")

I last wrote about the SPDR Nuveen Bloomberg High Yield Municipal Bond ETF (NYSEARCA:HYMB) in late 2022. In that article, I argued that the fund’s key benefit were its tax-exempt dividends, with no significant advantages in yields, returns, or risk. The fund has matched the returns of its benchmark since, broadly in-line with expectations.

Right now, HYMB offers investors a reasonable, growing, tax-exempt 4.4% dividend yield. Although it is not a particularly high yield, it might provide comparatively strong after-tax income for some investors in higher tax brackets. I rate the fund a buy, although the fund’s investment thesis and benefits are very dependent on the specific circumstances of each individual investor. Consider your tax liabilities before investing in HYMB, or in other municipal bond funds.

HYMB – Basics

- Investment Manager: State Street

- Underlying Index: Bloomberg Municipal Yield Index

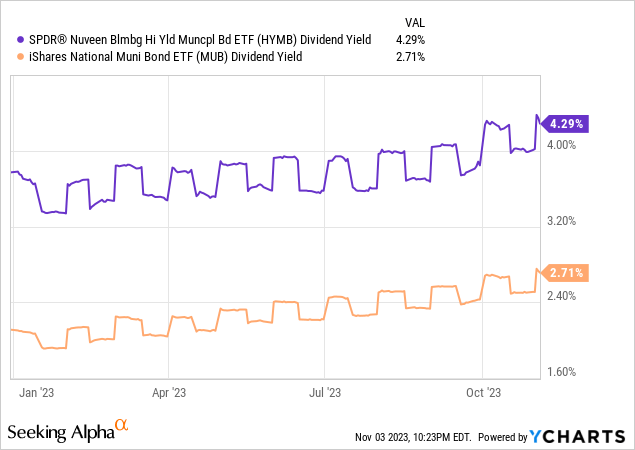

- Dividend Yield: 4.35%

- Expense Ratio: 0.35%

- Total Returns CAGR 10Y: 3.03%

HYMB – Overview and Analysis

Index and Portfolio

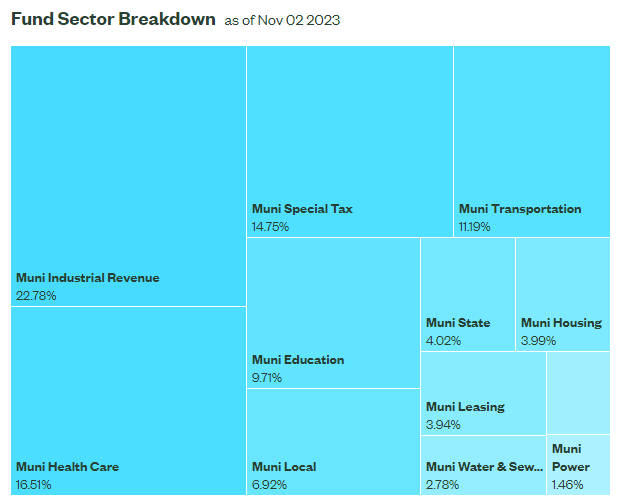

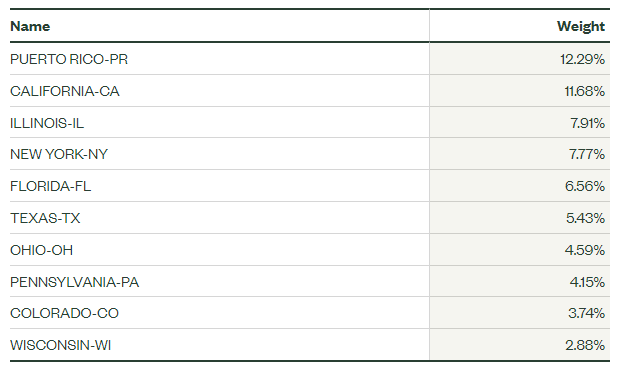

HYMB is a high-yield municipal bond index ETF, tracking the Bloomberg Municipal Yield Index (go to ‘About this Benchmark’ for details). It is a relatively simple index, including all dollar-denominated, tax-exempt, municipal bonds in the market, subject to a basic set of inclusion criteria. It invests in both investment grade and non-investment grade securities. HYMB currently holds over 18,000 securities, diversified across industries and states, more than sufficient diversification for a bond fund.

HYMB HYMB

Credit Risk

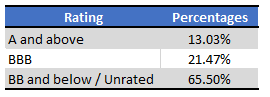

HYMB’s underlying index directly sets portfolio weights by credit ratings. Specifically, weights are as follows:

- 70% non-investment grade / unrated securities, so BB+ or lower

- 20% securities rated BBB

- 10% securities rated A

The above are index weights, actual fund portfolio weights are as follows.

HYMB – Table By Author

As can be seen above, HYMB’s credit ratings weights are similar to those of its index, with slightly greater allocations to investment-grade bonds. This is at least partly due to widening credit spreads, which have caused above-average price declines for most non-investment grade bonds.

