")

Investment Outlook

Olo (NYSE:OLO) recently reported its Q2 2024 financial results, beating revenue and matching earnings estimates.

I previously wrote about OLO in February 2024 with a Hold outlook due to operating losses and worsening operating cash flow.

Revenue continues to grow, and operating expenses are dropping, but the forward outlook for a demand-challenged restaurant industry is deteriorating, and the stock appears fully valued here.

I remain Neutral (Hold) on OLO for now.

Olo’s Market and Approach

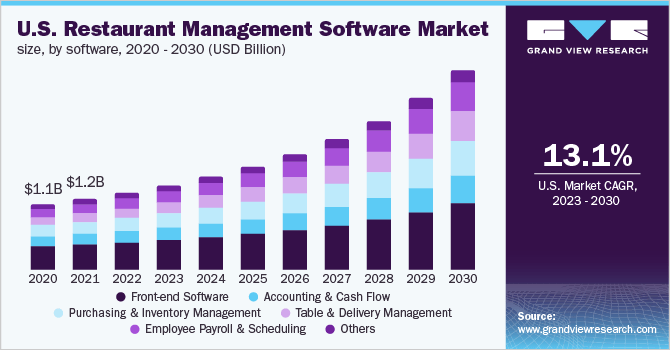

The worldwide restaurant management software market was an estimated $4.6 billion in 2022 and is expected to exceed $15 billion by 2030, per a market research report by Grand View Research.

If reached, this growth in demand would represent a CAGR of 16.3% from 2023 to 2030, which is a very strong growth rate.

The U.S. restaurant management software market is forecasted to grow at a slightly slower CAGR of 13.1% through 2030.

The chart below from Grand View Research illustrates the expected growth trajectory for various segments within this large market:

Grand View Research

The global pandemic pulled forward significant demand for restaurant takeout ordering, digital presence, and marketing to consumers, which increased the need for both point solutions and integrated software solutions from vendors.

The table and delivery management sector is expected to increase at a CAGR of 18.6%.

Olo’s focus has been to offer an integrated software system to enable online ordering, search and social integration, along with order management, kitchen order display and order dispatch that integrate with in-house or third-party delivery services.

The company also recently added its Olo Pay transaction processing service integrated with its full-stack and has seen continued growth in the use of this functionality.

