")

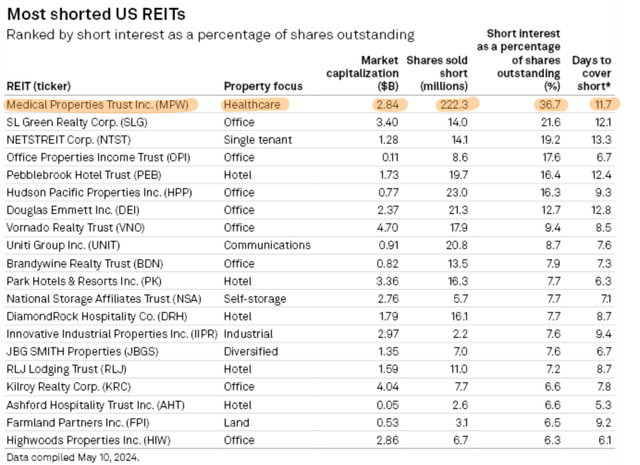

After falling roughly 80% from its all-time high in 2022 but up since I last covered the ticker, Medical Properties Trust (NYSE:MPW) has seen its largest tenant, Steward Health Care System (“SHCS”) file Chapter 11 bankruptcy. The REIT now faces a materially different investment reality over the next half year. MPW is the most shorted US REIT, with 222.3 million shares short, around 36.7% of its weighted average shares outstanding. S&P Global Market places this short interest rank roughly 1500 basis points ahead of the second most shorted REIT, SL Green Realty (SLG). The healthcare REIT held $17.4 billion of total assets spread across 436 properties consisting of general acute facilities, behavioral health facilities, and post-acute facilities as of the end of its fiscal 2024 first quarter.

S&P Global

This bankruptcy filing was an inherent salvo for the bears, but MPW is intensely undervalued, even against the bankruptcy of SHCS with the REIT reporting first-quarter normalized funds from operations (“NFFO”) of $0.24 per share, around $0.96 per share annualized for a 17.8% NFFO yield. MPW is now swapping hands for 5.6x times its annualized NFFO, expanding from when I last covered the ticker. The REIT last declared a quarterly cash dividend of $0.15 per share, kept unchanged from its prior quarter and $0.60 per share annualized for an 11.2% dividend yield. MPW is covering its dividend by 160%.

Global Debt Maturities, Liquidity, Summer Rate Cuts, And SHCS Hospital Sales

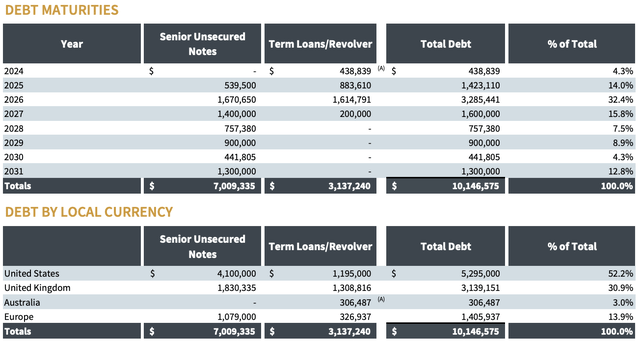

As of the end of its first quarter, MPW held a total debt balance of $10.17 billion, at a weighted average interest rate of 4.159% with $438.84 million, around 4.3% of the total, coming up for maturity in 2024. The REIT has been extremely active on the disposition front, selling five hospitals in California and New Jersey for $350 million post-period end. The REIT also sold a 75% interest in five Utah hospitals for $1.1 billion in April to place management on track to meet their target for $2 billion in total incremental aggregate liquidity in 2024.

Medical Properties Trust Fiscal 2024 First Quarter Supplemental

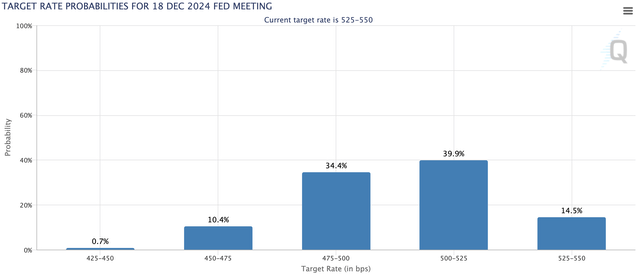

This has been used to aggressively reduce debt by $1.6 billion, with the 2024 maturity fully addressed. Further, Europe is set to lead the way with interest rate cuts, placing MPW on a path to see the cost of funds for its global-denominated debt start to reduce. The UK forms 30.9% of MPW’s debt, and the Bank of England is now widely expected to start cutting rates from the June meeting from its current 5.25%. The European Central Bank already started cutting base interest rates in June. The Fed will take more time with the CME FedWatch Tool pricing in, the Fed only beginning rate cuts towards the end of the year at the November FOMC meeting.

CME FedWatch Tool

The ongoing SHCS hospital sale process is core to MPW’s bullish thesis, as a potential summer short squeeze with management flagging during the first-quarter earnings call, that the process should allow them to replace SHCS with better-qualified operators. Hence, MPW is pushing towards a new zeitgeist, where the SHCS overhang will be removed, even as the REIT is set to extend up to $275 million in debtor-in-possession financing to SHCS. This will provide MPW with a senior position in the SHCS capital stack, with the REIT also guiding to exit 2024 with a significant liquidity base on the back of its $800 million refinancing of its UK hospital portfolio.

Becker’s Hospital Review

SHCS received approval from its Bankruptcy Judge on the 3rd of June to proceed with its aggressive timeline for the sale of its 31 hospitals and other assets. This is being completed in two tranches, with the first tranche set to have a bid deadline of June 24 and the first hearing on the 11th of July. This tranche will include the physician group and all of SHCS hospitals, excluding all of its Florida hospitals and some hospitals in Texas. The second tranche has a bid deadline of the 12th of August and a sale hearing ten days later, on the 22nd of August. This tranche will include all Florida hospitals and the remaining four of its Texas hospitals.

The conditions for a sustained short squeeze are shaping up in the summer. This quarterly dividend is set to be maintained on the back of strong coverage, as the ongoing sale of SHCS hospitals will help MPW diversify its portfolio across stronger operators, forever eliminating the counter-party risk of SHCS and delivering the conditions for the REIT to start growing FFO. The bankruptcy could turn out to be a silver lining for the overall risk profile of the REIT, helping reduce the risk premium required and driving the yield lower to the high single digits. I’m adding to my MPW position against this, with several catalysts set to play out through summer, starting from the Bank of England base rate cut. The large short interest seems odd against this, with the delay in filing of the first quarter form 10-Q broadly a non-story, as it was driven by the sudden disruption caused by the SHCS bankruptcy filing. There is a risk here of further delays, but MPW is a long-term position on the safe dividend yield and strong outlook for recovery.

Read the full article here