")

At the end of last year, I published “M/I Homes: A Speculative Rally Built On Sand” regarding the homebuilding company M/I Homes (MHO). At that time, the stock was coming off of a massive rally from 2022 that sent it over 3X higher. The stock traded at $135 then and now sells for $124, 8% lower. That article was published within a few days of MHO’s current peak.

My outlook on MHO largely stems from my views regarding the macro economy and housing market. Although MHO has a decent managerial focus, I believe its stock is overvalued due to excessive investor exuberance and a misunderstanding of its naturally cyclical business. Without significant population and GDP growth, the housing market cannot rise indefinitely, mainly when home affordability and existing home sales are so low.

Like most builders, MHO reinvests most of its profits into new projects. While that practice has led to solid income growth in recent years, I believe it may leave it in a weak position as the market turns over. Much has changed over the first half of 2024, with a clearer indication that the boom in homebuilding profits is likely passing. While the stock may still not be a wise short opportunity, there seem to be greater indications that its bear market has begun.

An Updated Look At The Housing Market

The homebuilding industry is closely tied to the macroeconomic landscape. Most builders rise and fall together and are limited in their ability to avoid cyclical pressures. Thus, investors should not assume that immense income growth will continue as building demand fluctuates dramatically with the economic cycle. Given the home affordability crisis, this may be truer today than ever.

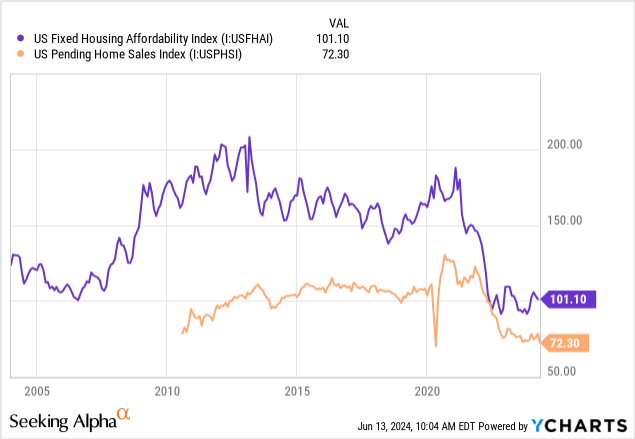

These measures have not changed dramatically over the past six months, although there are some indications that the cycle is reversing. First, affordability and pending home sales remain worse than their 2010 levels:

Home affordability is around where it was before the housing bubble crash in 2008. Existing home sales (not new) are also around 2009 minimal levels, indicating that market activity is generally weak. In most cities, home prices compared to incomes are higher than at the 2006 peak, exacerbated by much higher mortgage rates.

One main difference between now and then is that market volumes are lower, meaning only a small number of homeowners are certainly in unaffordable homes. M/I Homes is more focused on the more affordable market, with just over half of its customers being first-time buyers. It is also focused most on the Southeast, Texas, and the Midwest where homes are typically more affordable. Last quarter, its average home selling price was $471K, 17% above the median home price today ($420K). These figures are effectively similar, as we’re comparing an average and a median (as averages on this data will naturally skew high).

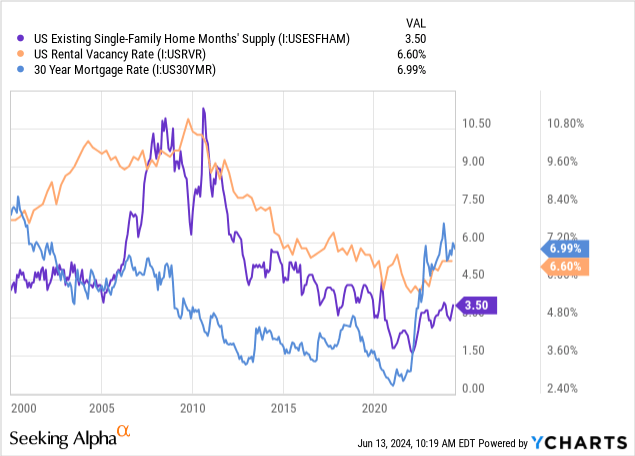

One driver of the homebuilding market’s stability despite low home sales is the abnormally low inventory levels of existing homes and reduced rental vacancy. Indeed, we can only expect home prices to decline if inventories are sufficiently high and rising, which has not been the case, but that may be changing. Following mortgage rates, there is a more significant increase in SFR inventories and rental vacancies. See below:

Rental vacancies and SFR inventory are still low compared to 2006-2008. I think they’re naturally lower because of internet-based technological improvements (such as Zillow) that have led to a faster time between home (or rental) listing and closure. For the same reason, it may be possible that inventories/vacancies will rise at an abnormally fast pace, though that has not yet been the case.

