")

When are The Trade Desk’s Earnings?

The Trade Desk (NASDAQ:TTD) will report Q3 earnings after the closing bell on Thursday, November 9th. The company’s earnings calls are usually interesting and give great information. Interested investors can listen here or catch the transcript from Seeking Alpha here.

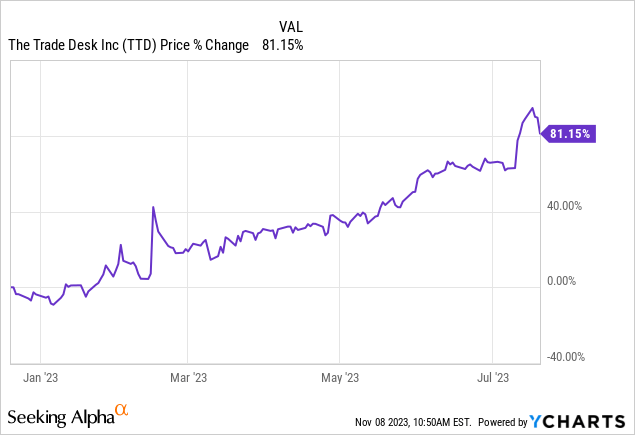

The Trade Desk has been a favorite of mine for a while and is a top-ten position. It was a Top Tech Pick of mine for 2023. I reiterated a buy in February and June before turning cautious and backing off to a hold rating in July after the mammoth gains shown below.

Since I turned cautious, the stock has held up reasonably well, losing 10% compared to the S&P 500’s 4%.

I also sold covered call options on my position in July, netting $14.8 per June 2024 $100 option. You can read about the reasons in the article here. The options are up 56% now, and the stock would need to rise 47% by June to make it a losing trade.

Three things to watch

The Trade Desk posted 23% year-over-year growth last quarter and expects the same this quarter. Will this be enough to move the stock higher?

1. CTV growth

As usual, all eyes will be on revenue growth and the gross spending of TTD’s customers, with connected television (CTV) as the main driver. The Trade Desk’s Video segment (which encompasses CTV, video ads on cell phones, and other similar advertisements) accounts for approximately 45% of sales.

CTV is also the fastest-growing segment due to the shift in ad dollars from traditional television to streaming television. For the first two quarters of 2023, The Trade Desk’s growth has outpaced the industry, which means it is gaining market share.

2. International sales

The Trade Desk has struggled to grow sales overseas meaningfully. Only 10% of its sales came outside of North America in 2022 and 12% so far in 2023. Meanwhile, the international market represents over 65% of the global advertising market. This makes it fertile ground for expansion.

There are opportunities for sustained growth here:

CTV advertising will only accelerate advertisers’ ability and appetite to fund this amazing new golden age of TV.

It’s also worth pointing out that this is an increasingly global trend. At Cannes this year, for example, we announced a new partnership with RTL, one of the largest pan-European media companies. Through this partnership, our international advertisers will have exclusive programmatic access to RTL’s addressable linear and connected TV inventory. We are starting with inventory across Germany, Spain, France, and Austria, with more European markets to follow soon.

This represents our most significant step yet into the European CTV market.

Disney announced today that they’ll roll out ad-supported models internationally for Disney+. We think that’s one of many opportunities around the world for us as it relates to CTV. So, the secular tailwinds just keep piling up, but very excited about all that.

Founder and CEO Jeff Green on the Q2 earnings call.

3. The company could beat expectations

There was an overall advertising slowdown in 2023 as many companies were budgeting for a recession. The recession has yet to materialize, and recent results from other companies are encouraging for the industry.

Amazon’s (AMZN) digital advertising segment posted 26% YOY growth, and the stock jumped after earnings (more on that here). Amazon’s advertising business is now 8% of total sales. Like The Trade Desk, Amazon’s ad solutions are terrific for discerning buyers focused on efficiency.