Data by YCharts

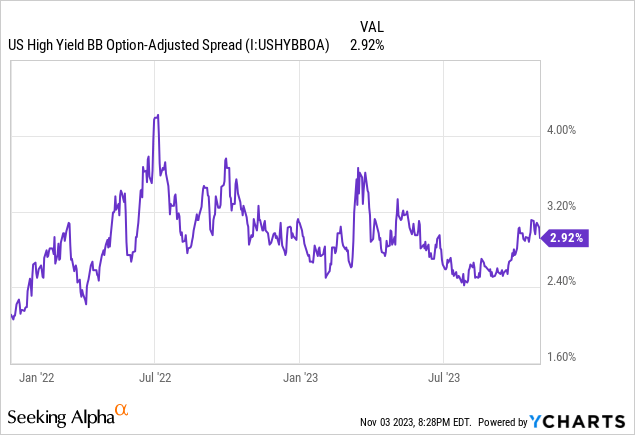

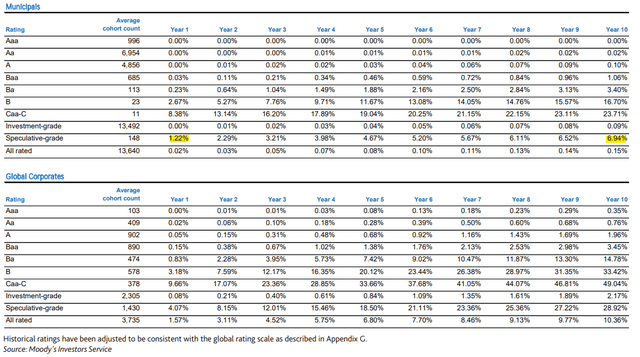

Although HYMB’s credit ratings are overall somewhat low, actual credit risk is extremely low, as municipal bankruptcies / defaults are extremely rare. As per Moody’s, default rates for non-investment grade municipal bonds range from 0.7% – 1.2%. For those rated BB, core to the fund’s portfolio, default rates range from 0.2% – 0.3%. Both figures are low on an absolute basis, and lower than those of corporate bonds with comparable credit ratings.

Moody’s

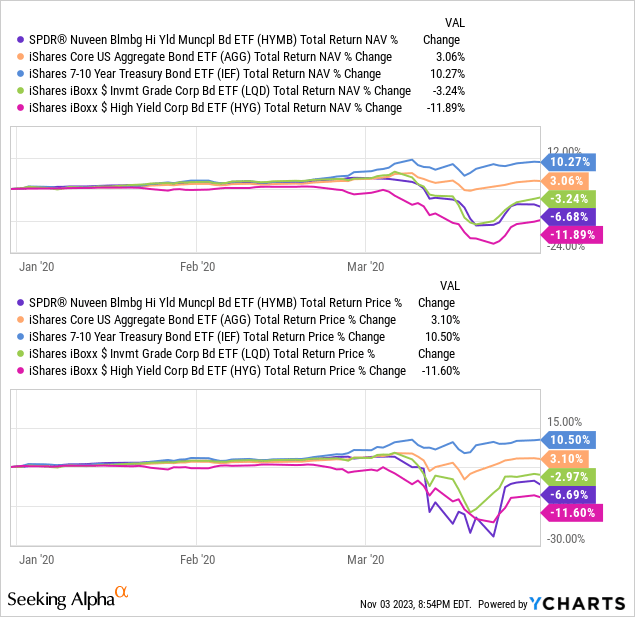

Considering the above, I think it is fair to say that HYMB’s credit risk is low, credit ratings notwithstanding. As such, the fund should see relative low losses during downturns and recessions. In reality, HYMB saw significant losses during the most recent recession in early 2020, during the onset of the coronavirus pandemic.

Data by YCharts

A significant portion of these losses were due to widening discounts, a rare occurrence for an ETF, but which do sometimes happen during periods of market stress. Losses were lower on a NAV basis, but still higher than average.

So, HYMB has low credit risk, but sees somewhat above-average losses during downturns and recessions.

Interest Rate Risk

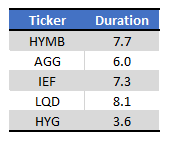

Municipal bonds tend to have long maturities and duration, and HYMB is no exception. The fund currently has a duration of 7.7 years, quite high on an absolute basis, but only slightly higher than average.

Fund Filings – Chart by Author

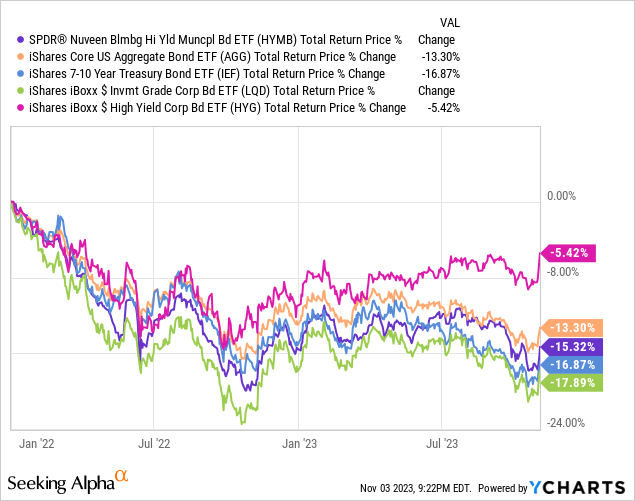

Above-average duration means above-average losses and underperformance when rates rise, as has been the case since early 2022. Underperformance was quite small, and some bond sub-asset classes performed even worse, however.

