Digital Turbine (NASDAQ:APPS) provides a platform for growth and monetization in the mobile ecosystem. They connect advertisers, publishers, carriers, and device makers through a full ad stack and proprietary technology. The company generates revenues from two main businesses, ODS/On-Device Solution and AGP / App Growth Platform.

ODS serves as a one-stop shop for pre-installed apps and curated content on new devices. Partnering with carriers and manufacturers, ODS delivers apps to users, earning revenue on installations and engagement.

AGP bridges the gap between app developers and brands/agencies. It provides a platform for targeted mobile campaigns across APPS’ extensive app inventory, allowing developers to reach relevant audiences and for APPS to earn revenue by facilitating these connections.

Share performance has been highly volatile. Having gone public in 2006 at a price level of $2, it went through extreme highs and lows, including reaching an all-time-high of over $85 in 2021. APPS has lost over 90% of its value since then, and currently, it is trading at around $3.8.

I initiate my coverage with a neutral rating. My modeled 1-year target price of $4.79 presents a projected 22% upside from today’s price of $3.9. However, despite the projected upside, uncertainty around the ad spend environment and partnership prospects are creating a lack of visibility into 2024, making the stock a very high-risk investment today, in my opinion.

Risk

Investing in APPS requires careful consideration due to several potential risks. Fundamentals, despite being decent today, have been facing moderate pressure due to multiple headwinds in recent times, ranging from lower advertising demand, and partnership churn, potentially threatening future outlook.

In addition, into the start of 2024, APPS will also expect a continuing headwind from lower device sales in the US:

Within our revenue guidance, we anticipate the headwinds associated with volume device declines to continue into Q4, principally on U.S. operators. While we believe future devices trends should improve, we’ve seen accelerating declines early in the March quarter, and at this time have limited visibility to the performance of the recent Samsung flagship device launch, and therefore we have further tempered our ODS volume expectations.

Source: Q3 earnings call.

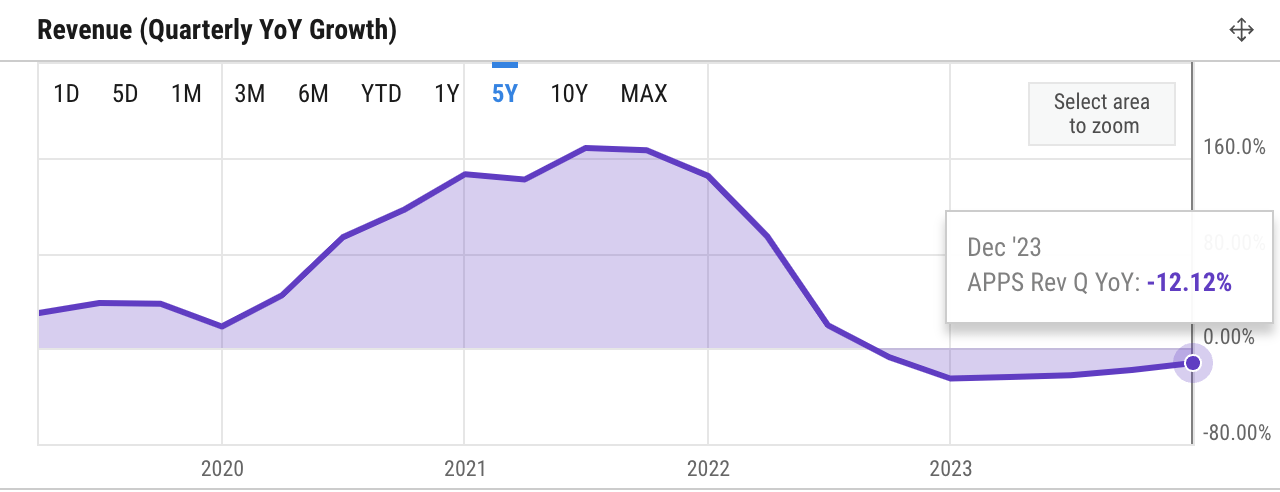

Revenue quarterly (YCharts)

Revenue growth has seen double-digit growth deceleration over the past year already. While it is understandable that the headwinds may be temporary, the magnitude of the decline highlights APPS’ relatively low resilience as a business and slow response to address underperformance, in my view.