Recent Financial Trends

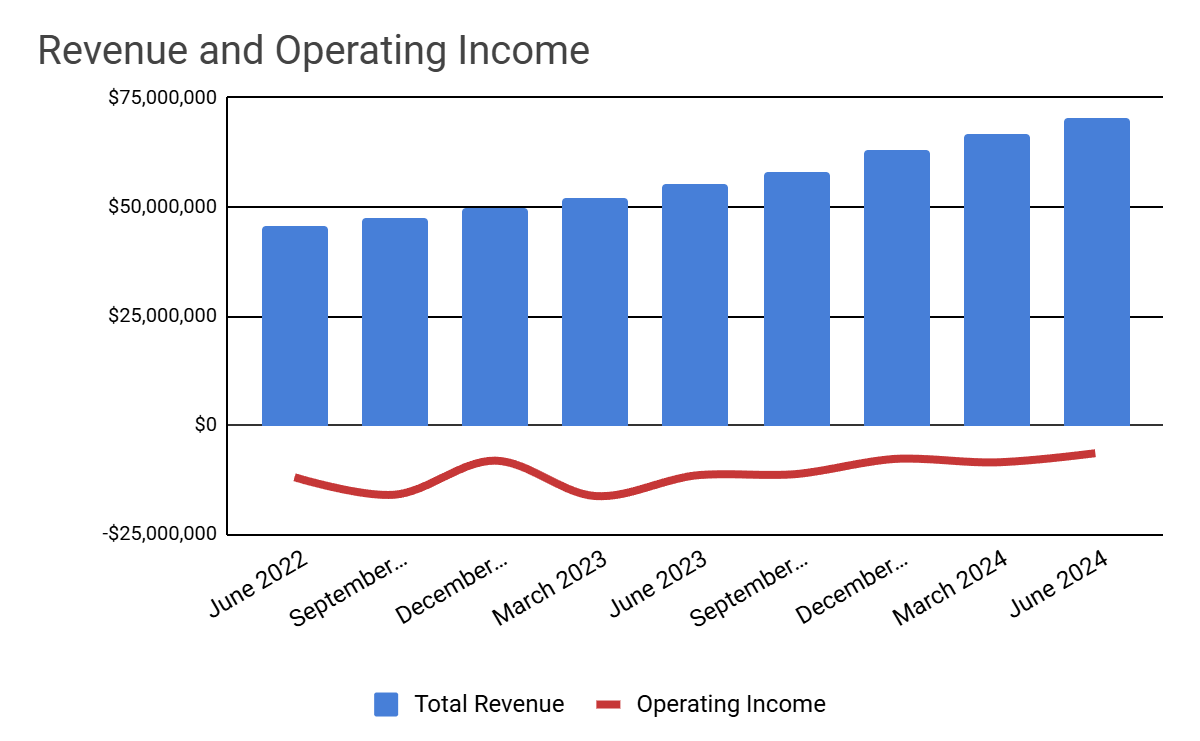

Total revenue by quarter (columns) has continued to rise, growing 28% year-over-year due in part to higher ARPU by 19%. Operating income by quarter (red line) has improved because of increased contribution from its Olo Pay system and reduced operating spending.

Seeking Alpha Data

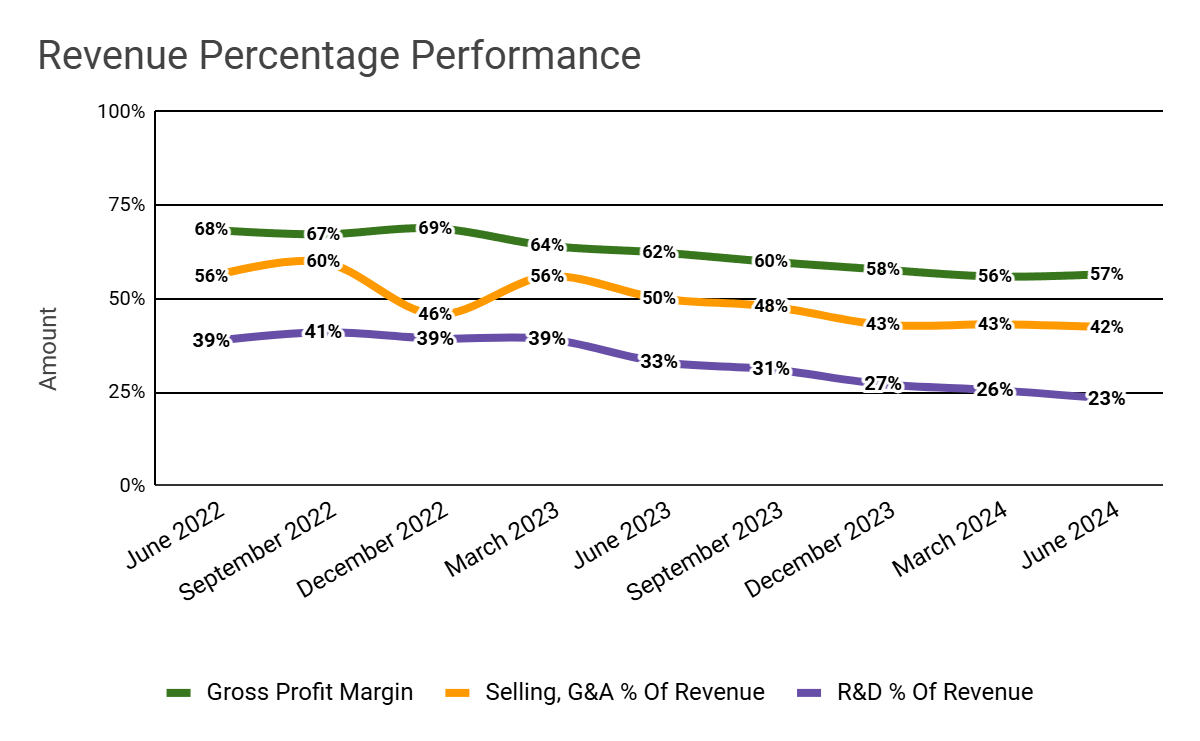

Gross profit margin by quarter (green line) has trailed lower as a result of a revenue mix shift as Olo Pay increases activity. Selling and G&A expenses as a percentage of total revenue by quarter (orange line) have trended lower due to reduced compensation expenses. R&D expenses as a function of revenue (purple line) have also moved lower on decreased spending in the near term.

