")

As the price of oil falls back to the yearly average, many stocks in the space are presenting buying opportunities. If you are looking to get into the space, Canadian Natural Resources (NYSE:CNQ) is a great place to start. The company just reported very strong Q3 numbers with record production & included a dividend increase. The company has increased its base dividend for 24 straight years. I feel very confident saying it will be 25 next year, and 26 the year after that. Shareholders are in for a treat as the company achieves its debt target of less than $10 billion in the next 6 months. It’s for these reasons that 2024 will be the year of the shareholder.

**All dollar values discussed are $CAD**

How Was Q3?

On November 2nd, Canadian Natural released Q3 earnings. The market loved the results as the stock surged 4.5%, but since then the price of oil has fallen off and so has the share price. Regardless, the earnings show why Canadian Natural is a must-have stock if you believe in the oil & gas story. Some of the highlights from Q3 were:

- GAAP EPS of $2.59

- Net Income of $2.34 billion

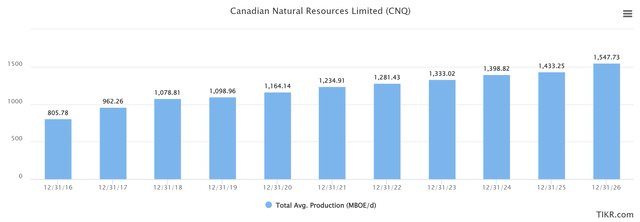

- Record quarterly production of approximately 1.39 million BOEs per day

- Cash flows from operating activities of $3.5 billion.

- Adjusted funds flow of $4.7 billion

- Debt to EBITDA at 0.7x at the end of Q3

All in all pretty strong. As you can see below, it is expected that Canadian Natural will continue to grow production, which is fantastic as that will lead to higher cash flows, which trickle down to the shareholders.

TIKR.com

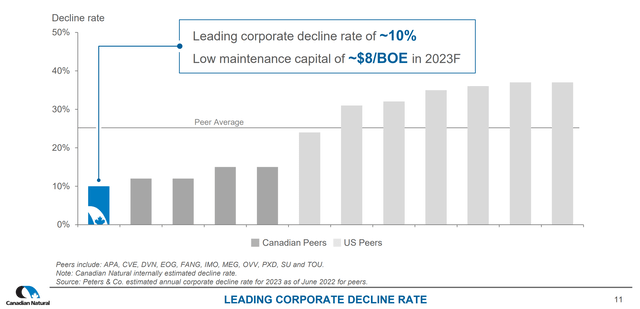

Usually, this would mean that we’re also going to see CapEx explode. But, that’s not the case. Like most of the industry, Canadian Natural is also in a bit of a holding pattern with respect to new projects. Obviously, things can come up, but nothing large is forecasted in the coming years. To be able to limit CapEx, yet grow production and free cash flow, you are laughing your way to the bank. Canadian Natural has a strong asset base with one of the lowest corporate decline rates out there at ~10%.

Canadian Natural Resources

The only real risk here is commodity pricing. So long as we see the price of oil remain stable, there isn’t much to worry about. Having such low debt, the company has positioned itself to run off of oil prices well below the current market.

They topped off the quarter with an 11% dividend increase. Canadian Natural is set to continue to reward its shareholders as the debt level continues to decrease.

How’s the Dividend?

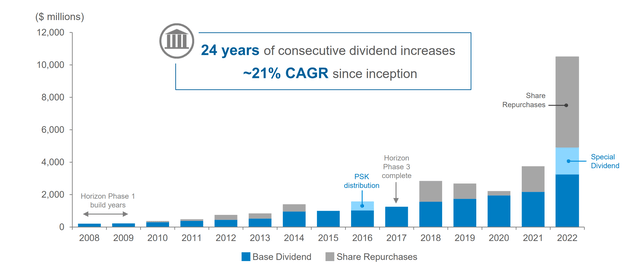

It’s growing!! In my most recent article on Canadian Natural, I mentioned that it was the safest way to play oil. Part of that is the stable, and reliable dividend. That remains true today. Something to keep in mind in the charts you will see below is the special dividend that we saw get paid out in August of last year. That throws off the idea of 24 years of continuous increases. On November 2nd, they announced an 11% increase taking the dividend up to $1.00 a quarter, or $4.00 a year. Hard to argue with that. Looking below, we can see the company is keeping its word concerning returning cash flow to shareholders.

Canadian Natural Resources

Typically I’ve been critical of commodity-based companies who refuse to cut their dividend. Often it can lead to debt pilling on just to cover the yield. That is something to keep in mind if we see oil prices plummet once again. If Canadian Natural ever does cut, there will be a rush for the exit. But when times are good, and the cash is flowing, who doesn’t love a good increase!! In 2022, the company calculated a return of $9.25 per share. $4.34 of which came from dividends, and $4.91 from share buybacks. Often, buybacks are overlooked by shareholders. While it is the company increasing its value, as a shareholder that also increases your value on paper.

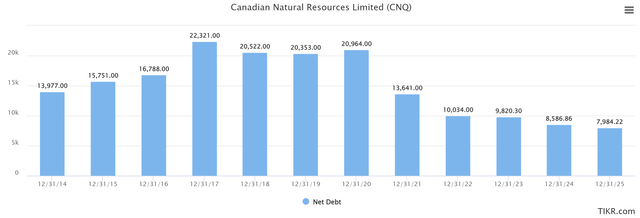

Will we see more buybacks and special dividends? I’m betting so. You’re going to want to watch the chart below very closely. While net debt is between $10-15 billion, the company takes its adjusted funds flow and takes away base capital and dividends. They are left with excess free cash flow. 50% of that will be spent on share buybacks, and 50% will go to the balance sheet & strategic growth capital/opportunistic acquisitions.

