")

By Scott Kennedy; Produced with Colorado Wealth Management Fund.

Commentary

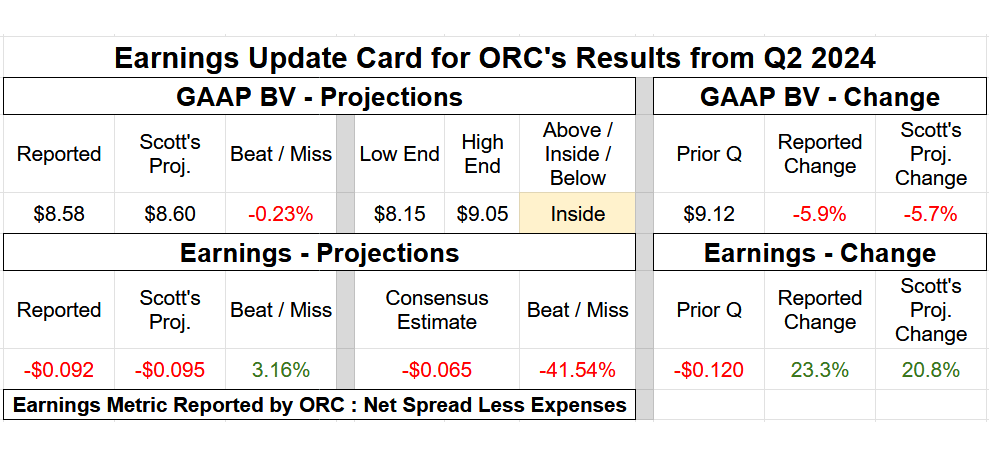

- Quarterly BV Fluctuation: Basically an Exact Match (Only a 0.2% Variance).

- Net Spread Less Operational Expenses (Core Earnings/EAD Equivalent): Basically an Exact Match (Only a $0.003 Variance).

An “as expected” quarter on both metrics for Orchid Island Capital, Inc. (NYSE:ORC) in my opinion. That said, some market participants could be disappointed by ORC’s modest quarterly BV loss. This was something I correctly anticipated as agency MBS spreads widened in late June 2024, which negatively impacted sector BVs going into quarter-end. As correction anticipated within our weekly mREIT and BDC newsletter, this spread widening has partially abated during early July 2024. While still modestly negative, ORC’s core earnings equivalent metric continued to slightly improve, which could be considered a bit of a “silver lining.”

ORC’s modest BV decrease and core earnings equivalent loss mainly stemmed from a similar amount of MBS valuation losses offset by derivative valuation gains and continued weak (though slightly improving) net interest income and higher operational expenses from a larger capital base, respectively. ORC’s minor quarterly CPR increase was as anticipated, as the company continued to “move up the ladder” per se regarding investing in some new production/higher coupons (which inherently have higher prepayment rates versus lower coupons).

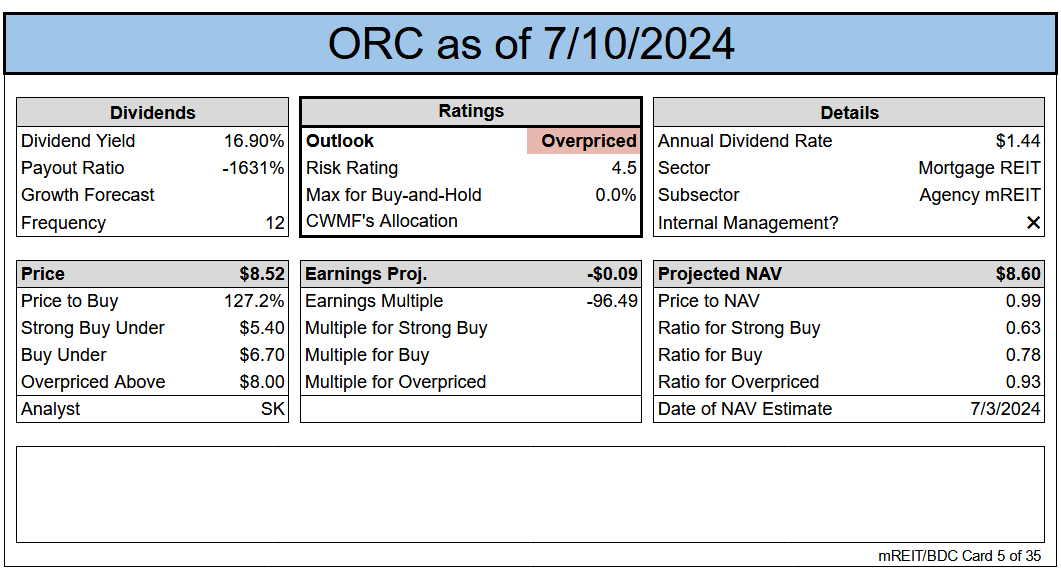

A risk/performance rating of 4.5 for ORC remains appropriate in the current environment/over the foreseeable future (“higher-for-longer” regarding rates/yields during 2024). That said, remember, my/our models are already projecting 1-2 Federal (“Fed”) Funds Rate cuts later this year – early next year, so that is also already “baked” into sector price targets.

We will use many terms in this article that may be unfamiliar to readers. We’ve created a glossary for those that are interested.

Change or Maintain

- BV/NAV Adjustment (BV/NAV Used Interchangeably): Our projection for current BV/NAV per share was adjusted: Unchanged (To Account for the Actual 6/30/2024 BV/NAV Vs. Prior Projection). Price targets have already been adjusted to reflect the change in BV/NAV. The update is included in the card below and the subscriber spreadsheets.

- Percentage Recommendation Range (Relative to CURRENT BV/NAV): No Change.

- Risk/Performance Rating: No Change. Remains at 4.5.

Earnings Results

The REIT Forum

Note: BV at the end of the quarter. Subscriber spreadsheets and targets use current estimates, not trailing values.

Valuation

The REIT Forum

Ending Notes/Commentary

ORC’s net spread less operational expenses metric, a figure that management has continued to highlight and refer to as the company’s core earnings equivalent/EAD metric, excludes one important factor/reconciliation. This specific metric excludes ORC’s current period hedging income. This is something I have continuously pointed out to subscribers.

As such, I would strongly recommend management provide an updated core earnings equivalent/EAD metric, whereas ORC’s current period hedging income (expense) is INCLUDED in this specifically referenced metric. This would equate to a more similar core earnings equivalent/EAD metric when compared to sub-sector peers.

This would merely cause less confusion for market participants moving forward regarding dividend metrics. Since ORC did not disclose the company’s current period hedging income figure in the company’s monthly update, I cannot disclose/discuss this amount at this time.

Orchid Island Capital also announced an unchanged per-share monthly dividend for July 2024 when compared to June 2024 ($0.12 per share). Simply put, this was correctly anticipated (within range). That said, remember, ORC reduced the company’s monthly dividend by (25%) back in October 2023 (not too long ago).

Finally, regarding equity activity, ORC once again “put the foot on the accelerator” and issued 12.0 million shares of common stock during Q2 2024. This calculates to 23% of ORC’s outstanding shares of common stock as of 3/31/2024. Simply put, notable quarterly common stock issuance which was deployed, as noted earlier, into higher coupon fixed-rate agency MBS. ORC issued an additional 2.0 million shares from 7/1/2024 – 7/10/2024.

I believe Orchid Island Capital, Inc. remains modestly overvalued (SELL). As such, readers should remain patient investing in ORC (and frankly the entire agency mREIT sub-sector) until valuations improve.

Read the full article here