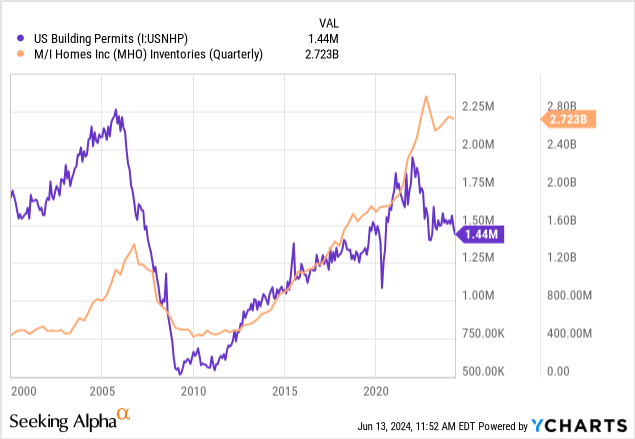

Nationally, building permits have likely peaked and are now headed lower, though they are still above their typical levels for this housing cycle. M/I has leaned into the building boom and has significant outstanding inventories, seeing a lower decline than the overall drop in building permits. See below:

Again, I would not say this situation is as bad as in 2006-2008 because M/I’s inventories are only slightly elevated compared to its sales. Still, I think the data points toward the company building into a glut that may become more apparent as the general economic data becomes more evident. The company’s contract backlog is essentially unchanged YoY but well below its 2022 level, again pointing to a demand peak.

The most significant red flag for homebuilders would be a rise in unemployment, which would have considerable negative cascading consequences for new home sales demand. A large portion of people financed homes at lower rates and prices, so they cannot necessarily afford to move and buy again at today’s much higher prices and mortgage rates. Thus, a rise in unemployment (which can force moving) would likely catalyze a significant decline in the housing market by increasing inventories in today’s low-demand market (as seen by pending home sales).

Unemployment did rise last month, though it remains historically low. Problematically, we cannot necessarily rely on the official government labor data. In recent years, a gap has grown between the establishment and household employment surveys. The government looks to the establishment survey, and though it is often seen as more accurate, there is debate on that point. The most recent data shows that unemployment may be notably higher than the official data suggests. Notably, Fed Chair Jerome Powell recently noted, “There’s an argument that they (jobs data) may be a bit overstated, but still, they’re strong.”

Although not specifically important for M/I, this is one tell-tale sign that the US economy is not as strong as some headlines suggest. That said, I also do not believe it is so weak that a crash is necessarily around the corner. M/I may still have time to deleverage to avoid potentially having excess inventory in 2025-2026.

What is MHO Worth Today?

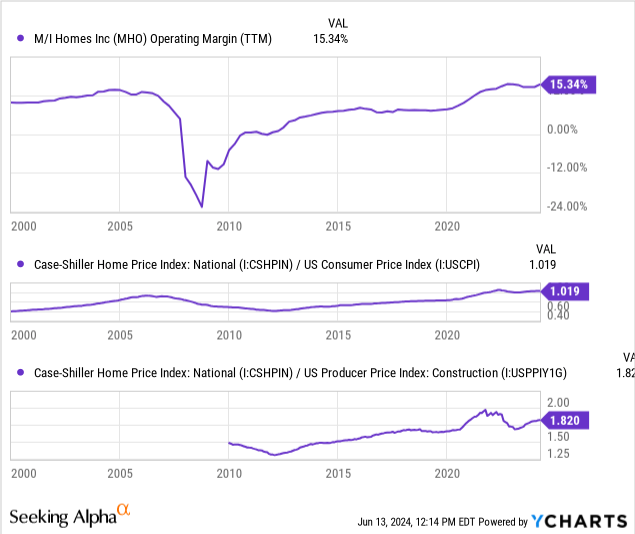

As home inventories and vacancies rise, I expect we will see a decline in home prices. If inflation remains sticky, it may be that home prices do not fall but that other prices, such as construction costs, rise faster. To a degree, M/I’s operating margin is correlated to the ratio of home prices to consumer prices or home prices compared to construction costs. Both figures are elevated today compared to historical levels, indicating home prices are as overshot as they were in 2006. M/I’s operating margins were similarly elevated at that time. See below:

The noticeable difference between now and 2008 is that fewer people who own homes today bought them at today’s extremely low affordability levels. To me, that makes it unlikely that we will see the same degree of rapid declines in the home financing market as then, which caused home prices to fall too far, too fast. However, I expect home prices to drop compared to costs over the course of one to three years.