Data by YCharts

Flipside of the above is that HYMB tends to outperform when rates decrease. Excluding the pandemic, this was last the case during 2021, during which HYMB outperformed. As was the case above, differences in performance were quite small, and a few bond sub-asset classes performed even better.

Data by YCharts

HYMB has a bit more interest rate exposure than average, which increases risk, volatility, and losses when rates rise. The impact or differences here are all quite small, however.

Dividends

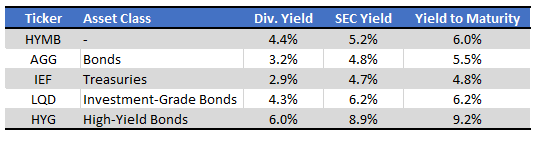

HYMB’s dividends are about average, across most relevant metrics. As is the case for most bond funds, trailing twelve-month dividend yields are quite low, at 4.4%, but more forward-looking dividend metrics are higher.

Fund Filings – Chart by Author

Although HYMB’s dividends are not particularly high, they do have one important advantage: they are exempt from most taxes.

Some context first.

Bond interest rate payments are (generally) taxable income, so investors must pay federal income tax on said payments. Said taxes are a burden for all investors, particularly for those in higher tax brackets. Avoiding these taxes is incredibly beneficial to investors, and investing in municipal bonds is one way of doing so.

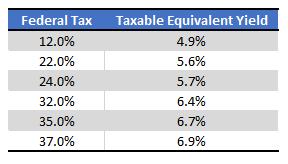

Investing in tax-exempt, low-yield municipal bonds can, sometimes, result in higher after-tax dividends than taxable high-yield bonds. One way of knowing if this is the case is through calculating a taxable equivalent yield to a municipal bond fund yield. So, for example, HYMB’s 4.4% dividend yield is equivalent to a 6.9% taxable yield for investors facing a 37% federal income tax. In other words, these investors receive the same income from a tax-exempt 4.4% yield and a taxable 6.9% yield.

Taxable equivalent yields for investors in other tax brackets follows:

Table and Calculations by Author

Although HYMB’s dividends are not particularly high, potential tax benefits are quite strong. Investors in higher tax brackets without access to tax-advantaged investment accounts might receive above-average after-tax dividends from the fund. As such, investors should consider their federal tax rate and attendant taxable equivalent yield when analyzing HYMB: the fund might make sense for tax-payers in the higher tax brackets, less so for those in the lower ones.

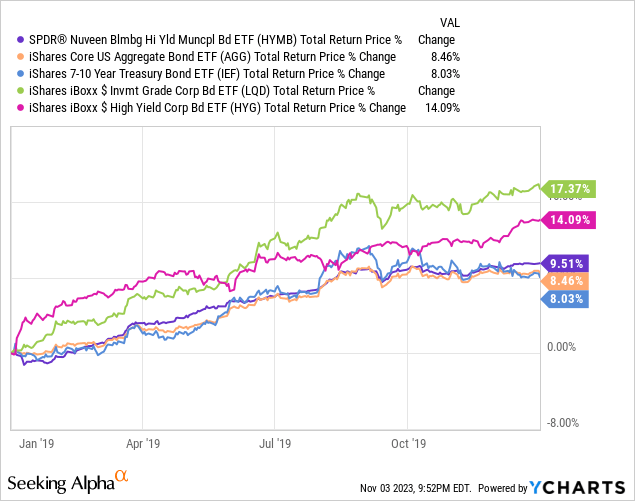

As a final point, HYMB does yield a bit more than broader municipal bond index ETFs. These securities tend to carry very low yields, due to their tax benefits, but the fund does try to focus on those with the higher (less low) yields.

Data by YCharts

Performance Track-Record

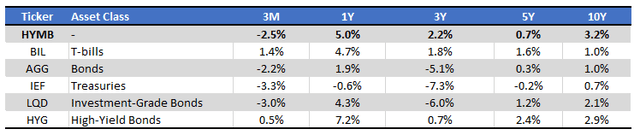

Finally, HYMB’s performance track-record is somewhere between adequate and above-average. The fund tends to outperform, although returns have been weak at the 3M and 5Y mark. Longer-term returns are low on an absolute basis, as interest rates were much lower in the past.

Seeking Alpha – Chart by Author

Overall, I do not think that HYMB’s performance is an important advantage or disadvantage for investors. Performance is adequate, as are most other metrics or fundamentals, but the fund’s most important advantage is its tax-exempt dividends.

Conclusion

HYMB’s tax-advantaged, growing 4.4% yield make the fund a buy.

Read the full article here