")

Overview

I am always on the hunt for high-quality companies as a long-term dividend growth investor. I strongly believe in the philosophy that dividend investing makes it a lot easier to stick with a long-term outlook and enables you to have a stronger emotional resistance to fluctuating stock prices. This is because the steady income that’s provided makes it really easy to continue holding, as my priority shifted from looking at the value of my investment and instead focusing on how much cash flow my investments produce over time. This is how I came across The Cigna Group (NYSE:CI).

While Cigna’s dividend history is a bit rugged and unusual, I believe there is some strong potential here following the more recent increase history. Additionally, the starting dividend yield is quite low at 1.6% which means that it won’t produce a sizeable amount of dividend income upfront, even with a large starting investment. However, I wanted to review why I believe that the dividend growth alone is what makes CI worth some consideration. I also think that CI has some strong upside potential, despite trading near all-time highs already. I aim to provide an unbiased analysis of the company and share some of my findings.

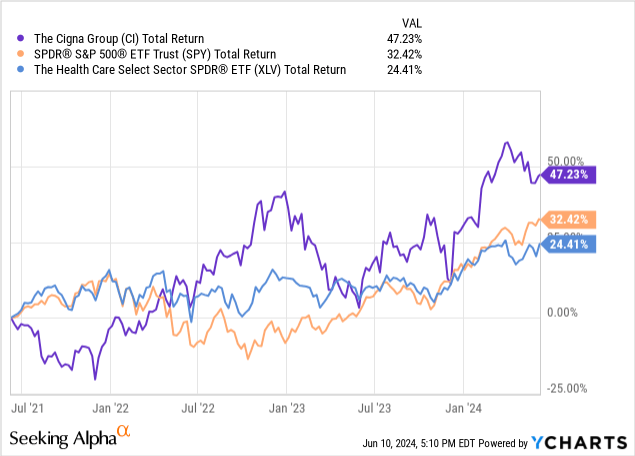

We can see that Cigna has delivered some strong total return that has outpaced both the S&P 500 (SPY) and the Health Care sector (XLV). The company’s earnings continue to grow and expand, while the balance sheet shows a lot to like. I believe that this outperformance of the market can continue based on the double-digit growth of their business segments and revenue going forward.

Just for a bit of context, The Cigna Group operates as a global health services company that provides a portfolio of insurance products and services for customers. In fact, some of you may be familiar with Cigna through your employer’s health insurance, as this is only one of the many revenue sources for the company. The company operates within two main segments: Evernorth Health Services and Cigna Healthcare.

Financials

Cigna reported their Q1 earnings at the beginning of May and the results were very strong. Revenue for the quarter grew by a massive 23.3% year over year, totaling $57.3B. Earnings per share came in at $6.47 for the quarter, beating estimates by $0.25 and this increase in EPS and revenue can be mostly attributed to the growth of their Evernorth Health Services segment. For reference, approximately 60% of Cigna’s revenue comes from this segment, while the remaining 40% comes from the Cigna Healthcare segment.

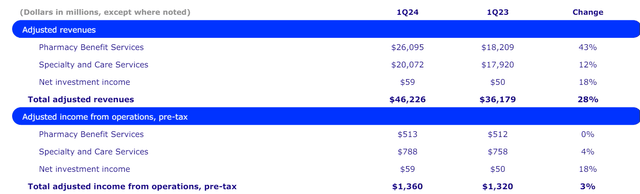

Focusing first on the Evernorth segment, we can see that the pharmacy benefits segment continues to makeup the largest slice of the business. This segment has seen an increase in adjusted revenue by 43% over the prior year, totaling $26B for Q1. The specialty and care services channel saw a 12% rise in revenues, amounting to $20B for the quarter.

Evernorth Health Segment (CI Q1 Presentation)

The large growth of the pharmacy benefits segment can be attributed to some large client wins and ongoing expansion of existing client relationships. Additionally, an increase in pharmacy and medical customers was the main factor contributing to the revenue growth. The specialty and care services segment saw a sizeable increase in revenue from affordability improvements, which opened the door to new clients and customers. However, this growth was offset by increased costs related to investments and onboarding of new clients, which is why we see only a marginal increase in total adjusted income from operations of 3% year over year.