Again, without a considerable rise in unemployment and a general economic dislocation, I only expect a normalization of M/I’s profit margin from its TTM 15% back to ~7% to 8%. The company has negligible interest costs, which should result in a ~40-50% reduction in its operating income. After accounting for that and taxes, I project its longer-term annual income will be closer to $200M. By that estimate, its forward “P/E” is around 17.5X. That may be manifested by 2025 at the earliest, but potentially not until 2028, depending on whether or not the US economy is slowing and how the Fed reacts to that. Specifically, whether or not the Fed ends or reverses its QT policy on its mortgage assets, as that may be pushing mortgage rates higher today.

The Bottom Line

Compared to the last time I covered MHO, I believe the homebuilding and single-family residential market cyclical decline will be slower than I previously anticipated. However, given the rise in home inventories, it seems even more certain that the cyclical peak for SFR homes has passed. To me, that points to a normalization of MHO’s operating margin, stemming from a prolonged relative decline in new home prices compared to MHO’s costs.

Again, as I know I’ll face some comments on this point, I am only estimating a normalization of market conditions from the Goldilocks environment of ~2021. I am not predicting a 2008-like crash. If so, I would see MHO as a short bet, as its profits would quickly turn into losses in that environment. Although my outlook for MHO remains bearish, I do not see it as a short opportunity. I do not currently believe there is sufficient data to point to a large housing market crash, only a return to more sustainable conditions.

Put simply, I do not see how homebuilders can continue to sell homes in a record unaffordable market without eventually seeing negative headwinds. In my opinion, MHO is currently valued as if this trend can continue forever, forgetting that homebuilders are highly cyclical.

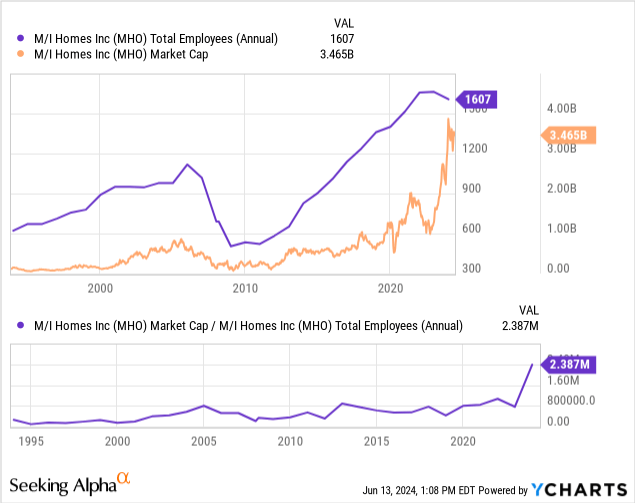

Like most homebuilders, MHO derives the bulk of its long-term value from its employees. Although the measure is imperfect, we can only expect a certain amount of income per employee over the long run across the economic cycle. Today, that figure is high, but it may be much lower next year. Thus, I think it’s reasonable to value MHO based on its relative employee count. See below:

MHO’s market-cap-to-employee ratio has generally been stable throughout its history, sustaining a normal level of ~$700K prior to the recent boom. However, its employee count actually declined in 2023, indicating the company’s prospects had begun to reverse.

We could reasonably make some inflationary adjustments to this metric and also account for retained cash from profits. However, I think the rate of increase to this metric is yet another indication of its overvaluation. In my opinion, a $2.5B valuation is more sensible, relating to a forward “P/E” of 12.5X based on my $200M long-term income outlook. That would relate to a market-cap-to-employee ratio of ~$1.55M, which seems more reasonable than its current level.

As such, my share price target for MHO is $90. That said, in the event of a recession, I expect MHO to decline further than that, depending on how the broader financial markets react. Of course, it is also possible that MHO’s prospects will rebound should mortgage rates decline significantly and renew stability in the homebuilding environment. Although I believe that is unlikely, it would cause my bearish outlook to shift if mortgage rates were back below 4%.

Read the full article here