")

Introduction

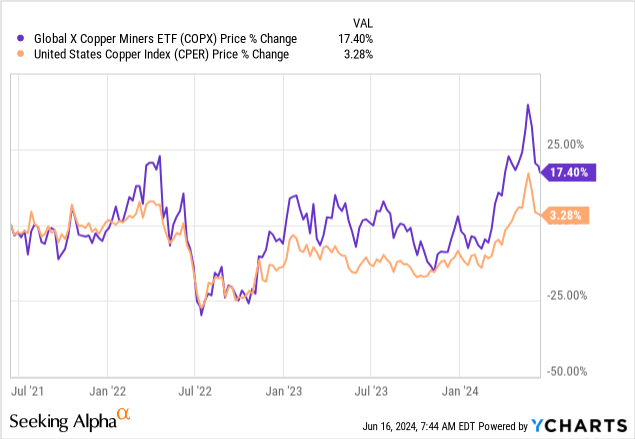

The Global X Copper Miners ETF (NYSE:NYSEARCA:COPX) has proven to be a solid choice for investors to gain exposure to the copper sector, delivering substantial returns for its investors. Since my previous article last September, where I rated COPX a “Strong Buy”, the shares have risen 15.33%, aligning with the upward trajectory seen in the price of copper.

This solid performance reflects our initial thesis: that COPX with its exposure to a diversified pool of copper miners, is strategically positioned to benefit from the anticipated demand-supply imbalance for copper. This is driven by surging demand for copper, driven by its role in electrification and supply unable to keep up.

My preference for COPX over direct copper futures (CPER), is due to the leverage copper miners can provide. As copper prices rise, miners would normally see profitability rise faster due to their operational gearing. Trading with an average price to free cash flow (“P/FCF”) ratio of 10.82 for companies within the ETF, we see the opportunity for multiple expansion driving the price of COPX higher. We see this being partly driven by mergers and acquisitions as mining companies attempt to build out and secure their copper portfolio. We saw this earlier this year with the attempted takeover of Anglo American (OTCQX:AAUKF) by BHP (BHP), with the bid representing a 31% premium to share price.

In this follow-up article, I will dive deeper into why I maintain a “Strong Buy” rating on COPX. Despite the recent fall from this year’s highs in the copper price, the long-term outlook for the copper price remains positive, underpinned by its role in electrification, and supply constraints. COPX, with its geographically diversified exposure to a portfolio of copper mining companies, continues to offer a solid opportunity for investors looking to gain exposure to this essential commodity.

Soaring Demand

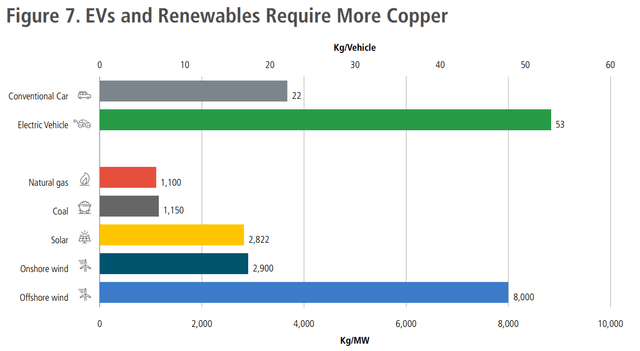

Copper demand is booming. With its excellent conductivity properties, copper has become an integral part of the modern world. It is used in homes, factories, for power generation and transmission. With the continuing growth of electrification demand for copper is set to soar. Electric vehicles are predicted to use 2-3 times as much copper as their traditional counterparts. In power generation, for solar seven times as much copper is needed to produce the same power as traditional power generation. For wind power that figure is seven times as much. With many governments continuing policies of switching to an energy system based on renewable energy and promoting electric vehicles over conventional, in some cases banning combustion engine vehicles, demand for copper looks only set to grow.

The role of critical minerals in energy transition, IEA, May 2021

This results in anticipated demand for copper almost doubling by 2035, a huge increase in demand. Given the anticipated surge in demand, unless supply increases to meet this, conventional economic theory suggests that prices will inevitably rise.

Restricted Supply

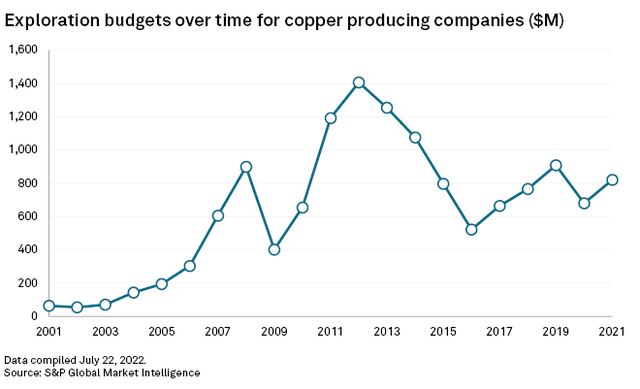

Failure to meet this surge in demand could jeopardize the transition to a greener future. However, the world is not rapidly increasing the mining of copper. Since peaking in 2012, exploration budgets for copper have dropped, with miners focusing on smaller expansions of existing mines. Any discoveries that are made are often of much lower grades, resulting in higher costs of extraction.

