")

Chubb Limited (NYSE:CB) has strong business fundamentals and positive growth prospects over the long term, being an interesting growth play in the insurance sector.

Business Overview

Chubb operates as a property and casualty (P&C) insurance company, being one of the largest insurance companies in its segment. The company was formed in 2016 through the acquisition of Chubb by ACE Limited, which adopted the name Chubb Limited worldwide. Chubb is listed on the New York Stock Exchange and its current market cap is about $108 billion.

The company has operations across the globe, being present in some 54 countries, offering P&C insurance across several lines, including commercial and property insurance, personal accidents and, to a less extent, life insurance being focused on Asia in this segment. Its distribution is done through insurance brokers and agents, plus direct-to-consumer platforms.

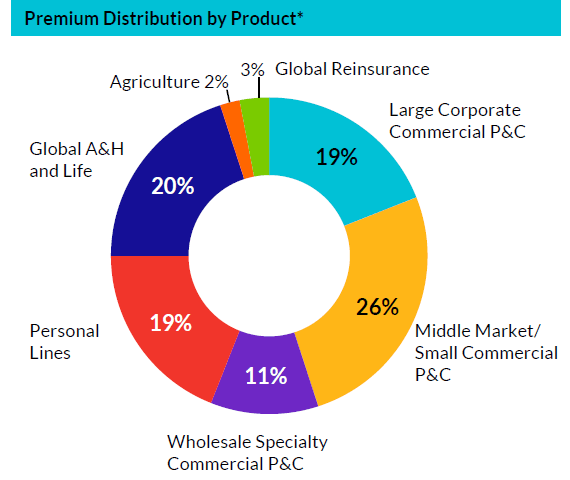

By product, it has a good premium diversification given that its largest insurance line (middle market/small commercial P&C) only accounts for 26% of total premiums, and other lines have similar weights of around 20% on total premiums, as shown in the next graph.

Business diversification (Chubb)

Geographically, despite being present across the globe, 52% of its premiums are still generated in the U.S., while Asia accounts for some 19% of total premiums, Europe, Middle East and Africa account for 17%, Latin America generates 7%, and Bermuda/Canada is responsible for the remaining 5%.

Regarding the company’s strategy, it has been focused mainly on maintaining sound underwriting criteria and generating recurring investment income over the long term. Chubb has a very strong underwriting history, showing that it only takes risks when it can properly quantify the risks it’s taking and can earn an acceptable return over the long term.

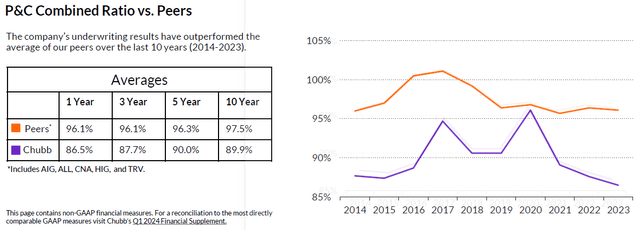

This approach can be seen in its combined ratio over the past few years, which has been consistently below its peers even during years of significant catastrophe claims, showing that Chubb’s underwriting is among the best in the industry and can be considered to be a competitive advantage over its competitors.

Combined ratio (Chubb)

As seen in the previous graphic, Chubb has been able to report a combined ratio of close to 90% (vs. 97.5% for its peers), on average, over the last decade, being consistently below 100%, which means it has produced underwriting profits every year. This is an outstanding history and something quite rare to see in the insurance industry, especially in years with higher than usual catastrophe losses, such as 2017 or 2020.

Another area where Chubb has invested in recent years has been in technology to improve its customer service and make it easy to dobusiness with the company, something that is important in the insurance industry because there isn’t much product differentiation between companies and good customer service can make the difference in the long term to retain customers and gain new ones.

In international markets, where the company has a lower presence and market share, its growth strategy has been more focused on expanding its presence, namely in countries where there are positive structural growth drivers. Indeed, in Asia or Latin America the insurance penetration is lower than compared to developed countries, boding well for Chubb’s long-term growth prospects.

Another important driver of its earnings over the long term is investment income, as the vast majority of its assets are invested in financial assets. Indeed, its investment portfolio amounts to about $140 billion, representing some 60% of Chubb’s assets.

Its investment approach can be considered conservative, investing heavily in fixed income securities with relatively low credit risk. This strategy is not expected to change much in the future, as one of Chubb’s main priorities is to have a strong credit rating, which is currently AA by S&P, thus its investment allocation must be conservative to not put its credit rating in jeopardy.

This means the company is not expected to take more risk to earn a higher investment income in the future, which seems sensible given that Chubb’s priority is to have financial strength and a sound business model over the long term.