In the Q3 earnings call, for instance, APPS did not only experience lower ad demand and partnership churn but also operational issues, which should have been a more manageable risk factor. This was brought up during the earnings call:

Hey, Bill, I just wanted to follow up on your comment about why the SingleTap trial wasn’t live. You talked about administrative issues. Can you give us a little bit more color on that when you expect that to be resolved? And then I had a couple of follow-ups.

Source: Q3 earnings call.

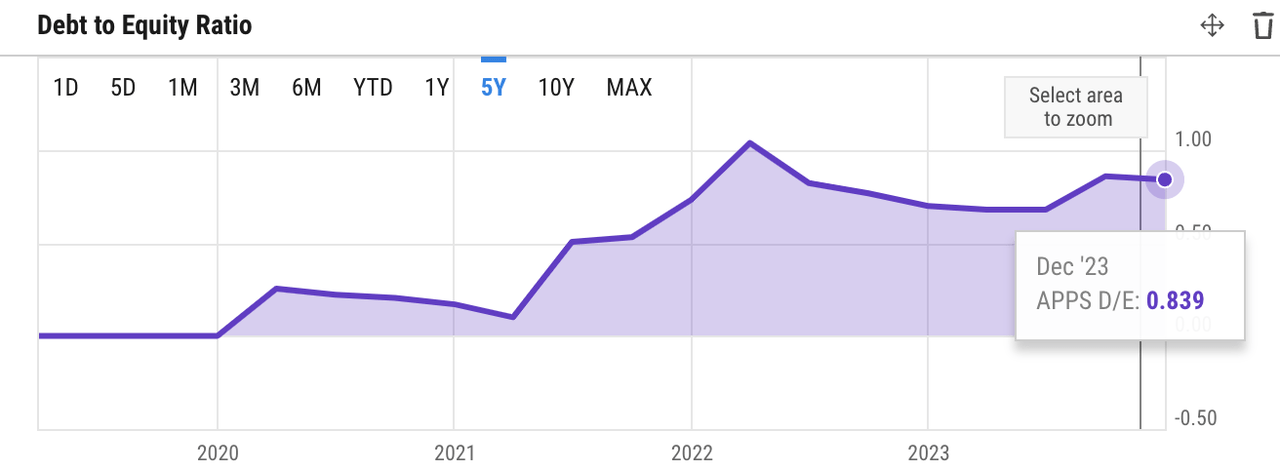

Debt to equity ratio (YCharts)

At the same time, the debt-to-equity ratio has remained elevated to 0.8x in 2023, almost 8x higher than two years prior, as APPS entered into a $600 million debt financing agreement sometime in 2021 under an elevated interest rate environment.

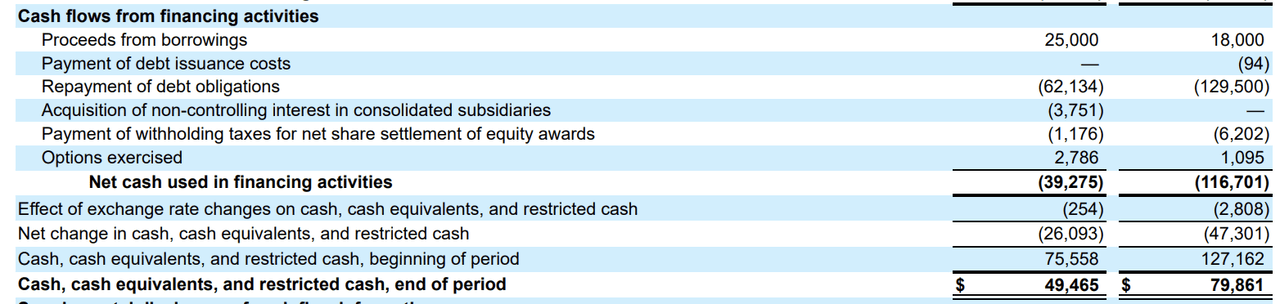

Cash position (10Q)

The elevated debt level may continue to threaten APPS’ future cash situation. The most use of cash has been the repayment of debt obligations. In Q3, cash level was down from $79 million to $49 million, over a quarter of its debt issuance in late 2021 already.