Seeking Alpha Data

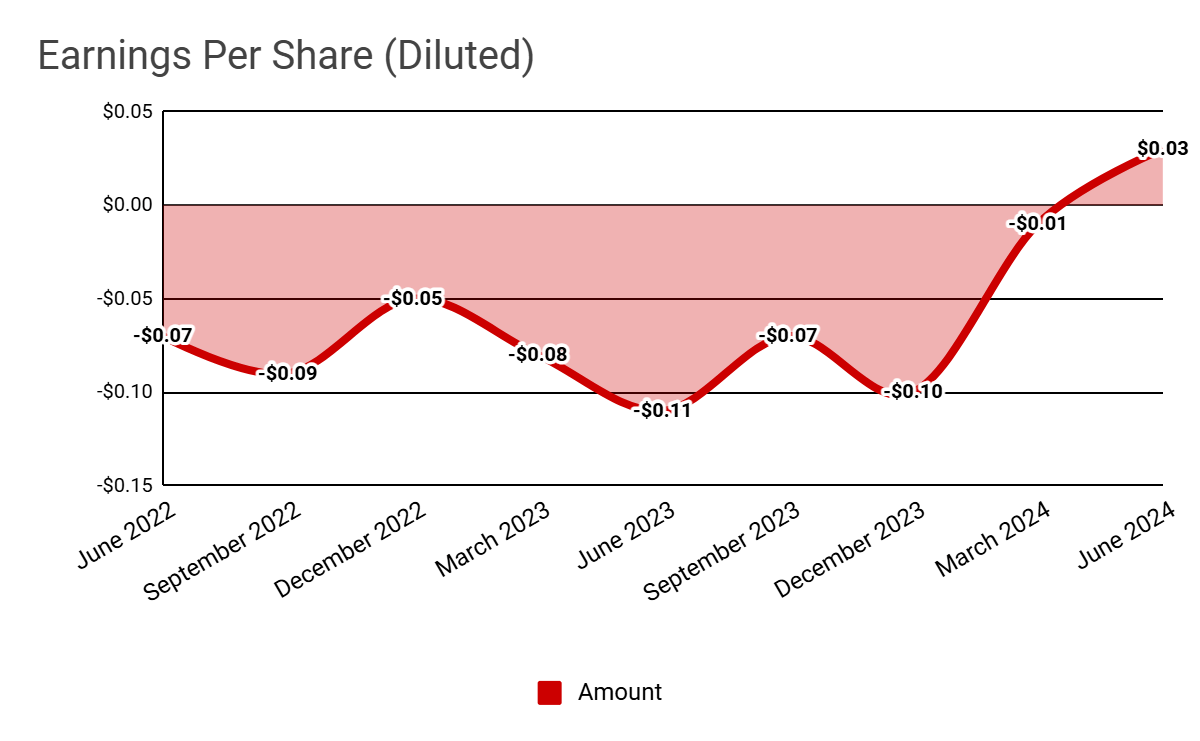

Earnings per share (Diluted) have turned positive after remaining within a negative range for many quarters, a positive development.

Seeking Alpha Data

(All data in the above charts is GAAP.)

For balance sheet results, OLO ended the quarter with $360.7 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash flow was only $7.8 million and capital expenditures were just $0.5 million. The company paid a hefty $45.3 million in stock-based compensation in the last four quarters.