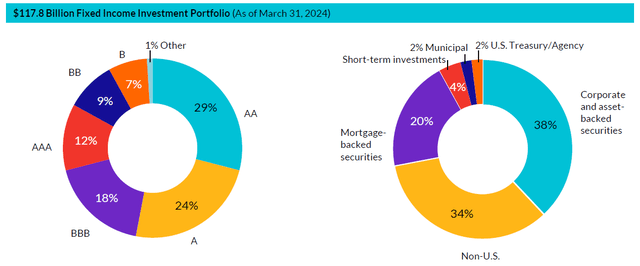

Given this backdrop and investment approach, some 84% of its investment allocation was to fixed income securities at the end of last March, with an average credit rating of A (by S&P) and a duration of nearly five years. The bond portfolio was well spread by sector, geography, and issuers, and about 85% was invested in investment-grade bonds.

Asset allocation (Chubb)

Financial Overview

Regarding its financial performance, Chubb has a very positive track record, reporting growing net premiums written and earnings in recent years. As Chubb is mainly geared to P&C, it was not much negatively affected by Covid-19, which lead to higher losses in the life insurance segment due to elevated mortality rates, while more recently its financial performance was supported by higher investment income due to increasing interest rates and a favorable pricing environment in the P&C industry across the globe.

In 2023, Chubb reported a record year supported by strong growth across all its business units, reporting double-digit premium revenue growth and strong net profit growth.

Its net premiums written increased by 13.5% YoY to $47.3 billion, due to higher pricing across P&C lines. In 2022, there was relatively high claims in the industry due to several weather events, which led to higher pricing across the industry, a trend that was positive for Chubb’s top-line growth during the last year. Due to its strong underwriting skills, higher pricing led to a record combined ratio in 2023, which declined to 86.5% and led to underwriting profits of about $5.5 billion, being an industry-leading underwriting performance.

On the investment income side, Chubb benefited from higher rates and credit spread to grow its investment income to $5.3 billion, up by 33% YoY, being another important support for earnings growth during the last year.

Despite the inflationary environment, Chubb reported strong cost control and positive operating leverage, leading to a core operating profit of $9.3 billion, up by 45% YoY, which benefited from a positive operating performance and a change in tax law in Bermuda, which led to lower taxes paid. Its net income was around $9 billion, up by 72% YoY, and its return on equity (ROE) ratio, a key measure of profitability in the insurance industry, was 15.4% in 2023, which is a very good level compared to its peers.

During the first quarter of 2024, Chubb maintained a very positive operating performance, continuing to benefit from higher pricing in the P&C segment. Its underwriting income was up 15% YoY and its combined ratio was 86% in Q1 2023, life insurance income was up almost 10% compared to the same period of last year, and Chubb’s investment income increased by 23% YoY. Its net income was up by 13% YoY to $2.14 billion and its ROE was 14.3%, remaining at a very good level.

Going forward, Chubb’s strategy is not expected to change much, being focused on maintaining a strict underwriting criteria, expanding its geographical reach, and growing its investment income while maintaining a conservative asset allocation. Its growth prospects are also supported by its international operations, especially in Asia which has a relatively low insurance penetration, boding well for its premium growth in countries such as China for instance.

Given its strong business fundamentals and a capital position of about $76 billion at the end of 2023, Chubb seems to have a strong balance sheet and doesn’t need to retain much earnings in the near future.

Indeed, it has returned significant capital to shareholders in recent years and has an outstanding dividend history, given that it has raised its dividend for more than 25 years in a row, being therefore a dividend aristocrat.

In 2023, Chubb returned some $3.9 billion to shareholders, through $2.5 billion of share buybacks and dividends of $1.4 billion. Its current quarterly dividend was recently raised to $0.91 per share, or $3.64 annually, which leads to a forward dividend yield of only 1.4%. This is not an impressive dividend yield and there are better income alternatives within the insurance sector, such as its European competitor Ageas (OTCPK:AGESF) which I’ve covered recently and yields more than 7%.

Regarding its valuation, Chubb is currently trading at 1.8x book value, at a premium compared to its historical average of about 1.4x book value over the past five years. While at first glance this could be seen as a sign of overvaluation, investors should note that Chubb has grown its premiums and earnings considerably over the past few years, plus its profitability is nowadays much higher than it was in the past. Indeed, its ROE has been about 14% in recent quarters, while before the pandemic its ROE was in the high-single digits, thus justifying a higher multiple.

Compared to its closest peers, Chubb seems to be attractively valued, given that competitors such as Progressive (PGR), Hartford Financial Services (HIG) or Allstate (ALL) all trade at higher valuation multiples. The exception is American International Group (AIG), which is trading at a lower multiple, but is a peer that reports a lower profitability level and has historically traded at a discount to its peers.

Therefore, Chubb seems to be attractively valued considering its strong fundamentals and industry-leading underwriting margins, a profile that has also grabbed Berkshire Hathaway’s (BRK.A) attention in recent months, given that the financial behemoth has bought Chubb’s shares recently. This is a strong signal that Chubb has a wide moat in the insurance industry and its shares are attractive for long-term investors, as Berkshire is well-known as a value investor that invests in companies with a strong competitive advantage in their industries.

Conclusion

Chubb is one of the best companies in the P&C insurance industry, having strong underwriting results and better growth prospects than peers due to its exposure to some growth markets. Its current valuation seems attractive for long-term investors despite its strong share price performance in recent years, making it one of the best growth plays in the insurance industry right now.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here