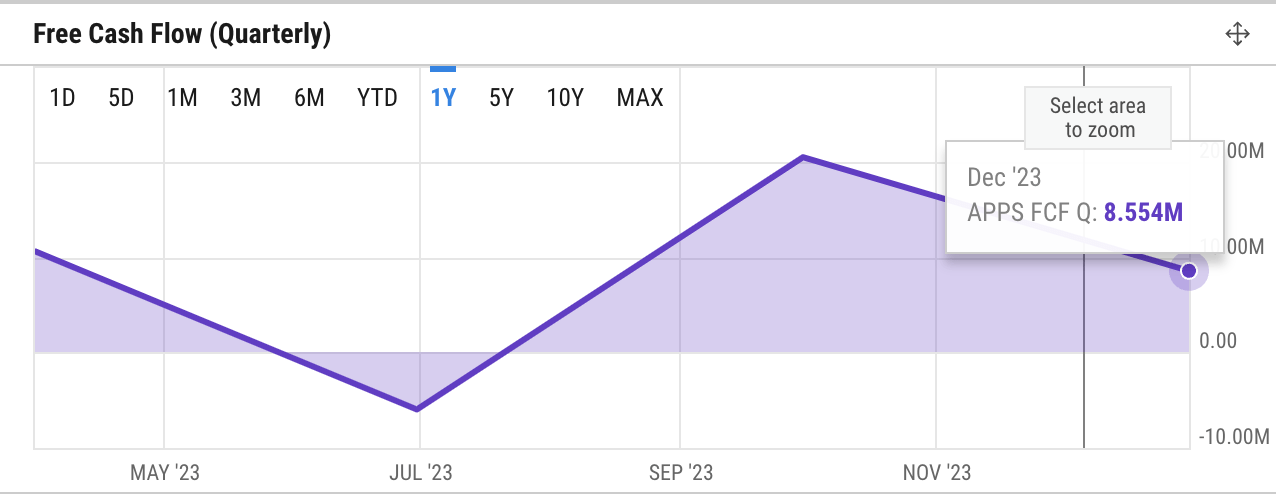

FCF (ycharts)

Though APPS has a proven track record of positive cash flow from operations/OCF and FCF, the overall cash generation has been moderately choppy. In addition, the slowing revenue growth presents uncertainty about APPS’s cash flow outlook in FY 2024, in my opinion.

Part of my concern is driven by what seems to be a pattern of persistent weakness in business partnerships. Revenue growth for both its business, ODS/On Device Solutions, and AGP/Apps Growth Platform, are largely driven by partnerships with third parties, such as telecom carriers or brand agencies.

In Q3 2024, we saw how APPS’ partnership terminations with an EU-based reseller and also a carrier resulted in a combined revenue loss of over $8 million. In the absence of these terminations, APPS would have seen a decline of only 7% instead of over 12% in revenue.

Revenue breakdown (10K)

Given that the same thing also happened almost a year ago when APPS filed its 10K in March 2023, it seems to be a pattern that investors may need to be aware of. At that time, annual revenue was down by over $80 million YoY, with $77 million of it driven by a termination of carrier partnership. In the absence of that, APPS would have seen a flat YoY annual revenue growth instead of a 16% decline.

As such, the seemingly heavy reliance on few, concentrated partnerships to drive revenue growth and then the pattern of weakening of the relationships itself, should present a red flag for investors.

