happy about the strong response to job postings and the talent they attracted and the full deployment of the expanded sales force was expected around the end of the second quarter.

Based on Ibsrela’s performance to date and the sales force expansion, I expect the company to exceed the high end of the $140-150 million guidance range.

IBS-C is a big market and there is certainly room for significant growth in the following years. Ardelyx expects Ibsrela to generate more than $1 billion in annual peak sales by the end of its patent life and this would be achieved by the product reaching 10% market share. The performance since launch is certainly pointing in the right direction.

Valuation and upside potential

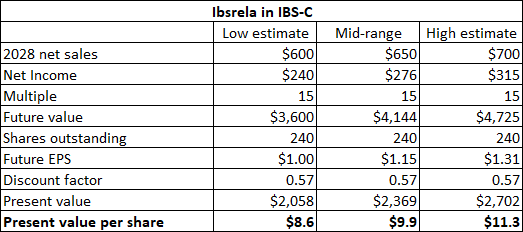

Ardelyx looks attractively valued at current levels based on Ibsrela alone. I am valuing this asset in the $8.5 to $11 per share range based on 2028 net sales reaching $600 million at the low end and $700 million at the high end of the range. I should note that there are some remaining obligations to AstraZeneca in terms of percentage of net sales on tenapanor as a whole (including Xphozah), but this is not a significant amount – as of the end of the first quarter, the remaining obligation was $42.6 million which should not have a significant impact on Ardelyx’s profits or Ibsrela’s in the long run.

Author’s estimates

Xphozah is the hard part in terms of estimating its contribution to the valuation. Under the assumption of appropriate long-term coverage, it’s value and peak sales potential could approach Ibsrela’s in the long run.

However, if there is no reliable long-term coverage, I believe it is not appropriate to assign a full valuation to Xphozah. Even if it gets an extension through legislative efforts, I doubt Ardelyx will get the full long-term recognition. And since its long-term future depends on the will of politicians, I would not venture even to estimate the probability of Xphozah gaining long-term coverage. I also cannot with any degree of confidence estimate what Xphozah’s sales look like without Medicare coverage.

The good news is that we can treat this as upside optionality since I see the stock as good value based on Ibsrela, and then start to worry about further upside potential if and when the stock enters double-digit share price territory.

I should note that my Ibsrela estimates include modest to negligible contribution from ex-U.S. territories, which offer some additional upside optionality in the long run, because I want to see real traction outside the U.S.

Financial overview

Ardelyx had $202.6 million in cash and equivalents at the end of the first quarter, and this figure includes the proceeds from the term loan agreement with SLR Capital, which brought the total amount owed to $100 million. The company also has the option to draw another $50 million under the loan agreement.

With rapidly growing revenues and cash expenses likely in the $60 million a quarter range going forward, I believe Ardelyx is in good financial shape regardless of Xphozah’s outlook as I expect Ibsrela will likely bring the company to cash flow breakeven by the second half of 2025, and sooner if there are meaningful Xphozah revenues.

Risks

While I believe the risk-reward is skewed to the reward side after the latest selloff, the path forward for Ardelyx is not without risks:

- The main risk at current levels is Ibsrela underperforming sales expectations. Ibsrela could underperform expectations due to a variety of factors, such as adverse changes to patient access and increased competition.

- Expectations around Xphozah may be low right now, but negative updates could once again put pressure on Ardelyx’s share price even if the current perception is that there is little to no value assigned to Xphozah.

Conclusion

The lack of coverage for Xphozah in 2025 and beyond would be a major setback for Ardelyx in terms of long-term upside potential, but all is not lost as there is a genuine legislative effort to bring coverage back for another two years and provide time to find a long-term solution.

I see the stock as well positioned to deliver shareholder value from current levels with Ibsrela alone, and significantly more if there is long-term coverage of Xphozah. The focus in the near-term will go back to commercial performance of Ibsrela and Xphozah and will switch back to legislative updates on Xphozah later in 2024.

Read the full article here