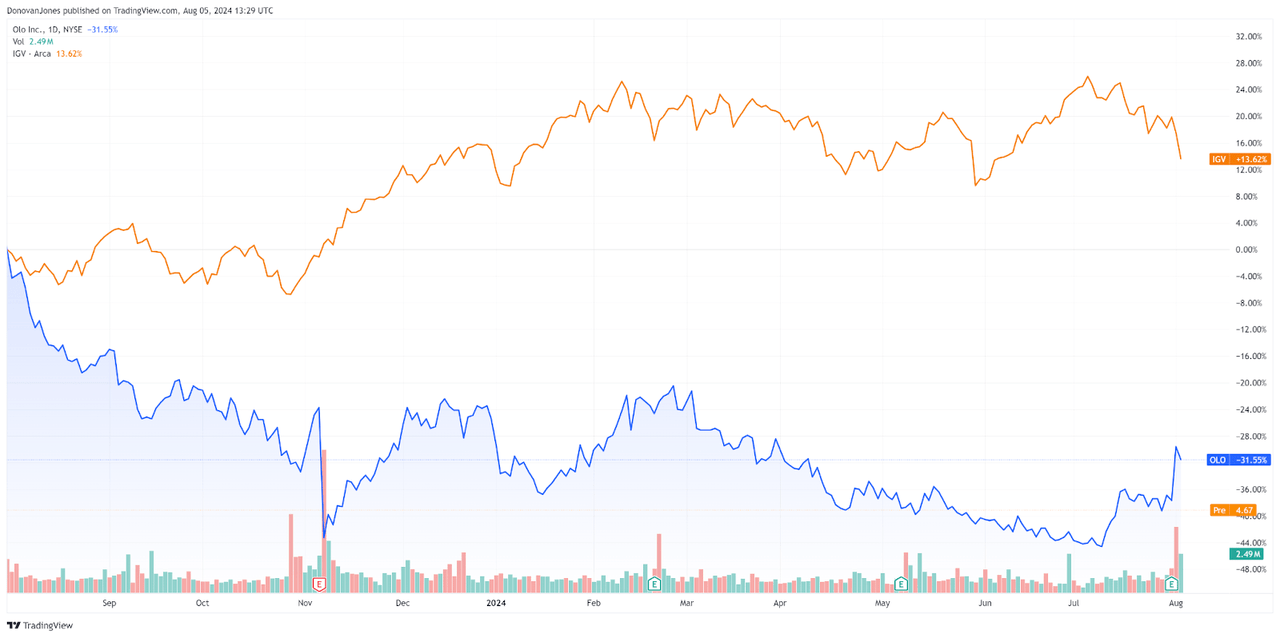

In the past 12 months, OLO’s stock price has dropped by 31.6% vs. that of the iShares Expanded Technology-Software ETF’s (IGV) rise of 13.6%, as the chart shows below.

TradingView

The major financial and operating metrics table below provides a handy reference for various trailing and forward metrics:

|

Metric |

Amount |

|

EV/Sales (“FWD”) |

1.8 |

|

EV/EBITDA (“FWD”) |

18.6 |

|

Price/Sales (“TTM”) |

3.3 |

|

Revenue Growth (“YoY”) |

26.1% |

|

Net Income Margin |

-9.4% |

|

EBITDA Margin |

-10.6% |

|

Market Capitalization |

$851,060,000 |

|

Enterprise Value |

$505,780,000 |

|

Operating Cash Flow |

$8,320,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.15 |

|

2024 FWD EPS Estimate |

$0.20 |

|

Rev. Growth Estimate (“FWD”) |

20.3% |

|

Free Cash Flow/Share (“TTM”) |

-$0.03 |

|

Seeking Alpha Quant Score |

Hold – 2.85 |

(Source: Seeking Alpha)

While the company is not strictly a SaaS-only firm, its Rule of 40 performance shows a need for significant improvement:

|

Rule of 40 Performance (Unadjusted) |

Q2 2024 |

|

Revenue Growth % |

26.1% |

|

Operating Margin |

-9.1% |

|

Total |

17.0% |

(Source: Seeking Alpha)

Olo’s metrics are compared to competitor Toast’s (TOST), and indicate OLO is being valued at lower multiples than TOST, likely due to slower growth and higher net losses:

|

Metric |

Toast |

Olo |

Variance |

|

EV/Sales (“FWD”) |

2.6 |

1.8 |

-29.3% |

|

EV/EBITDA (“FWD”) |

46.8 |

18.6 |

-60.3% |

|

Rev. Growth Estimate (“FWD”) |

30.0% |

20.3% |

-32.5% |

|

Net Income Margin |

-6.0% |

-9.4% |

55.5% |

|

Operating Cash Flow |

$170,000,000 |

$8,320,000 |

-95.1% |

(Source Seeking Alpha Data)

Why I’m Neutral On Olo

Olo’s leadership appears to be managing the company for profitability on reasonable revenue growth.