Catalyst

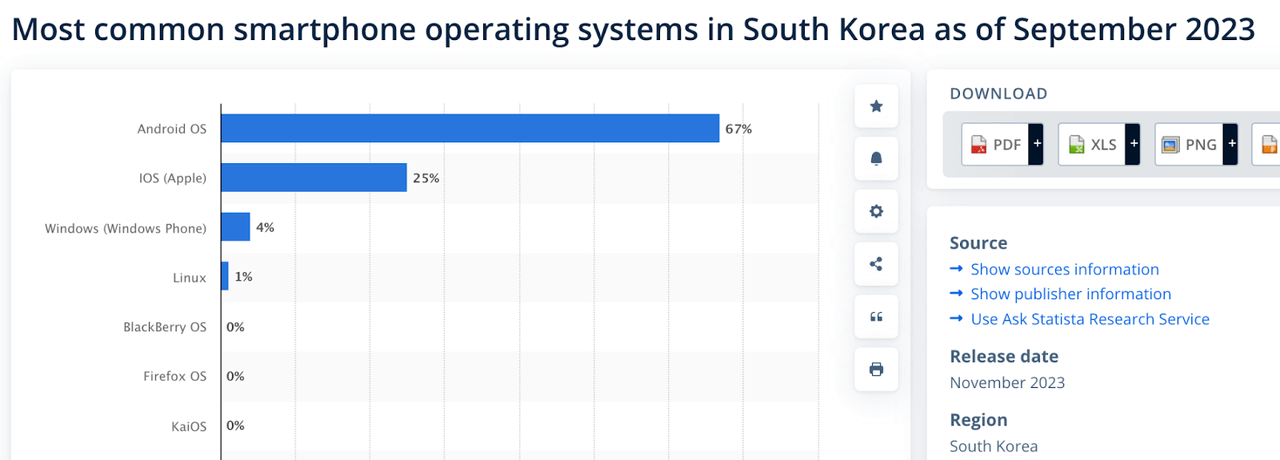

There are some catalysts for 2024, but in my view, their effect could be minimal. As a start, while APPS has inked a partnership with alternative app stores like Korea’s ONE Store, the impact may be limited. ONE Store, boasting higher revenue than Apple’s App Store in Korea, signifies an attractive partnership where APPS’ SingleTap offering integrated within their 40 million devices opens a new user base.

South Korea’s mobile marketshare (statista)

However, the magnitude of this catalyst is tempered by factors like potentially minimal market share of alternative OS, including Apple’s iOS, in Korea, leaving Android, which is used by its home-grown Samsung as the major player. Therefore, while ONE Store holds promise, its initial contribution to APPS’ growth might be smaller than anticipated, requiring further developments for a more substantial impact.

