(CRWD)")

CrowdStrike (NASDAQ:CRWD) will be reporting Q1’25 on June 4, 2024, and continues to present a compelling story as enterprises tackle the challenges associated with the new threat landscape that is AI/ML. As AI progressively intertwines with enterprise operations, whether it is used for automation, performance optimization, or acts as a threat vector for data leakage, GenAI is here to stay and will become a considerable challenge as the rate of change opens an entirely new door for threat actors to steal trade secrets and customer data, amongst other things. CrowdStrike’s AI-native single platform security solution aims to cover all aspects of cybersecurity without the need for multiple consoles, multiple platforms, and the high associated costs for hiring experts to manage these products. Despite the challenging macro landscape, CrowdStrike’s total cost savings as it pertains to their customers offers a compelling growth story as Falcon is gradually becoming the go-to solution. I reiterate my STRONG BUY recommendation for CRWD stock, with a price target of $475/share at 23x price/sales.

Be sure to read my previous report covering CRWD dated February 12, 2024:

CrowdStrike Will Have Their AI Moment

CrowdStrike Operations

CrowdStrike continues to make strides across their subscription offerings and their ability to land and expand new customers. I believe the biggest strength CrowdStrike has to offer isn’t necessarily their diversified security offerings, but rather, the single platform strategy that covers the entirety of IT infrastructure, whether on-prem or cloud-hosted. When considering competing platform providers such as Palo Alto Networks (PANW), CrowdStrike has complete integration across each layer and automates the majority of the process for a faster implementation process. This ease of use allows for a quick transition from competing platforms to CrowdStrike’s Falcon platform as the firm further scales across enterprises and hyperscalers. Given the increasing complexity of IT infrastructure with the addition of AI/ML applications, this feature is exceptionally beneficial as time to use is a necessity.

CrowdStrike’s platform was designed from the ground up as a single agent and agentless cloud security solution, allowing for the firm to integrate with ease across the next generation of IT infrastructure. As it pertains to my thesis covering enterprise use for AI, as outlined in my reports covering Dell Technologies (DELL) and Oracle Corp. (ORCL), I anticipate initial use cases for AI applications to take place across cloud platforms as the supply constraint for acquiring Nvidia (NVDA) H100s remains prevalent. I do anticipate AI/ML applications to inevitably migrate to private data centers in time as the H100s become more readily available; however, this likely won’t occur until CY1h25. Regardless, whether applications are run in the cloud or on-prem, or both, Falcon offers a single platform solution for enterprises to secure their hot and cold data with ease through their own AI automation features. Unlike competing security platforms that require a completely new set of consoles and subscriptions, CrowdStrike’s Falcon platform offers the all-in-one solution that has the ability to keep this valuable data secure, no matter the location.

CrowdStrike has taken the initiative to bolster their presence in the next generation of AI applications by acquiring Flow Security, a small startup that focuses on runtime data security and classification. This product’s goal is to prevent data leakage at all points in the lifecycle, covering areas like access control, real-time data discovery, classification, risk detection, and real-time policy enforcement. One point that stuck out in CrowdStrike’s q4’24 earnings call when discussing the acquisition was management’s patience in bringing newly acquired products to market, sometimes taking 18 months before product integration. Though this may not necessarily excite investors as the acquisition will not drive immediate sales, I believe this strategy builds trust with customers and potential new customers as CrowdStrike ensures seamless integration across the platform rather than bolting on a new product, leaving it up to customers to cover the costs to integrate into the platform. Over time, when the data security tool is brought to market, I anticipate customer adoption to rapidly expand as the timing may align with my cloud-to-on-prem transition thesis. If this holds true, I expect that CrowdStrike should realize a significant upswing in sales for this feature in late eFY26.

Another factor that stuck out to me in their q4’24 earnings call was that management is growing their team for scale. Despite the potential macroeconomic headwinds that are currently setting in as future projects appear to be drying up, per ISM, management is taking the initiative to grow the firm and proactively expand their AI-related capabilities. This aligns with my overall cost-savings thesis relating to managing down opex by automating administrative tasks with GenAI. If this follows through, I believe the case for enterprises to switch to the AI-first security platform that CrowdStrike has to offer is even more compelling, as the security platform has the ability to ultimately lower the total cost of operating within the IT and security departments.

