")

We like a little stock-based compensation (SBC). It helps to align incentives of management and employees with shareholder interest. But too much stock-based compensation is a major turn-off. Excessive SBC dilutes company shares which will result in under-performance if the value generated by SBC does not adequately compensate for the dilution. It can be difficult to capture the effect of SBC without examining the financial performance of a company in detail, because SBC is often omitted from non-GAAP measures of performance such as adjusted earnings.

SBC is an expense. We like to invest in growth at a reasonable price. In order to determine the “reasonable price” part of the equation we must understand the expense. The issue is of particular concern with high growth technology companies which tend to distribute SBC at a higher rate than other sectors.

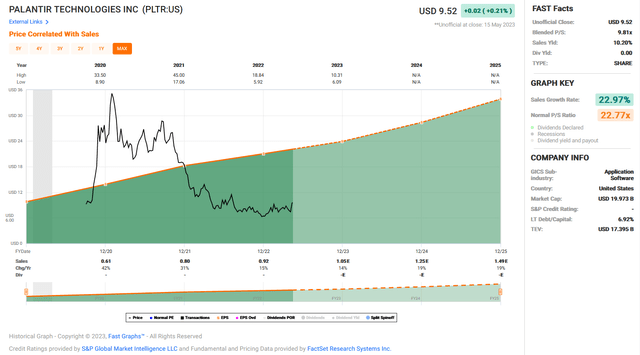

Among those companies with a controversial SBC rate is Palantir Technologies Inc. (NYSE:PLTR). The potential for Palantir’s market is attractive from our perspective. It’s intriguing to examine how the company will be able to leverage AI technology in future developments. The company’s data analysis tools are valuable to large clients and the demand for data security is expected to continue growing. The company is trading at a price to sales ratio of 9.8x which is well below its average of 22.7x.

FAST Graphs

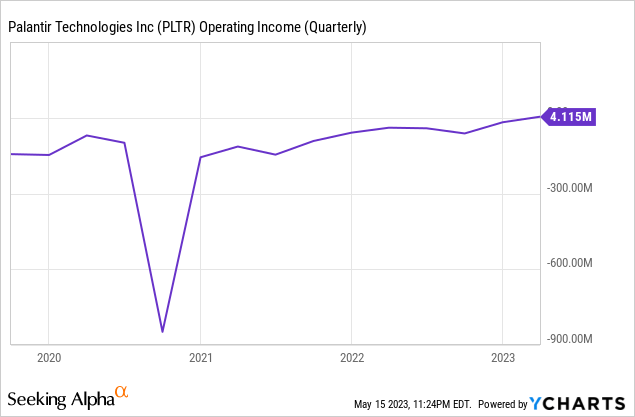

With the company posting its first quarterly operating profit in Q1 2023 of $4.1 million including SBC, it seems like the company could be turning a corner and worth establishing a position. PLTR has long been scrutinized for its SBC practices over the past few years. The company has been making improvements and acting with greater discipline. Unfortunately, it’s still not enough to get us excited.

Stock-Based Dilution

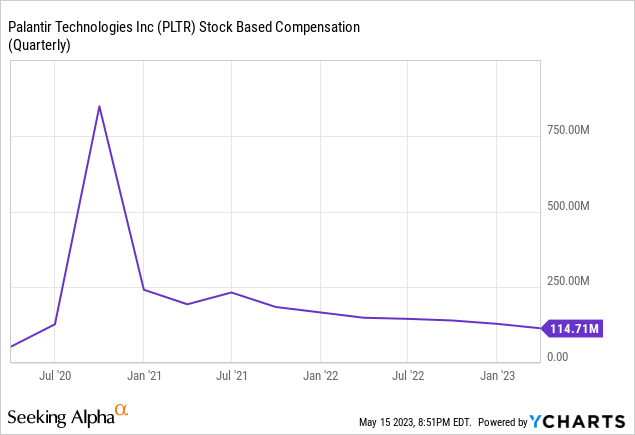

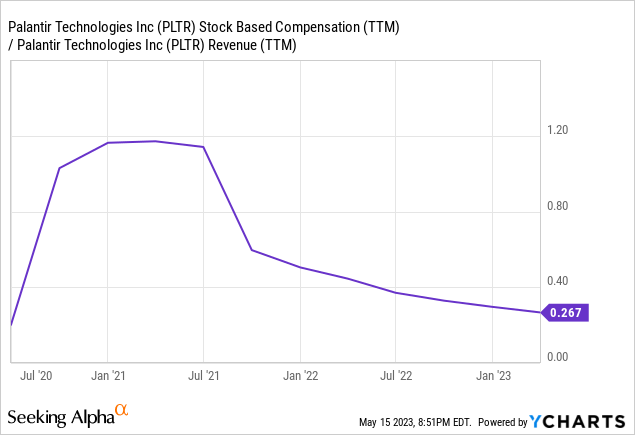

PLTR has issued a significant amount of SBC, including a surge above $750 million per quarter in 2020. Since 2021, the company has been reducing its quarterly SBC. Q1 2023 experienced only $114.714 million in SBC. This is down from $149.323 million in Q1 2022.