Alphabet (GOOG)(GOOGL) also posted strong YOY growth of 11%. Only 9% came from advertising; however, YouTube ad sales were up 12.5%. This is an encouraging industry trend.

Is The Trade Desk stock a buy?

The advertising industry is shifting away from traditional buys to programmatic. In programmatic advertising, a publisher (website, mobile, CTV publisher) sends bid requests for ad inventory. A demand-side platform (DSP) like The Trade Desk then bids on the inventory on behalf of its clients based on first-party data. It happens instantaneously, and the ad runs.

This type of marketing is more dynamic, efficient, and targeted. It also reaches consumers where they spend an increasing amount of time. This is why I like The Trade Desk when advertisers focus more on efficiency.

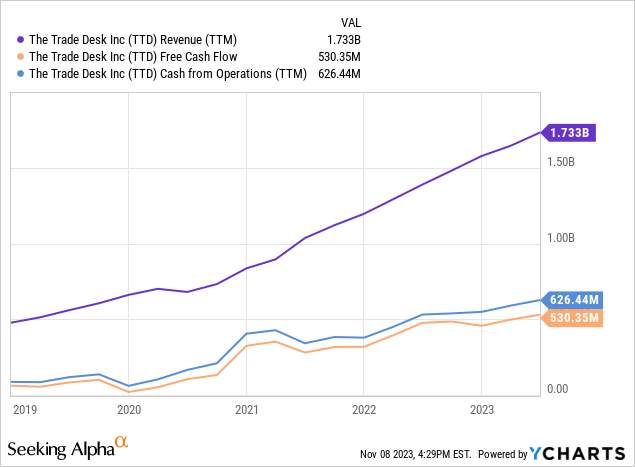

The company has been on a tear for years, increasing sales and cash flow.

It is also a high-growth company that is typically GAAP profitable.

The result is a terrific balance sheet with $1.4 billion in cash and investments and no long-term debt. Financial health and positive cash flow are critical to today’s growth stocks because high interest rates make taking on debt an expensive proposition. The Trade Desk is incredibly healthy financially.

The company has a bright future, but there are two reasons that I am cautious heading into earnings and do not have a buy rating on it.

First, the advertising market’s return to growth may be delayed. The recession never materialized this year, but this could keep the industry headwinds blowing longer. Many now believe it will come next year. Consumer spending is strong; however, sentiment is low, and credit card debt is at an all-time high. Something has to give.

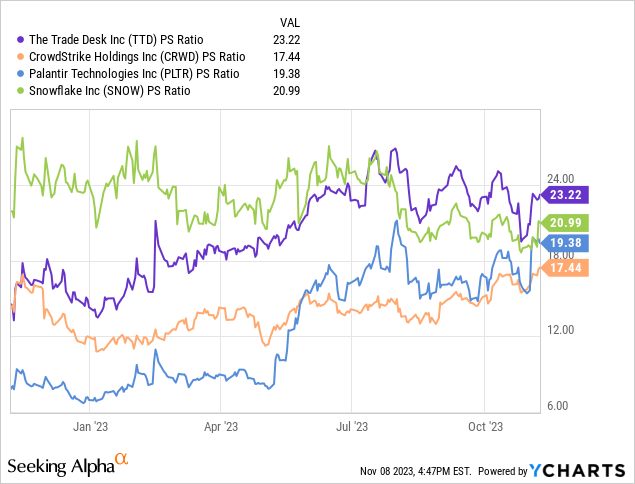

When I pinned The Trade Desk as a top pick, it had a price-to-sales (P/S) ratio of 15. It is up 50% since then to 23.

This is higher than fellow growth companies like Palantir (PLTR), CrowdStrike (CRWD), and even Snowflake (SNOW), as shown below.

Each company is unique, but The Trade Desk is an outlier operating in an industry seeing headwinds.

The company needs a monster quarter to justify a significant positive move. I love the company, but won’t buy shares at this price in this economy.

Read the full article here