TIKR.com

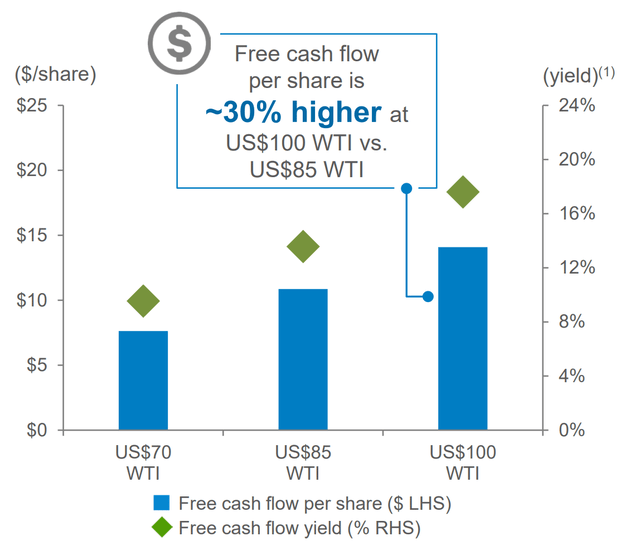

Where it gets really good is when that bar gets below $10 billion. Canadian Natural will then take adjusted funds flow, less base capital, dividends, and strategic growth capital. EVERYTHING that is left will be paid out one way or another. For reference, as we stand now, net debt sits at just over $11.5 billion. I fully expect them to hit the sub $10 billion mark in Q1 of 2024. Will be very exciting. So how much will we get? Well, being a commodity-based company, that depends on the price of oil. Looking below, you can see just how dependent it is on the price of oil. In 2022, the average price of WTI was just under $95. So far in 2023 (through September), we are at just over $77. That is quite the difference. While October was strong we have come back to the average in the last couple of weeks as we trade at $77.

Canadian Natural Resources

I’m not going to try and predict where the price of oil goes. I am bullish, but whether it trades at $80, $90, or $100 I have no idea. What I do know is that regardless, Canadian Natural is going to be making good money and returning a large portion of it back to shareholders in 2024. Because of this, I believe this stock is a buy on any sort of dip.

What Does The Price Say?

In February, I offered up a price target of $70. While the stock has returned 9% since it hasn’t quite panned out to where I thought it would. The main reason for that is strictly commodity pricing. As mentioned, the average price of WTI is about $18 different year-over-year. For that to happen, yet the stock still appreciated says everything you need to know about Canadian Natural.

TC2000.com

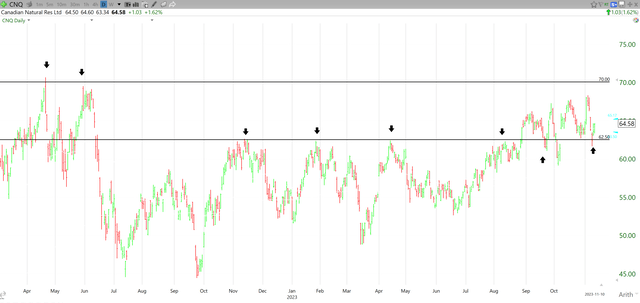

Back in February, I spoke about the stock nearing a breakout above $62.50. We saw a test in May and a backtrack. Then another series of tests in August before finally breaking through in late August. We then saw the stock spike, before re-testing and even breaking back through $62.50 a couple of times, even as recent as 11/8. The good news is that the stock has responded strongly after each test.

While $70.00 is only about 8% from current levels, it remains my current price target. The main reason for this is it would be an all-time high. Looking below, the encouraging trend right now is that we keep setting higher highs, and higher lows. As long as that continues, there is no reason not to be bullish.

TC2000.com

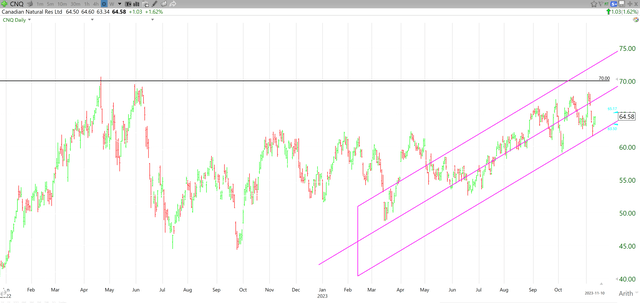

Should that reverse, I would be worried about where the stock goes from here. My current stop on the stock would be at $57.50. About 11% to the downside from current levels. This allows a bit of a heavier position to capture more of that dividend. Being a commodity-based stock, pricing can change quickly. It’s important to always have stops in place because of that. As mentioned, I am bullish on oil & gas, and Canadian Natural is one of the safest ways to play the industry.

Wrap-Up

At the end of the day, if you want to be bullish on oil, or you are unsure but what exposure, Canadian Natural is a great place to start. The company is very well managed, and one of the safest investments in the space. Canadian Natural pays a strong dividend yielding 4.6%. As we approach the $10 billion net debt mark, we are going to see increased dividends and stronger buyback programs. Thus leading to 2024 being the year of the shareholder.

Read the full article here