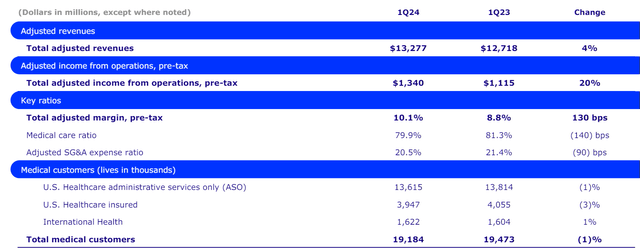

Moving onto the Cigna Healthcare segment, we can see that this slice of the business accounts for about $13.2B of revenue, showing a slight 4% increase from the year prior. This segment is where CI provides solutions to clients and customers related to medical plans, individual health insurance plans, and Medicare related services. Even though the total number of medical customers slightly decreased by 1%, total adjusted income from operations increased by a sizeable 20% due to an increase in pricing margins.

Cigna Healthcare Segment (CI Q1 Presentation)

Management’s outlook going forward is to achieve a full-year revenue amounting to $235B and adjusted income from operations totaling $8.065B. They also plan to achieve the following earnings growth for each segment:

- Specialty and Care Services: 8% to 12% growth over the next fiscal year.

- Pharmacy Benefit Services: 2% to 4% growth over the next fiscal year.

- Cigna Healthcare: 7% to 10% growth over the next fiscal year.

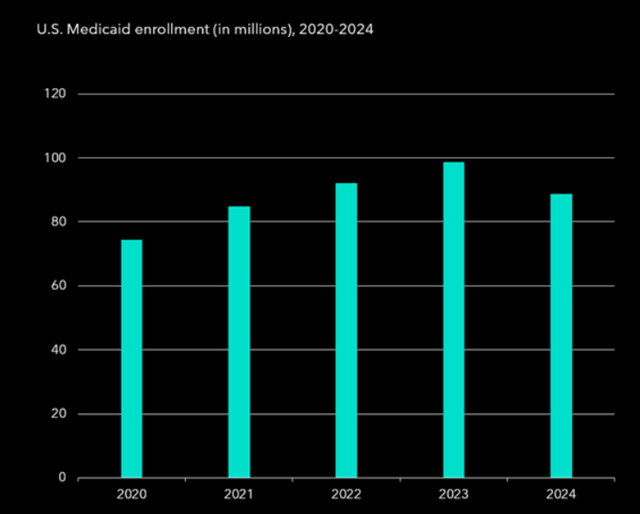

These amounts average out to a blended 6% to 9% estimated growth rate company-wide. This level of growth is highly likely in my opinion as we still see the effects of a post-pandemic world. According to data, Medicaid enrollment numbers are starting to fall, which presents an opportunity for CI to gain more market share growth through increased customers.

Clarivate

As more of the population can no longer apply or qualify for Medicaid, this will directly translate to an increase in enrollment plans for services offered by CI. This would ultimately lead to an expansion in their customer base and will lead to higher revenues across segments.

Lastly, liquidity remains solid now as CI currently has about $8.4B in cash and equivalents at the moment. Furthermore, CI pulls in about $11.6B in cash from operations at the moment. This strong cash position can help maneuver any potential headwinds or slowing of revenues in the future. However, the company does have an elevated level of debt, with long-term debt amounting to nearly $31B as of the last quarter.

Dividend

As of the latest declared quarterly dividend of $1.40 per share, the current dividend yield sits around 1.6%. While the yield is admittedly very low, we can at least be assured that the dividend is very safe at the current level. The current dividend payout ratio sits at a very healthy 20%. This low payout ratio is a good indicator that CI has plenty of free cash flow that can be reinvested back into the growth of the company, or the additional cash can be used towards future dividend raises.

The dividend history here is a bit odd. So far, CI has increased annual dividend payouts for three consecutive years. While the increases during these recent years have been incredibly strong, this wasn’t always the case. The dividend amount previously was paid out only once per year, on an annual basis. In fact, the dividend rate remained the same between 2008 all the way through 2020, until it was finally raised and shifted back to quarterly payments in 2021.

