Welcome to another installment of our CEF Market Weekly Review, where we discuss closed-end fund (“CEF”) market activity from both the bottom-up – highlighting individual fund news and events – as well as the top-down – providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the second week of May. Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

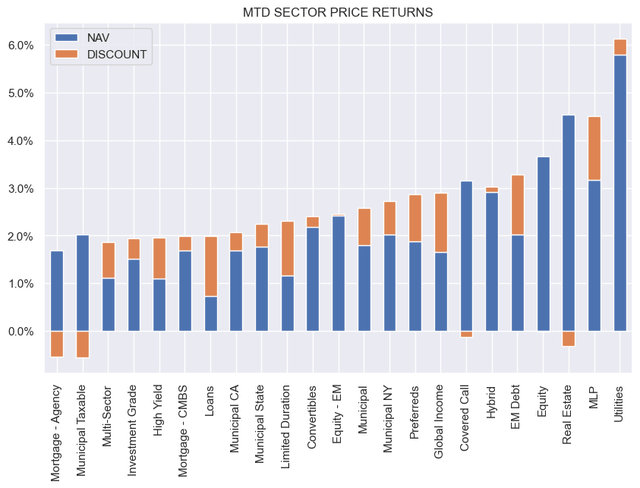

CEFs enjoyed a strong week, with all sector NAVs moving higher. MLPs and Utilities finished in the lead. The month-to-date picture is strong with broad-based gains. Both NAVs and discounts have supported price gains.

Systematic Income

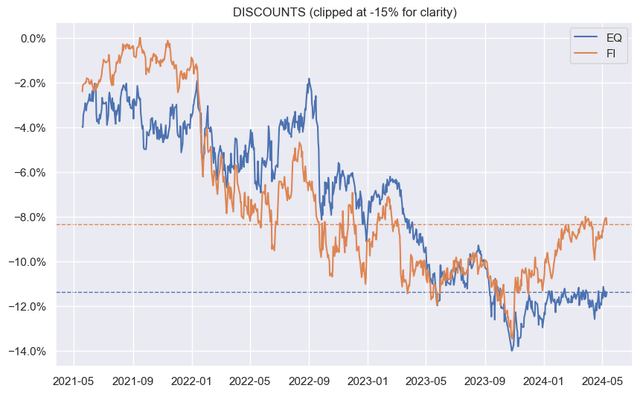

Fixed-income CEF sector discounts are trading near their tights over the past year. Equity CEF discounts remain more subdued.

Systematic Income

Market Themes

The last few months have seen a slew of CEF activism as asset managers like Saba and Karpus accuse CEF managers of various wrongdoing as they try to wrest control of the board.

One criticism that CEF activists tend to levy at managers is that the discounts of the targeted funds are much too wide. Their presence, according to the activists, is evidence that the managers are not good stewards of investor capital. However, as with anything else, we don’t have to take activists at their word. Let’s take a closer look at this.

The activist criticism is straight-forward. Wide discounts are bad because the wider the discount, the lower the price of a given holding and the lower the value of the investor’s investment account.

The discount question cuts both ways, however. The wider the discount, the higher the implicit level of leverage that an investor achieves on their capital. This creates a kind of trading on margin dynamic without the risk of a margin call. The discount also magnifies the underlying yield of the asset portfolio and, if the discount is wide enough, fully offset the management fee, delivering active management at a no or negligible cost.

Another way to think about a CEF discount is that it is a mathematical outcome of the management fee and secondary-market trading. In other words, because CEF managers are entitled to a fee on a basket of assets, that basket of assets should trade at a discount to their secondary-market value in a fund wrapper. Of course, not all CEFs trade at discounts, but that’s because fees are not the only driver of discounts which are also driven by risk sentiment, fund alpha, leverage cost and other factors.

CEF activists can use the presence of the discount to suggest that a given fund has no alpha. This may be true in theory; however, the reality is that risk sentiment and recent performance usually swamps any alpha-related discount dynamics. One evidence of this is that all 71 CEFs in the Municipal CEF sector trade at discounts. It seems unlikely that not a single fund in the sector has net positive alpha.