Its Olo Pay continues to grow activity and gross profit contribution if not reduced gross margin as a result.

As a result, management increased its 2024 revenue guidance to $280 million at the midpoint of a tight range, indicating increasing confidence and also a little extra revenue from the end of the Wingstop relationship, which was delayed somewhat.

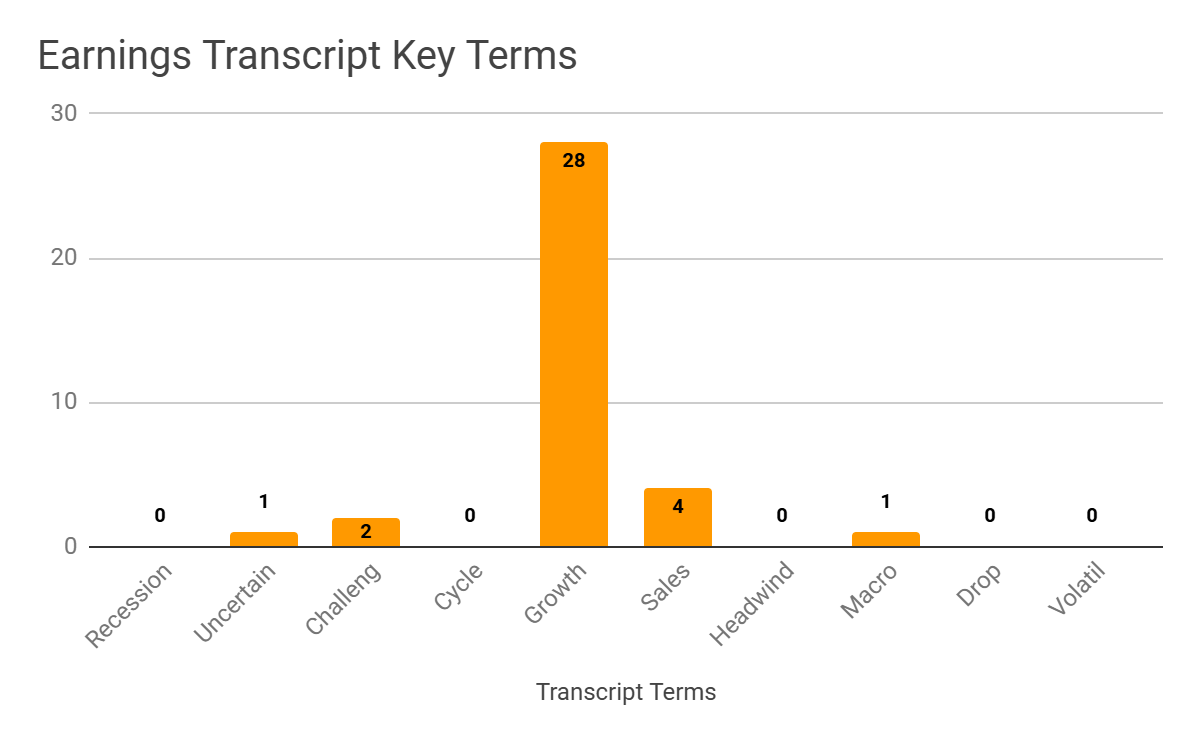

The graphic below shows the frequency of various keywords in the most recent conference call between management and analysts.

Seeking Alpha Data

The company’s clients continue to face macroeconomic challenges and uncertainties, which can make for more demand for their system but also may delay decision-making on a desire to reduce spending.

Many public restaurant companies are noting reduced traffic, causing them to discount. However, Olo’s Engage system can help them improve their marketing motions with customers, reducing their need to discount as their sole strategy.