Seeking Alpha

So, while Cigna may not have been the best choice historically for consistent dividend income, I believe we are on a path of change. The recent dividend growth rates have been astronomical and if this continues, I can see a long-term investor’s yield on cost rapidly rising. For instance, the dividend has increased at an average CAGR (compound annual growth rate) of 38.03% over the last three-year period. If we zoom out to a five-year time frame, the increases look unrealistically large at a CAGR of 165% due to how lows the dividend was five years ago.

As revenues continue to grow, I anticipate dividend raises to continue to be strong. The last dividend increase was by 14% and because the current payout ratio remains so low, I expect the future raises to continue in that double-digit territory. For a stock that has a yield at only 1.6%, this shouldn’t be too unreasonable to expect.

Valuation

In terms of valuation, I believe that the high-quality nature of the business hasn’t been fully priced in yet. The company current trades at a price to earnings ratio of 12.92x, which sits above its five-year average price to earnings ratio of 11.97. However, the current price to earnings ratio does sit below the sector median of 19.49x, which could also be an indication of undervaluation. Wall St. seems to believe that CI is undervalued because the average price target sits at $392.04 per share. This represents a potential upside of over 15% from the current price level.

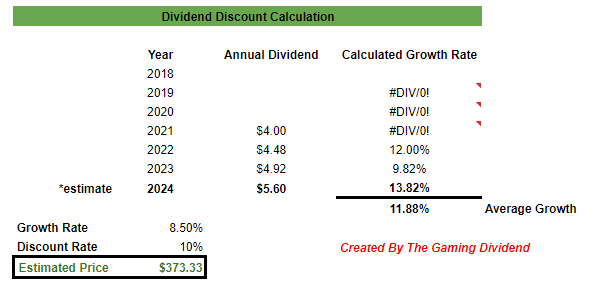

The highest price target sits as high as $435 per share and the lowest price target is $349 per share. To get another reference point for a fair value estimate, I decided to conduct a dividend discount model here based on the growth over the last few years. As previously mentioned, management expects growth to land somewhere between the 6% to 10% range.

Forward revenue growth currently lies at 11% while EBITDA growth is at about 8%. I expect the company to grow at the higher end of the expected range going forward due to the catalyst of more customer enrollments. Therefore, I thought an estimated growth rate of about 8.5% was a fair input.

Author Created

With these inputs in mind, I come to an estimated fair price of about $373.33 per share. This represents a potential upside of approximately 10.2% from the current level, assuming they can grow earnings by 8.5%. I think this is extremely likely, as the year-over-year EBITDA growth has averaged closer to 20% over the last five-year period. Additionally, the business plans to grow cash flow by $60B over the next five years, which will be used to increase capital expenditures, the dividend, and strategic acquisitions that can drive growth.

Vulnerability

There will always be the looming risk of government intervention within the healthcare industry. As we approach the US Presidential elections at the end of this year, healthcare is usually one of the more important topics of discussion. In a world where universal healthcare can become a possibility, I imagine this would mostly be a negative thing for businesses like Cigna. This would likely limit growth opportunities and profit margins would shrink as the number of enrollments would also decrease. We’ve already seen the numbers of medical customers slightly decrease over the year and how it hindered the growth potential, like I previously mentioned. Ultimately, if something like universal healthcare happens, it would render customer account less important in my opinion.

Takeaway

In conclusion, CI’s growth prospects look strong and make this an interest buy. Despite trading near all-time highs, the company continues to provide excellent earnings growth across all segments. Growth projections from management are strong for next year as well, and I believe that performance will likely fall at the higher end of the growth range of 6% to 10%. This is because of the lower Medicaid enrollments, which means that Cigna effectively has more potential customers to help grow their revenue base through health insurance services. Additionally, the strong cash flow growth will likely lead to the continuation of double-digit dividend raises. The dividend payout ratio remains very low at the moment, which leaves a lot of room open for growth. Lastly, I believe there to still be a 10% upside from the current price levels, based on my dividend discount model.

Read the full article here