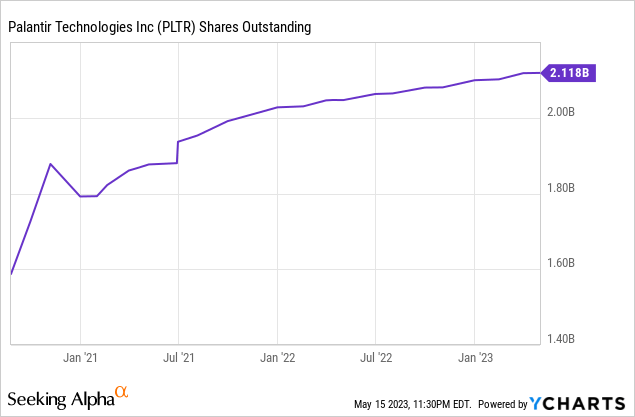

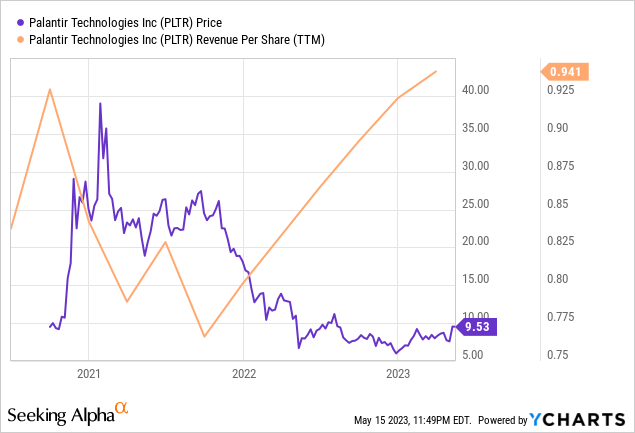

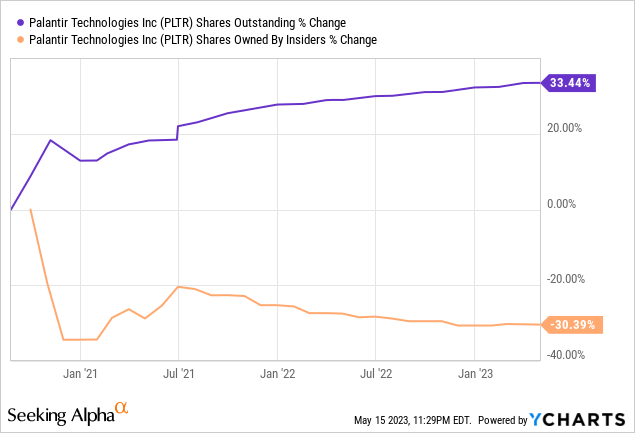

As a result, shares outstanding have ballooned from 1.6 billion in 2020 to 2.118 billion today. By itself, this isn’t necessarily a problem if revenue growth exceeds share growth. Between 2020-2021 revenue per share was in decline, not a good indication. Since 2022, revenue per share has been on the rise. Unsurprisingly, this has corresponded with changes in share price momentum.

It is disconcerting to us that while shares outstanding has increased by 33.44% since 2021, largely a function of SBC, shares owned by insiders has declined by 30%. While some attrition should be expected, the degree of decline does not demonstrate that the SBC is creating the value that shareholders would expect for the dilution they pay.

SBC as a percent of revenue has improved significantly over the past two years. In 2021, the percentage was in excess of 100% which is a major concern for us. Today it stands just under 27%. As of March 31, 2023 the company had unrecognized stock-based compensation expenses related to options outstanding of $686.5 million and $703.2 million related to RSUs which the company expects to be realized over the coming years.

We believe this is too high. Normally, we look for SBC/revenue of 10% or less, although we have a conservative perspective on that. We recognize that some companies have the goal of attracting top talent and that requires solid compensation packages which will include sizeable SBC. Still, the current SBC rate appears to be in excess from our point of view. We’re willing to pay for top talent, but not overpay for it.