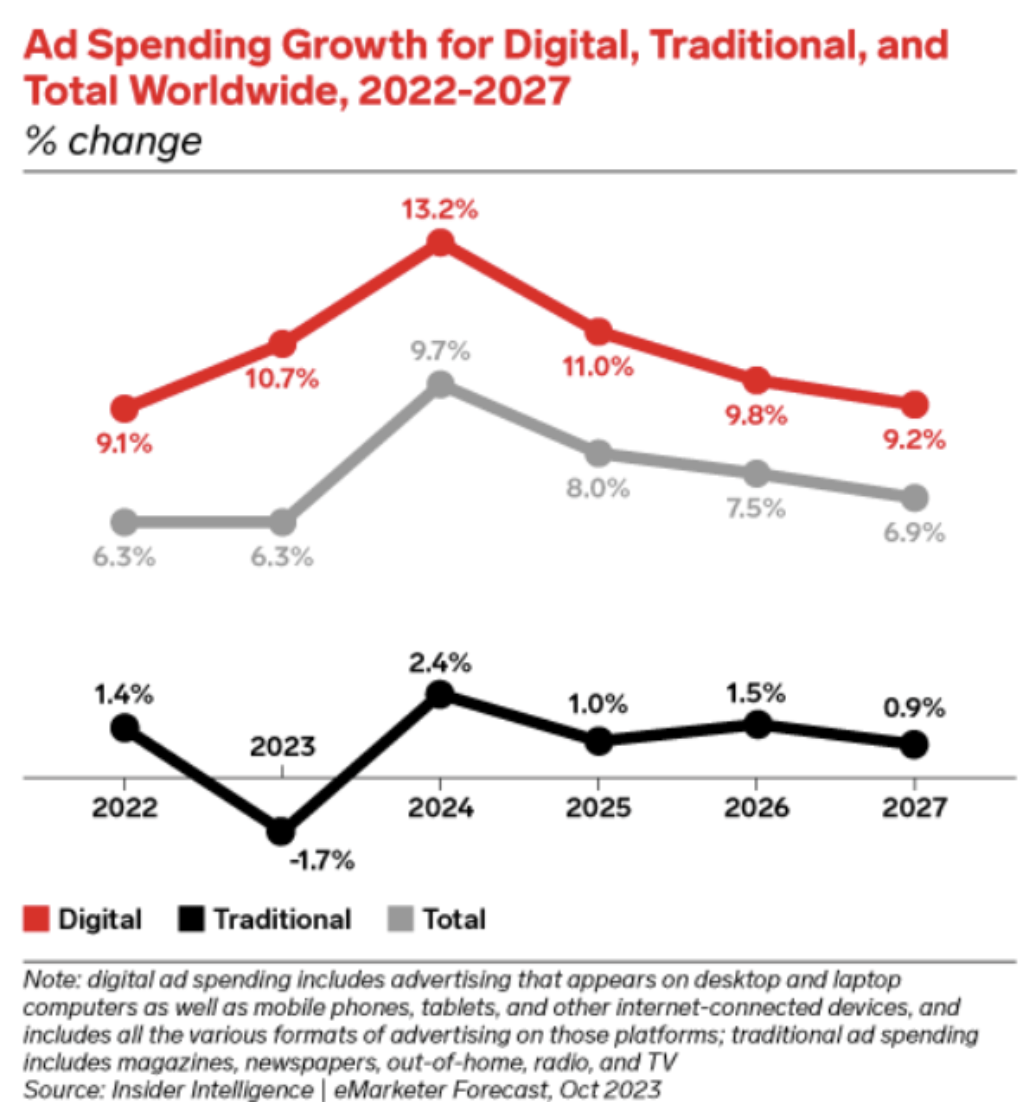

Ad spend growth projection (emarketer)

On the other hand, ad spending potentially bottoming out in 2023 could mean a rebound opportunity in 2024, likely driven by the Olympics 2024 and the US election. The improved outlook should benefit APPS’ AGS segment, potentially boosting not only revenue growth but also margin expansion.

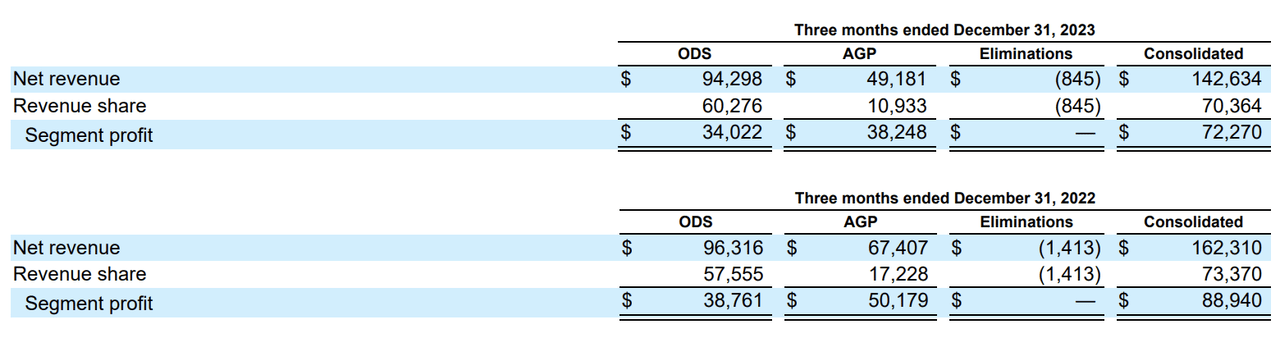

Revenue breakdown (10Q)

At over 77% gross margin, AGP is the significantly higher-margin business, despite only making up over 34% of the overall revenue. ODS’s gross margin, meanwhile, is just over 36%. With the limited visibility in ODS business in 2024, I would expect a rebound, if any, to be driven by AGP. In this scenario, I would project AGP’s share of revenue to increase from just 34% to probably somewhere above 40%, as it was a year ago at the end of 2022, lifting overall gross profitability.

