")

Introduction

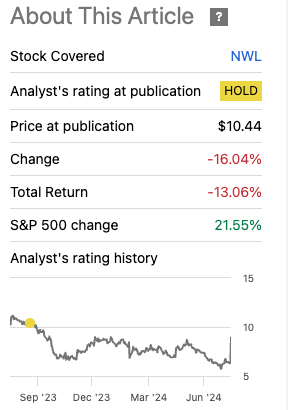

Newell Brands (NASDAQ:NWL) has recently reported Q2 ’24 earnings, which the market loved, sending the company’s share price up 40% as investors believe the turnaround is well on its way. Even after such a run-up in share price, the company still underperformed the overall market since the first time I covered it back in August last year. Today I wanted to take a look at the results and what can help it turn around going forward. The company still has a long way to go and needs to prove it can continue to improve going forward. I stand by my hold rating yet again.

1-year Performance

Q2 Numbers

The company’s top line came in at $2B, down -7.8% y/y (core sales down -4.2%) and a miss of $50M. Non-GAAP earnings per share came in at an impressive $0.36, a huge beat of $0.15. To note, the reason the company saw such a beat was because it realized a tax gain a quarter earlier than expected.

In terms of margins, we can see that whatever management has been doing over the last year has been paying off tremendously. Q2 reported gross margin improved by 590bps to 34.4%, while normalized gross margin improved by 490bps to 34.8%. Operating margins saw a 260bps improvement compared to the prior year, while normalized margins saw a 170bps improvement, now standing at 10.8%.

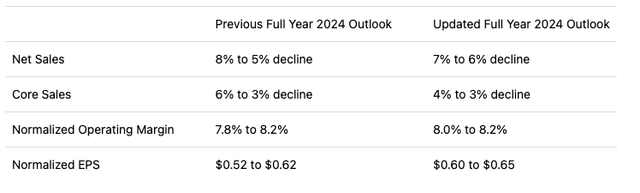

On the back of these results, the company raised its full-year 2024 outlook, narrowing the ranges:

Seeking Alpha

In terms of the company’s financial health, NWL managed to pay down some debt since the end of 2023, $500m to be specific, which should alleviate some of the interest expense pressures. Despite the lower debt amount, the company’s interest expense increased by $2m y/y due to persistently high interest rates. Furthermore, Moody’s Corporation (MCO) downgraded NWL’s debt rating throughout the year, with the latest downgrade coming in on February 9, followed by a downgrade just a few days later from S&P Global (SPGI). These downgrades have increased the annual interest expense by around $39m a year. So, if the company’s financial situation continues to improve, by paying down debt, the interest expense burden should start to come down. To me, the company’s debt pile is still rather significant, standing at around $4B, while its interest coverage ratio as of Q2 ’24 stood at just about 2x, which is what analysts say is sufficient, but it’s too close for comfort to me, which means I would need to have a decent margin of safety when calculating the company’s intrinsic value.

Overall, I think the slowdown in revenue declines and an impressive margin improvement is a step in the right direction, coupled with an improved 2024 outlook, the company’s share price saw over 40% increase on the day of the release. Investors liked what they heard, and the turnaround is now much more plausible than it was just a year ago, and the market seems to agree. I don’t think it warranted such a reaction on the day, but because the company was so down in the dumps, any positive news was going to be very bullish.

Comments on the Outlook

So far, sales in the Home and Commercial, and Outdoor and Recreation segments continued to see declines, while Learning and Development came in flat y/y with a decent improvement in margins. A ray of hope that the company is starting to see a turnaround.

So, this was enough to send the company’s share price to the moon. What has the company been doing and what will it continue to do to help improve its top-line growth? With the introduction of the organizational realignment strategy on top of the Realignment plan of 2023, the company is going to focus its efforts on the best-performing brands and “disproportionately invest in innovation, brand-building, and go-to-market excellence” for their best brands and most profitable geographies. The new CEO has been hard at work since being appointed, which is a very promising sign in my opinion. The strategies implemented are starting to bear fruit, however, it is still rather early stages, so I don’t expect to see huge changes over the next couple of quarters, although the margin improvements have been fantastic. Further investments in the company’s best brands according to the management should turn positive in the near future, but that remains to be seen.

As for margins, we are close to what the management expects its long-term margin profile to look like. In the latest transcript, the CEO Chris Peterson said that the company’s long-term gross margin goal is 37% to 38%, which he believes is achievable. And how does the company aim to achieve such margins? Well, the One Newell Approach is still the overarching theme of the company, the company aims to continue to streamline its operational efficiency through a reduction in SKUs, streamlining the company’s real estate, and centralizing its supply chain functions. On the latest transcript mentioned above, the company is meaningfully reducing its dependency on China and is aiming to reduce it to 10% over the coming quarters. This means that the company will likely avoid any further increases in costs if China is going to get hit with more tariffs going forward. So, it seems that Project Phoenix, which was implemented at the beginning of 2023 has been working well and should have been fully implemented by the end of 2023. We can see the impact of the strategy on margins clear as day. If we take management’s long-term outlook at face value, which probably isn’t ideal, there is still another 800bps improvement to be had on gross margin over the next few years, which is outstanding. But as I said, that is what management expects and there could be a lot of unexpected issues over time, therefore I am taking these comments with a grain of salt. Nevertheless, let’s look at an updated valuation.

Valuation

For revenues, there isn’t a lot of information to gauge how well the strategy is going to work out in the end, however, for the sake of forecasting, I decided to go with around a 7% decrease in top-line for FY24, as per management’s updated numbers, -2% for the following year, flat for FY26 and a slight bounce in FY27 that will taper off to 2% growth by FY33, giving me an overall CAGR of 2% over the decade. As per below.

Author

For margins, I decided to implement what management expects its long-term margin profile to look like, but the company will not reach 38% by FY33, only 37% to keep it safe. Below are the assumptions and progress of gross margins that lead to a doubling in operating margins over the next decade.

Author

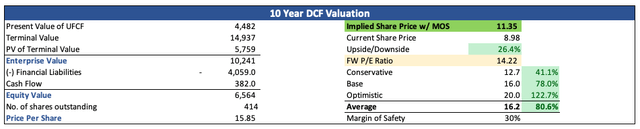

To keep it on a much safer end, I went with 10% as my discount rate instead of the company’s very low WACC of around 5%. This way, I am giving myself more room for error in the estimates above. I am also going with 2.5% as my terminal growth rate because I would like the company to keep up with the US long-term inflation goal. Furthermore, I am going to add another 30% discount to the final intrinsic value calculation due to the company’s still high levels of debt and the uncertainty of the turnaround itself. Better be safe than sorry. With that said, NWL’s intrinsic value is around $11.35 a share, meaning, the company is trading at a discount.

Author

Closing Comments

The above fair value of the company depends on management’s ability to continue to improve its margin profile considerably, 700bps over the next decade, to be exact. Is it possible? I think so, if the massive y/y improvement is any indication, however, I am still going to continue to be on the fence. The reason is that I would like to see a few more quarters of results before concluding that the company’s margin profile is progressing in the right direction, and we will eventually see 37% to 38% in the long term. Furthermore, I would like to see how the company’s top line progresses going forward and whether it will manage to eke out a positive percentage over the next few quarters or not.

In the meantime, I will continue to monitor the situation and will update my model accordingly.

Read the full article here