Though billings growth has raised many questions within the sellside analyst community across CrowdStrike and competing cybersecurity companies alike, I do not believe this metric is suggestive of future business as customers face exorbitant financing costs in this high interest rate environment. This is reflected in the firm’s balance sheet, as deferred revenue has increased by 30% from the previous year.

Corporate Reports

In terms of growth, CrowdStrike continues to grow their ARR at a strong rate, increasing 34% in q4’24. Though management anticipates a softer eq1’25 in terms of ARR, I do not anticipate this to necessarily foreshadow future growth as firms seek to minimize up-front costs to manage cash in this high rates environment.

Corporate Reports

Overall, management forecasts total revenue to grow by ~30% in eq1’25 with eFY25 growing within the same ballpark of 30%. I believe this level of growth can be sustained in the coming years as the firm expands on their data-centric security features and remains hyper-focused on securing the migration of AI applications both in the cloud and on-prem. To reiterate my case for CrowdStrike, I anticipate the single-platform solution to realize strength as enterprises will not need to purchase additional platforms to cover all AI-related applications. This plays in strongly to the case for companies in managing cash, capital investments, and operational expenses, or headcount. As management put it in their q4’24 earnings call, every $1 spent with CrowdStrike results in $6 in cost savings.

Corporate Reports

In terms of operations, I do anticipate some compression in the firm’s operating margin as management seeks to scale operations with additional headcount. Given the tightness in the AI/ML data science talent pool, I anticipate additional costs to work their way through the income statement as the firm may need to offer competitive bids for these highly qualified experts. Despite the slightly higher operating costs, I do anticipate that revenue growth will far outpace any additional costs associated with the increase in headcount, with the firm realizing strong growth in adjusted operating income.

In addition to this, I anticipate CrowdStrike to strongly benefit from their strategic partnership with Dell Technologies, as Dell is one of the leading server integrators for the next generation AI factories. As of q4’24, the partnership has garnished $50mm in total deal value, which I anticipate will continue to ramp as more firms adopt and integrate AI applications into their operations.

CrowdStrike is also collaborating with Nvidia to utilize Nvidia’s AI computing services on CrowdStrike’s AI-native CrowdStrike Falcon XDR platform to secure GenAI model creation. I believe that combining this with CrowdStrike’s partnership with Google (GOOGL)(GOOG) GCP will significantly bolster the firm’s hyperscaler security prowess when considering the heightened flow of data ingestion. This partnership should significantly improve the threat detection speed and a cybersecurity department’s ability to react to potential breaches.

CrowdStrike Valuation & Shareholder Value

Corporate Reports

CrowdStrike offers a compelling story that is reflected in their rich valuation of 28.36x price/sales. Despite being priced well above its competitors, CrowdStrike is the only firm to touch up on virtually all needs as it relates to securing the next generation of IT infrastructure and AI applications.

Corporate Reports

Considering my anticipated growth trajectory for the firm, I believe there remains a significant amount of value to be realized in CRWD shares. As competitors grapple with platformization and simplified solutions, CrowdStrike enables the features required for the cybersecurity department as an all-in-one, automated solution. I reiterate my STRONG BUY recommendation for CRWD shares, with a price target of $745/share at 23x price/sales.

Corporate Reports

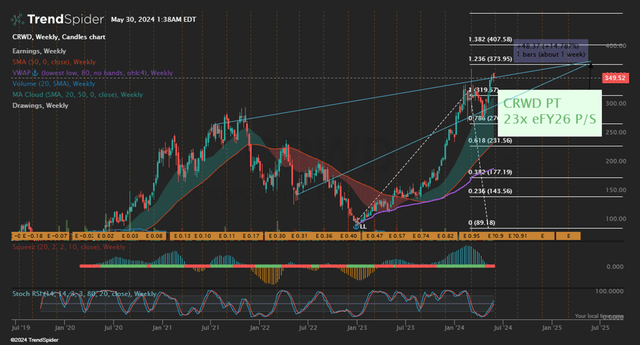

Looking at the technical chart, CRWD shares appear to be on an upward funnel-like trajectory as it nears this price target. Though shares may turn over in the near term, I do anticipate them to follow this path through next year.

TrendSpider

Read the full article here