Valuation/Pricing

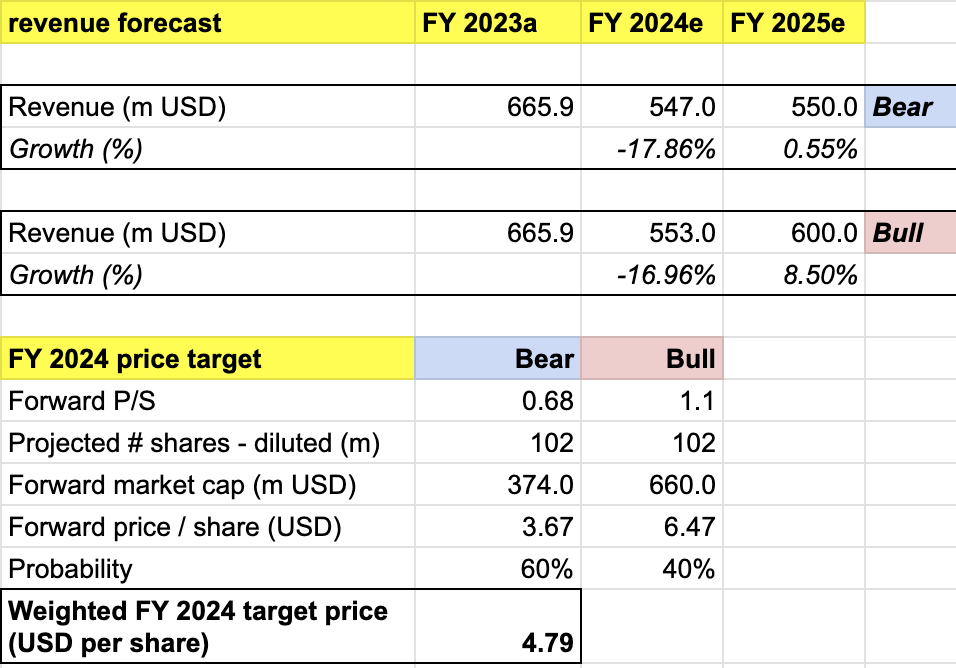

My target price for APPS is driven by the following assumptions for the bull vs bear scenarios of the FY 2025 (FY ending on March 2025) projection:

-

Bull scenario (40% probability) assumptions – APPS to achieve the high end of its FY 2024 revenue estimate of $553 million. I also project APPS to deliver 8.5% revenue growth and reach $600 million of annual revenue in FY 2025. I assign APPS a 1.1x P/S to reflect the valuation premium for successful execution in accelerating revenue growth, an expansion from 0.6x today.

-

Bear scenario (60% probability) assumptions – APPS to deliver a revenue of $547 million in FY 2024 and $550 million in FY 2025. I would expect APPS to face partnership-related and cash flow challenges. I assign APPS a P/S of 0.6x in this scenario, the level where it is trading today.

Price target (own analysis)

Consolidating all the information above into my model, I arrived at an FY 2025 weighted target price of $4.79 per share, suggesting a 22% upside from the current price level.

In my opinion, APPS remains relatively a high-risk investment. Despite the seemingly attractive upside, I would rate the stock neutral, advising investors to continue monitoring how the catalysts are shaping up into 2024, before making a decision.

Conclusion

Despite its potential, volatility defines APPS’ history, with the stock plummeting over 90% from the all-time high. While my model projects a 22% upside potential to $4.79 within a year, uncertainties around the ad spend environment and partnership prospects cloud 2024 visibility. Considering this lack of clarity and the high-risk nature of the investment, I initiate coverage with a neutral rating. This implies that while potential exists, the current risks outweigh the projected gains, making APPS a less than ideal choice for investors at this point.

Read the full article here