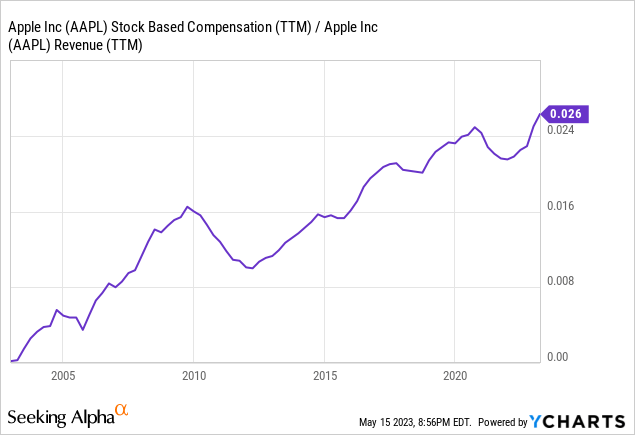

For reference, Apple (AAPL) is now paying its highest SBC/revenue in the last 20 years at 2.6%. While Apple and Palantir are very different technology companies, it demonstrates how wide the gap is between these two companies. It also demonstrates that a technology company does not need high SBC in order to grow into one of the most successful tech companies, as Apple did with SBC/revenue under 1% pre-2010.

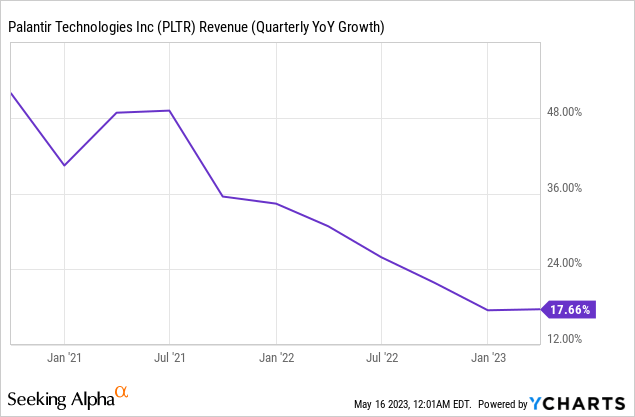

Naturally, as revenue growth slows the company will come under pressure to reduce SBC/revenue. When SBC/revenue was over 100% revenue growth was close to 50% YoY. Today, at SBC/revenue of 26.7% revenue growth is only 17.6% YoY. We are not attracted to revenue growth that is less than SBC/revenue. One way to think of this: all of the company’s revenue growth is going to SBC, and then some. If SBC is supposed to help the company grow, it’s not growing enough.

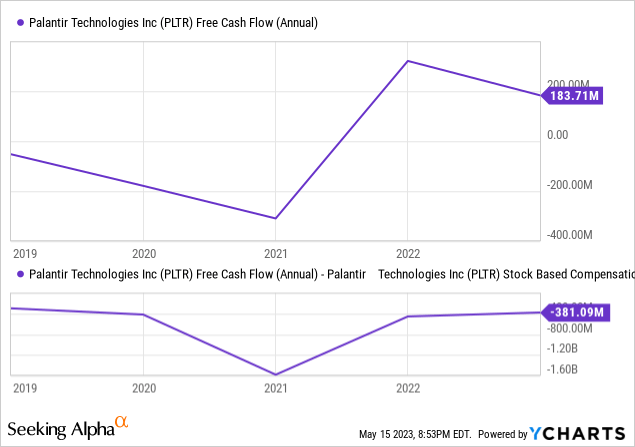

Cash flow is of particular importance to us. It is the basis for “reasonable price” in growth-at-a-reasonable-price. We’re looking for solid free cash flow, free cash flow growth, or free cash flow potential. PLTR last reported free cash flow of $183.71 million and net operating cash flow per share of $0.09. By itself, this cannot determine much. For PLTR we need to add back the SBC to free cash flow to get a clearer picture of cash flow potential. When SBC is subtracted from FCF we see that the company actually lost $381 million. The trend has improved since 2021, when SBC was grossly excessive, but in-line with real/adjusted FCF in 2019. So with all the SBC over the last 4 years, real FCF hasn’t improved much at all.

Summary

PLTR has a track record of loosely diluting its shares in an attempt to attract talent. Unfortunately, the results so far have been mediocre. The company has been tightening up its stock-based compensation structure but revenue growth has contracted simultaneously. There continues to be significant amounts of SBC that is expected to be realized in the near future.

Until the SBC structure becomes more conservative, it is difficult for us to get excited about Palantir. As a shareholder, we would not feel confident that we are getting the value we deserve from that share dilution. For these reasons, we continue to be on the sidelines.

Read the full article here