S&P Global Market Intelligence

This has led to the pipeline of projects being thin, with many recent discoveries of lower grades having higher costs associated with them. This has led some analysts to suggest that copper prices must rise over 20% from recent highs to attract investment in new mines. With many environmental regulations getting tougher, it is only taking longer to bring new mines on-stream. Current exploration and planned capacity increases come nowhere close to what is needed to meet the future anticipated demand for copper.

One alternative proposed to boost supply has been to recycle more copper. However, this alone cannot meet the surging demand for copper due to several limitations. Firstly, recycling currently only accounts for 17% of the world’s refined copper supply, making it totally insufficient to meet the projected doubling in demand. Additionally, the recycling infrastructure, particularly in emerging markets, is significantly underdeveloped leading to low recycling rates, and inefficient processing. Another issue comes from the fact we need so much more copper. Much of the copper in use today, and for use in new applications like electric vehicles, will not reach its end of life for decades, and hence will only be recycled in decades time. With recycling not able to match the anticipated increase in demand alone, this underscores the need to expand copper production from mines.

With soaring demand and limited supply, copper prices appear poised to only go higher.

Why COPX?

Given you now know why I am bullish on the copper price, it is important to understand what exactly the Global X Copper Miners ETF, trading as COPX, is. This is an ETF that’s core aim is to offer investors to a selected basket of copper mining companies across the world. Although the companies may also engage in the mining and refining of other materials, a significant proportion of revenues must be derived from copper. The maximum holding weight is 4.75% with the ETF rebalancing twice a year in April and October.

The current top 10 holdings of the ETF are Boliden AB (OTCPK:BLIDF), KGHM Polska Miedź SA (OTCPK:KGHPF), First Quantum Minerals Ltd. (OTCPK:FQVLF), Glencore PLC (OTCPK:GLCNF), Teck Resources Ltd. (TECK), BHP Group Ltd. (BHP), Lundin Mining Corp. (OTCPK:LUNMF), Freeport-McMoRan Inc. (FCX), Antofagasta PLC (OTC:ANFGF), and Southern Copper Corp. (SCCO). This provides exposure to a geographically diversified portfolio of mines and reduces the risk of investing in a single company. This provides exposure to almost all of the top 10 largest copper mines in the world with the exception of two mines that are operated by the Chilean government.

Like many other companies engaged in the production of key commodities, the miners in COPX are price takers and heavily exposed to the price of copper. When copper prices rise, miners have the ability to generate a greater percentage profitability increase due to operational gearing. With COPX allowing exposure to both old and new copper mines, I believe it is an ideal choice for investors wanting exposure to this key commodity.

Risks

In my previous article, I covered what I believed to be the three main risks to my thesis: the copper price, geopolitical factors, and reversal of government net-zero goals. In this article, I want to review some of these risks and also other risks that I believe may affect the valuation of COPX.

One risk I identified was the threat of an initial short-term fall in the copper price. Although the copper price reached a record high earlier this year it has since fallen back. This can be partly attributed to growth in stockpiles of copper, and a fall in manufacturing output in China in May. Other factors such as a recession could drive prices lower, however, in the long term, I remain bullish on the copper price.

Another risk is that of geopolitical factors. We have already seen this risk come about as First Quantum Minerals’ mine in Panama was closed following massive protests. This caused the shares in First Quantum Minerals to fall 39%. With mines becoming harder to approve, rising environmental standards when mining, and risks of higher royalties, copper miners face a wave of challenges. On one hand, COPX helps mitigate this challenge by investing in a geographically diversified array of miners, so problems at a single miner can be mitigated. This, however, does not mitigate the fact that many mines are concentrated in the same jurisdiction such as Chile.

The anticipated rise in copper prices driven by electrification and supply constraints may present a double-edged sword. While a higher copper price will increase profitability for copper miners, there is a high risk of demand destruction if the price rises too high. More importantly, copper substitutes do exist effectively putting a lid on how high the copper price can rise. One alternative is aluminum, which can be substituted in multiple situations. Although only 60% the conductivity of copper, it is nearly a third of the weight and almost a 1000 times more abundant. If the copper price rises too high the economic incentive to switch to aluminum only grows. Already aluminum has been deployed in a variety of electronic applications and research is ongoing into enhancing its conductivity closer to that of copper.

Conclusion

As the metal of electrification, the fundamental drivers of copper demand remain strong. Coupled with tight supply, it seems inevitable that copper prices increase. COPX’s diversified exposure to a wide range of copper miners put it in a position to benefit from this demand-supply imbalance. For investors seeking to gain exposure to this essential commodity, COPX offers a compelling opportunity. The ETF’s diversified array of copper mining companies enables a broad exposure to the sector as the world turns to a more electrified future. I therefore continue to give COPX a “Strong Buy” rating, confident that it should continue to provide a positive return to investors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here