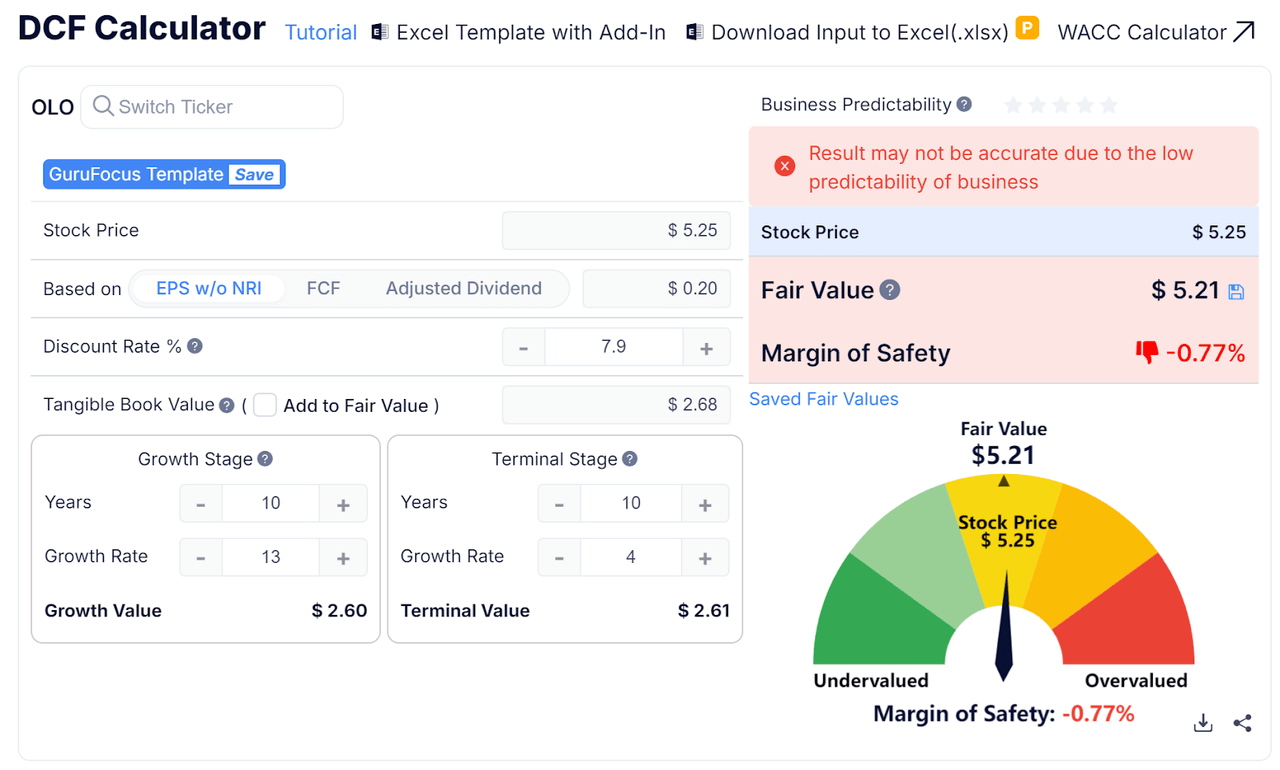

My discounted cash flow calculation for OLO is shown here:

GuruFocus

My assumptions were a generous 13% annual earnings growth rate, a 7.9% discount rate (3.8% 10-year plus 4.1% ERP), and 2024 earnings of $0.20 per share.

The DCF indicates OLO is fully valued given the stated assumptions, and this is further buttressed by its comparison valuation to competitor Toast.

Olo is growing more slowly than Toast, so its lower valuation is reasonable.

While the company’s Olo Pay system will continue to produce revenue growth into 2025 and beyond, it has a lower gross margin profile compared to the firm’s other revenue streams.

The US economy is expected to continue to slow as consumers pull back on discretionary spending, as this economic forecast by The Conference Board expects.

Given the stock’s apparently full valuation against a backdrop of slowing consumer demand, my outlook on OLO in the near term is Neutral (Hold).

Read the full article here