What this suggests is that the mere presence of a discount is not the fault of the manager but rather the reality of the CEF structure, where the discount simply capitalizes the fee annuity. If mutual funds traded in the secondary market, they would mostly trade at discounts as well. Ultimately, we can support what CEF activists try to achieve, but we don’t have to buy their explanations. Their primary goal is to make money, and their moralistic grandstanding is often smoke-and-mirrors.

Market Commentary

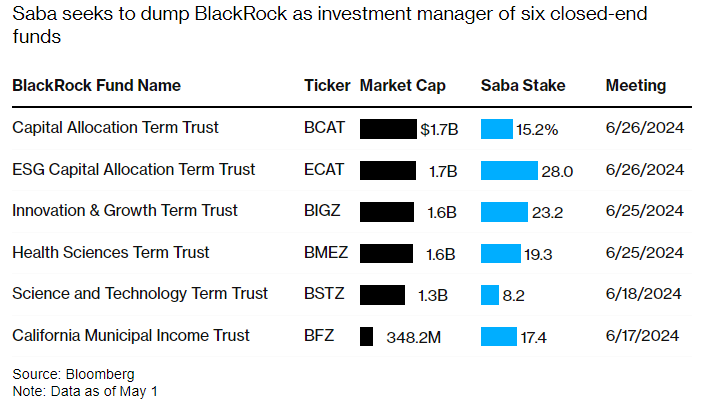

BlackRock and CEF activist Saba are going at it. Saba launched a bid to remove BlackRock from managing six of its funds. They include BCAT, ECAT, BIGZ, BMEZ, BSTZ, BFZ with total assets of over $10bn. Saba’s stake in these ranges from 8 to 28%. The proxy meetings are due in late June where new directors may be elected to decide the fate of the funds. There is a lot of the usual moralistic grandstanding by both parties. Saba is alleging that BlackRock is illegally preventing its nominees from being elected while BlackRock is saying Saba just wants to take over the funds to generate fees which it has already done a few times.

BlackRock

Elsewhere, the activism in the Muni CEF space that was highlighted a few weeks ago is beginning to bear fruit. A BlackRock Muni CEF (MUI) announced it is holding a tender offer of 50% of its shares at a 2% discount to NAV contingent on the fund being able to convert to an unlisted interval CEF, i.e. a fund that provides liquidity to investors by periodically purchasing a set number of shares.

This is fairly unusual as far as CEF responses to activism go. Tender offers, terminations, or conversions to open-end funds you tend to see now and again, but a conversion to an unlisted CEF is very unusual. The main problem with this is that it is bad news for most of the fund’s current shareholders, who are unlikely to be very excited about holding an unlisted fund. The possible benefit to BlackRock is that it will make it more difficult for CEF activists to do their job, as acquiring a lot of shares in an unlisted fund would be tough.

There are two potential tactical trades here. One is to buy the fund now at around a 7% discount when half the shares are likely to be bought back at a 2% discount, leaving some potential upside. The second would be to buy the fund once it completes its tender offer. At that point, very few of its shareholders will be willing to hold it in an unlisted form (the remaining shareholders would be tactical traders or those that didn’t pay any attention, both of which would be eager sellers) which means that its discount is likely to blow way out, creating an attractive, if illiquid, holding for long-term buy-and-hold investors. First Trust announced the completion of its MLP fund mergers. Recall that the MLP CEFs FEN, FEI, FPL and FIF were merged into the ETF EIPI. This was a tax-free reorganization, however a couple of the funds said they would need to adjust their NAVs slightly (FEN up and FEI down) prior to the merger.

The manager said that more adjustments to NAVs were likely for the CEFs as well as EIPI leading into the merger. This likely has to do with deferred tax assets and liabilities, which is a feature of only MLP CEFs. The pitch for the merger was daily portfolio transparency (a minor benefit), discount elimination (beneficial for existing investors merging into the ETF, less so for new shareholders), lower total expense ratios (not by much as it appears EIPI has a hefty 1.1% management fee – very high for active ETFs and high even for CEFs).

Read the full article here